Sometimes words speak louder than actions. That has certainly been the case lately with the Fed hinting that it may taper off asset purchases by the end of this year.

On Wednesday, Fed Chairman Bernanke said the Federal Reserve would keep monetary policy loose a while longer but hinted that the days of easing may be numbered. Bernanke said that the Fed may wind down its quantitative easing (QE) program if the economy continues to improve.

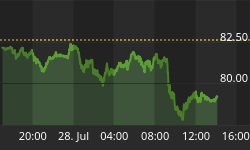

Stock investors weren't happy with the news and the major averages were down by more than 1% at the close on Wednesday. Tellingly, the 10-year Treasury Yield Index (TNX) was up nearly 6% after the Fed's announcement - its highest level since March 2012.

The mere hint that the Fed may back off from QE has been enough to send bond yields the world over to their highest levels in over a year. Bond prices in emerging countries have fallen as investors have pulled their money out of global bonds. The spillover impact of this rise in bond yields was felt immediately in several financial sectors. Global stock prices were down, with Japan's Nikkei index falling 20% into nominal bear market territory in just a few weeks. The Nikkei's decline was also partly in response to the Bank of Japan's recent refusal to accelerate its recent efforts at monetary easing.

Global stock markets clearly don't like the idea of rising interest rates, nor do they like the idea of a slowdown in central bank money printing. This remains a very interest rate-sensitive financial market, and rightfully so: we're still almost a year-and-a-half away from the bottom of the 120-year Kress deflationary cycle and markets today are predicated on the idea of low interest rates. That why an increase in interest rates is bound to upset the apple cart and lead to a sell-off in equities and other assets.

There is a school of thought among some economists that rising bond yields are actually a sign of economic strength. One noted economist has gone so far as to state: "Higher rates normally accompany a healthier economy; they only rarely weaken an economy. This is all very good news." I respectfully disagree. Higher rates in an economy that is still weakened by deflationary undercurrents can only be bad news. This is especially true when one of the leading sectors of growth within the economy, namely real estate, has come to rely on low rates. Indeed, we've already seen in just a few short weeks the destruction that rising rates can do to rate-sensitive industries such as real estate. Witness the sharp decline in the Dow Jones REIT Index (DJR), which fell nearly 15% in just over two weeks.

I would also point out that while the rising interest rate trend isn't sufficiently established enough to be a major threat to the stock market or the economy, it has the potential to create problems down the road if it continues. In many ways the rising rates (and falling bond prices) are beginning to resemble what happened in 1994 when a bond market sell-off added to the pressure of the S&L crisis to hit equities hard. Not coincidentally the 20-year Kress cycle, a component of the 120-year cycle, bottomed in late 1994 and is now entering its final "hard down" phase into 2014.

The celebrated recovery in real estate in the last couple of years has been almost exclusively based on low mortgage rates. Much of the recovery in consumer retail spending is a direct result of the real estate bounce back. One could almost say, "As goes real estate, so goes the economy," so it behooves us to carefully consider the question posed in the above headline.

It's worth pointing out that mortgage rates, like all other types of rates, are on the rise. The average rate for 30-year fixed rate mortgages 4.12% as of June 19, according to Freddie Mac. One year ago the average 30-year FRM was 3.84%. After falling for eight consecutive weeks earlier this spring and nearly hitting an all-time low, rates have risen the past few weeks on the back of the rally in Treasury yields. The Mortgage Bankers Association (MBA), which represents the real estate finance industry, predicts 30-year mortgage rates will rise to 4.4% by the end of this year. Does anyone dare suggest the housing market will simply shrug off even a minor increase in rates over the next several months?

The dominant longer-term trend for interest rates is clearly down, however, as you can see in the following graph. The trend for the 30-year conventional mortgage rate is defined by the chart pattern of lower highs and lower lows which has been established since 2006. As Robert Campbell said in a recent issue of his Real Estate Timing Letter, "Until the actions of the Fed speak otherwise, Fed policy is currently working to push mortgage rates down."

The bottom line is that while the longer-term rate trend is down, as long as the intermediate-term interest rate trend is up it can still create significant volatility for both equity and real estate markets. And as we learned from the lesson of 1994, even a temporary rate increase is nothing to scoff at.

Gold

A growing number of asset managers from high profile investment banks foresee a gold breakdown, however. Could they be correct in their dire prediction? Ordinarily we could answer that question in the negative. After all, fund managers have a historical tendency to be wrong at major inflection points. But this isn't an inflection point for gold, at least not yet. What we're dealing with here is a possible continuation of a well-established trend that has been in place for almost two years. The crowd (and by "crowd" we can include fund managers) can be right during the final "hard down" portion of a major bear market, much like they were during the final months of the 2008 credit crisis.

Also worth pointing out is that downside momentum and negative investor sentiment both tend to feed on itself during the last stages of a major decline. With so many hedge funds responsible for the short-term moves in commodities like gold, all it takes is for a herd mentality to develop and the next thing you know there can be a self-fulfilling sell-off underway.

Just how bearish has the crowd become on the yellow metal? Based on a Bloomberg survey, the number of traders expressing bearish views on gold increased to its highest level this year. Confirming this widespread bearish sentiment, gold-backed ETP holdings fell to a two-year low of 2,117 metric tons last week. While some investors looked for the Chinese to lend support to the physical gold market with continued purchases of physical bullion, the cards appear to be stacked against gold in the short term.