An unfolding EM crisis, higher Treasury yields, a short squeeze and various market mayhem.

The thesis has been that unconstrained global Credit inherently fuels serial boom and bust cycles. In particular, the dramatic policy response to the 2008/09 collapse of the Mortgage Finance Bubble incited unprecedented financial and economic excess in China and throughout the "developing" economies. Double-digit Credit growth has been compounding over recent years in China, Brazil, India, Turkey and, generally, throughout Asia and Latin America. I have referred to such a late-cycle dynamic as the "terminal phase" of Credit Bubble excess.

For going on five years now, unprecedented "hot money" has inundated emerging market (EM) financial systems and economies. And as "money" flooded in, EM central banks "recycled" much of this liquidity right back into U.S. Treasuries, German bunds, and sovereign debt around the world. This massive flow of finance into EM also spurred a spectacular expansion in sovereign wealth funds (SWF), hedge funds and the "global leveraged speculating community" more generally. The rapid growth in both EM central bank reserve assets and the global pool of speculative finance solidified the perception of unlimited cheap global liquidity. Repeated - and increasingly desperate - central bank measures over recent years have further crystalized the perception that global markets enjoy a powerful liquidity backstop. Accordingly, speculation has run roughshod through the global markets.

A strong case can be made that recent years have seen the greatest episode of global securities mispricing in history. Global yields collapsed throughout, although nowhere has this mispricing been more pronounced than with EM bond markets. For example, Brazilian (dollar-denominated) bond yields collapsed from above 25% in 2002 to a record low 2.5% last year (currently 4.8%). After averaging about 7% for the period 2003-2011, Turkish (dollar-denominated) bond yields sank to a record low 3.17% in November 2012 (currently 5.6%). After last year sinking to record low 2.84%, Indonesian dollar bond yields have jumped back to 6.12%.

The bullish EM case has been premised on superior fundamentals compared to the developing world. The bear case is that EM markets have been at the heart of historic Bubble excess. I posit that EM securities markets have provided the most extreme case of misperceptions, speculative excess and a general mispricing of risk throughout. I would further argue that the EM Bubble has begun to burst. Moreover, I would expect that global markets have likely commenced a problematic "periphery" to "core" Credit and economic crisis - where risk aversion, de-leveraging and resulting liquidity issues move from one market to the next. This dynamic has been held somewhat at bay by massive Fed and BOJ QE and Draghi's liquidity backstop.

So far in 2013, the Brazilian real has declined 12.66% and the Argentine peso 12.59%. India's rupee has dropped 13.25%. The Turkish lira is down 10.26%, the Indonesia rupiah 11.44%, the Malaysian ringgit 7.35%, and the Thai baht 3.96%. The South African rand has lost 17.28% and the Russian ruble 7.51%.

Over the past three months, the Brazilian real has declined 12.98%, the Indian rupee 12.32%, the Indonesian rupiah 11.53%, the Malaysian ringgit 8.10%, the Turkish lira 7.11%, the South African rand 6.98%, the Argentine peso 6.42%, the Thai baht 6.09% and the Philippine peso 5.63%.

Market action in recent months has caught many participants be surprise, including some of the most sophisticated market operators. In particular, instead of rallying on heightened EM instability, "core" sovereign bond prices have unexpectedly been hit by selling pressure. Treasury yields have surged 82 bps during the past three months and bund yields have jumped 50 bps. Recent atypical correlations between "core" (perceived safe haven) bonds and EM risk markets have thrown a monkey wrench into many investment/speculation strategies (including variations of popular "risk parity" models).

August 22 - Financial Times (Robin Wigglesworth): "Central banks in the developing world have lost $81bn of emergency reserves through capital outflows and currency market interventions since early May, even before the recent renewal of turmoil in emerging markets. The figure, which excludes China, is equal to roughly 2% of all developing country central bank reserves, according to Morgan Stanley analysts, who compiled the data from central bank filings for May, June and July. However some countries have suffered more precipitous drops. Indonesia has lost 13.6% of its central bank reserves between the end of April and the end of July, Turkey 12.7% and Ukraine burnt through almost 10%. India, another country that has seen its currency pummelled in recent months, has shed almost 5.5% of its reserves. 'It's a real regime change compared to what we have been used to for the past decade,' said James Lord, a Morgan Stanley strategist. 'We saw huge reserve accumulation as emerging markets tried to stem currency appreciation, but now we're seeing the exact opposite.'"

The flood of "hot money" finance into EM spurred years of domestic Credit system excess and attendant destabilizing loose "money." The reversal of "hot money" flows has now instigated a problematic tightening of finance. Importantly, years of historic loose finance created Credit systems and economic structures vulnerable to any meaningful tightening of financial conditions. Over recent months, this latent fragility has been increasingly on display.

I have argued that the dramatic policy measures from one year ago (Draghi's "do whatever it takes" and the Fed's $85bn monthly QE) were in response to heightened global fragilities - and that such desperate measures would only work to further destabilize already disorderly global finance. As for EM, unwieldy flows over the past year have, I believe, only created greater fragilities. In Europe, Draghi's OMT ("outright monetary transactions") backstop was instrumental in both a loosening of finance and a general political backtracking from financial and economic reform (especially at the troubled "periphery").

In the U.S., open-ended QE has had minimal impact on the unemployment rate, while exerting dramatic effects on stock prices, corporate debt issuance (especially riskier debt) and home prices (especially at the upper-end). Going on five years of near-zero short-term rates and bond market intervention has coerced an unprecedented shift of saver assets from the safety of "money" to the risk market wolves. The belief that the Federal Reserve and global central banks would continue to backstop risk markets has been fundamental to epic market mispricing.

Moreover, Trillions have flowed into myriad perceived "money-like" products, strategies and funds (ETFs, hedge funds, SWFs, "bond" and "total return" funds, and various "structured products" and other derivatives) where investors have little appreciation for the degree of associated price, Credit and liquidity risks. The protracted period of massive flows significantly impacted the markets in the underlying securities acquired through these strategies, in particular distorting perceptions of marketplace liquidity (in particular for EM securities and U.S. municipal debt). Misperceptions coupled with significantly inflated securities prices create latent market fragilities.

It's not difficult for speculators and investors alike in U.S. markets to disregard the unfolding EM crisis and market risk more generally. After all, ignoring global macro issues has been rewarded handsomely for some time now. Moreover, with the Fed and Bank of Japan (BOJ) combining for about $160bn of monthly QE, ample (developed) marketplace liquidity has seemingly been ensured. And increasingly unstable "periphery" markets also seem to ensure rotation from EM to developed markets, especially U.S. stocks. This is particularly the case with the highly inflated (performance-chasing and trend-following) "global pool of speculative finance." Indeed, the confluence of acute EM fragilities, $85bn monthly QE and highly-speculative markets has spurred progressively more dangerous speculative excess throughout the U.S. equities marketplace.

August 21 - Wall Street Journal (Juliet Chung and Rob Barry): "Short sellers are facing their worst losses in at least a decade, a Wall Street Journal analysis has found, as many of the rising stocks they bet against have only continued to soar. That has stung several high-profile hedge-fund managers, including William Ackman and David Einhorn, who have placed prominent short bets. In the Russell 3000 index, the 100 most heavily shorted stocks are sharply outperforming the average returns of stocks in the index, according to a Journal analysis of data provided by S&P Capital IQ. The shorted stocks are up by an average of 33.8% through Aug. 16, versus 18.3% for all stocks in the index. The gap between the performance of the most-shorted shares... and the market as a whole is wider than it has been in at least a decade... 'It's actually more painful now than it was in '99,' said veteran short seller Andrew Left of... Citron Research."

My "Issues 2013" premise was that an increasingly distended "global government finance Bubble" was susceptible to significant bipolar risks: an intensified Bubble might either begin to falter or it would become a case of "how crazy do things get." Well, at this point, there are cracks to go along with a lot of craziness. Comparisons to 1999 speculative excesses resonate. And while it is easy for most to dismiss (or, better yet, relish) the pain being inflicted upon short sellers, the bludgeoning of the bears is indicative of a highly speculative marketplace that has become disconnected from underlying fundamentals.

Global markets have become keenly sensitive to Fed "tapering" risks. On the one hand, the unfolding EM crisis has sparked de-risking and de-leveraging dynamics. "Hot money" has begun to flee EM, in the process initiating the self-reinforcing downside of what has been a historic Credit boom. EM central banks have been forced to sell international reserves (Treasury, bund, etc.) to bolster their flagging currencies and vulnerable debt and securities markets. Resulting higher yields have forced de-risking and de-leveraging in ("safe haven") Treasuries, which has worked to pressure U.S. MBS and muni debt, in particular.

On the other hand, Fed QE is fueling major market distortions. The Fed liquidity backstop has provided a magnetic pull for global "hot money," giving a competitive advantage to U.S. risk assets, stocks, corporate debt and, ultimately, the U.S. economy. In a replay of the late-nineties, the "king dollar" dynamic has been exacerbating EM outflows and attendant fragilities. Meanwhile, the supposed inevitable winding down of QE provides an incentive for EM central banks and the speculator community to commence de-risking prior to the withdrawal of the Federal Reserve's market liquidity backstop. If bonds trade this poorly in the face of the Fed's $85bn monthly purchases, who is content to wait and see the marketplace liquidity profile when our central bank is no longer a huge buyer.

The unfolding tightening of EM financial conditions portends trouble for the global economy. EM markets have begun to adjust to harsh new realities. Developed markets, if they were functioning normally, would have begun to adjust to mounting risks to the global financial system and economy. Instead, market players assume heightened fragilities will only extend the period of unprecedented developed central bank "money printing" and market intervention. This view was bolstered by Bernanke's comments that the Fed would "push back" against any tightening of financial conditions.

The upshot has been a late-cycle speculative melt-up in U.S. stocks, in particular. Popularly shorted stocks have been targeted for "squeezes" the most aggressively since 1999. So-called "high beta" stocks have become market darlings like it's 1999. Stocks with minimal earnings (hence, little risk of earnings disappointments) have become the target of market game-playing and shenanigans to an extent not experienced since 1999.

The excesses from 1999 set the backdrop for a major market Bubble top in early-2000. Yet the late-nineties Bubble was relatively contained, chiefly impacting a narrow group of stocks, the technology sector and only a segment of the U.S. and global economy. The now well-entrenched "global government finance Bubble" has become deeply systemic in the U.S. and abroad. The Bubble essentially enveloped all risk market and myriad strategies. It has fueled conspicuous speculative excess in risky strategies. It has, as well, fueled unappreciated excesses throughout perceived low-risk strategies.

The Bubble has spurred excessive issuance and mispricing in high-risk junk bonds, leveraged loans and risky municipal debt. It has also spurred massive over-issuance of perceived high-quality Treasury securities and "money-like" debt instruments. It has spurred a boom in perceived liquid and low-risk ETF products, funds that loaded up on illiquid securities as "money" flooded in. It has fueled record assets in hedge funds and sovereign wealth funds. It has spurred incredible concentration of assets in the hands of a group of sophisticated financial operators most adept at playing policy-driven speculative markets.

As an analyst of Bubbles, I readily admit it is impossible to accurately predict the timing of their demise. Even in hindsight, I have no idea why technology stocks put in Bubble highs in March of 2000. It's not clear why stocks peaked again when they did in 2007. It's never been clear to me why the U.S. equities Bubble cracked when it did in late-1929. But all those major market tops were put in after speculative market melt-ups pushed the divergence between inflated securities price Bubbles and deteriorating fundamentals to precarious extremes. And all three speculative melt-ups were fueled in part by powerful short squeezes, squeezes made possible by traders shorting securities in response to deteriorating fundamental backdrops. A similar environment exists for a major top in 2013.

For the Week:

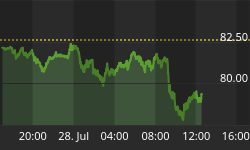

The S&P500 added 0.5% (up 16.6% y-t-d), while the Dow declined 0.5% (up 14.6%). The S&P 400 MidCaps jumped 1.0% (up 19.3%), and the small cap Russell 2000 rose 1.4% (up 22.2%). The Morgan Stanley Consumer index slipped 0.2% (up 20.9%), while the Utilities increased 0.2% (up 5.8%). The Banks increased 0.3% (up 26.6%), and the Broker/Dealers advanced 1.3% (up 42.7%). The Morgan Stanley Cyclicals were down 0.4% (up 20.0%), while the Transports were up 1.7% (up 22.1%). The Nasdaq100 surged 1.6% (up 17.4%), while the Morgan Stanley High Tech index slipped 0.1% (up 14.7%). The Semiconductors gained 0.3% (up 20.8%). The InteractiveWeek Internet index rose 0.7% (up 22.9%). The Biotechs surged 3.5% (up 34.1%). With bullion gaining $21, the HUI gold index was up 0.6% (down 38.6%).

One-month Treasury bill rates ended the week at one basis point and three-month bill rates closed at 3 bps. Two-year government yields increased 4 bps to 0.38%. Five-year T-note yields ended the week up 6 bps to 1.62%. Ten-year yields slipped a basis point to 2.82%. Long bond yields declined 5 bps to 3.79%. Benchmark Fannie MBS yields declined 3 bps to 3.60%. The spread between benchmark MBS and 10-year Treasury yields narrowed 2 to 78 bps. The implied yield on December 2014 eurodollar futures jumped 5 bps to 0.71%. The two-year dollar swap spread was little changed at 18 bps, while the 10-year swap spread rose about 3 to 19 bps. Corporate bond spreads were mostly narrower. An index of investment grade bond risk declined 2 to 79 bps. An index of junk bond risk dropped 19 to 387 bps. An index of emerging market debt risk jumped 23 to 345 bps.

Debt issuance slowed. Investment grade issues included PNC $750 million, Southern Co $500 million, Pricoa Global Funding $500 million, DTE Electric $400 million, Entergy Louisiana $325 million, and Western Union $250 million.

Junk bond funds suffered outflows of $2.33bn (from Lipper). Junk issuers this week included Northshore RE $200 million and Beazer Homes $200 million.

Convertible debt issuers included B2Gold Corp $225 million and Spansion $200 million.

International dollar debt issuers included Sweden $3.0bn, Interamerican Development Bank $2.0bn, Korea Development Bank $1.0bn, Abbey National $1.0bn and Metrocat RE $200 million.

Ten-year Portuguese yields rose 6 bps to 6.43% (down 32bps y-t-d). Italian 10-yr yields jumped 14 bps to 4.32% (down 18bps). Spain's 10-year yields rose 8 bps to 4.44% (down 83bps). German bund yields increased 5 bps to 1.93% (up 61bps), and French yields jumped 8 bps to 2.47% (up 47bps). The French to German 10-year bond spread widened 3 to 54 bps. Greek 10-year note yields gained 16 bps to 9.78% (down 69bps). U.K. 10-year gilt yields were unchanged at 2.70% (up 88bps).

Japan's Nikkei equities index ended the week little changed (up 31.4% y-t-d). Japanese 10-year "JGB" yields added a basis point to 0.76% (down 2bps). The German DAX equities index added 0.3% for the week (up 10.6%). Spain's IBEX 35 equities index fell 1.5% (up 6.4%). Italy's FTSE MIB lost 1.9% (up 6.6%). Emerging markets were mostly lower. Brazil's Bovespa index gained 1.3% (down 14.4%), while Mexico's Bolsa was slammed for 2.7% (down 6.4%). South Korea's Kospi index dropped 2.6% (down 6.4%). India's Sensex equities index declined 0.4% (down 4.7%). China's Shanghai Exchange fell 0.5% (down 9.3%).

Freddie Mac 30-year fixed mortgage rates surged 18 bps to a two-year high 4.58% (up 92bps y-o-y). Fifteen-year fixed rates rose 16 bps to 3.60% (up 71bps). One-year ARM rates were unchanged at 2.67% (up one bp). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed rates up 11 bps to 4.75% (up 49bps).

Federal Reserve Credit jumped $24.1bn to a record $3.590 TN. Fed Credit expanded $804bn during the past 46 weeks. Over the past year, Fed Credit was up $779bn, or 27.7%.

Global central bank "international reserve assets" (excluding gold) - as tallied by Bloomberg - were up $652bn y-o-y, or 6.2%, to a record $11.185 TN. Over two years, reserves were $1.049 TN higher, for 10% growth.

M2 (narrow) "money" supply declined $23.5bn to $10.761 TN. "Narrow money" expanded 7.0% ($707bn) over the past year. For the week, Currency increased $1.2bn. Total Checkable deposits dropped $35.0bn, while Savings Deposits expanded $9.3bn. Small Time Deposits slipped $0.9bn. Retail Money Funds increased $1.7bn.

Money market fund assets increased $15.5bn to $2.637 TN. Money Fund assets were up $64bn from a year ago, or 2.5%.

Total Commercial Paper outstanding jumped $16.7bn this week to $1.020 TN. CP has declined $45.2bn y-t-d and $0.5bn, or 0.4%, over the past year.

Currency and 'Currency War' Watch:

August 23 - Bloomberg (Matthew Malinowski and Blake Schmidt): "Brazil's real posted its biggest gain in almost two years as the central bank stepped up efforts to stem the world's worst currency decline, announcing a $60 billion intervention program involving swaps and loans. The real climbed 3.7% to 2.3488 per dollar in Sao Paulo, paring its decline in the past three months to 13%, still the biggest among 31 major dollar counterparts tracked by Bloomberg."

The U.S. dollar index was little changed at 81.36 (up 2.0% y-t-d). For the week on the upside, the Brazilian real increased 1.9%, the Swedish krona 0.5%, the Swiss franc 0.5%, the euro 0.4% and the Danish krone 0.4%. For the week on the downside, the New Zealand dollar declined 3.7%, the Australian dollar 1.7%, the Norwegian krone 1.7%, the Canadian dollar 1.5%, the South African rand 1.5%, the Japanese yen 1.2%, the Singapore dollar 0.7%, the British pound 0.4%, the Mexican peso 0.4%, the South Korean won 0.3% and the Taiwanese dollar 0.3%.

Commodities Watch:

The CRB index slipped 0.6% this week (down 1.4% y-t-d). The Goldman Sachs Commodities Index was little changed (up 0.4%). Spot Gold gained 1.5% to $1,398 (down 16.6%). Silver jumped 1.7% to $23.78 (down 21%). October Crude declined 87 cents to $106.42 (up 16%). September Gasoline gained 1.3% (up 9%), and September Natural Gas added 0.1% (up 4%). December Copper slipped 0.3% (down 8%). September Wheat rallied 0.6% (down 18%), and September Corn jumped 4.6% (down 29%).

U.S. Fixed Income Bubble Watch:

August 22 - Wall Street Journal (Katy Burne): "Investors have yanked $30.3 billion from U.S.-listed bond mutual funds and exchange-traded funds this month, marking the third-largest monthly outflow in records going back to 1984, according to estimates by TrimTabs... The August moves come on the heels of a record $69.1 billion monthly outflow in June and a $14.8 billion outflow in July. Before June, bond funds posted inflows for 21 consecutive months. Some $1.2 trillion of investor funds flowed into bond funds between 2009 and 2012."

August 19 - Bloomberg (Liz Capo McCormick and Anchalee Worrachate): "Regulations aimed at reducing the risk of another financial crisis are starting to upend a key part of the bond market that expedites trading in everything from Treasuries to junk bonds. The U.S. repurchase, or repo, market where banks and investors borrow and lend Treasuries and other fixed-income securities shrunk to $4.6 trillion daily outstanding last month, down 35% from a peak of $7.02 trillion in the first quarter of 2008... From fewer repos to lower inventories of bonds, financial institutions are responding to more stringent capital standards imposed by regulators around the world. Already, the group of dealers and investors that advise the U.S. Treasury say that they see declines in liquidity in times of market stress, including wider gaps between bid and offer prices and the speed of completing trades... 'During the market selloff over the past few months, those rules, a lot of which are just proposed or not yet taken effect, already impacted dealers' willingness to take on inventory of Treasuries, investment grade corporates to emerging market debt,' Gregory Whiteley, who manages government debt investments at... DoubleLine Capital LP, which oversees $57 billion, said... 'That exacerbated the intensity of the selloff.'"

August 23 - Bloomberg (Matt Robinson): "Losses this month in fixed-income markets are making 2013 among the worst years on record for U.S. investment-grade corporate bonds, even exceeding 1994 when the Federal Reserve shocked investors by doubling benchmark interest rates in 12 months. A 1.8% decline in August in the Bank of America Merrill Lynch U.S. Corporate Index brings losses for the year to 4.3%. That contrasts with a 17.8% return in the Standard & Poor's 500 Index and marks the biggest underperformance for bonds since 1999, when they lost 1.9% while shares soared 21% including reinvested dividends."

August 22 - Bloomberg (Michelle Kaske): "The largest exchange-traded fund tracking the $3.7 trillion municipal-bond market is selling for less than the value of its holdings for a record stretch as demand for local debt sinks to the lowest level in more than two years. The $3.2 billion iShares S&P National AMT-Free Municipal Bond Fund, known as MUB, traded at a discount to its net asset value for 61 straight days through Aug. 21..."

August 19 - Bloomberg (Sridhar Natarajan and Lisa Abramowicz): "Leveraged loans are becoming more volatile as they attract unprecedented cash from investors seeking debt that offers protection from rising interest rates. Loan prices have swung 11.92 cents on the dollar since the end of 2010, compared with a 1.5-cent fluctuation in the three years ended Dec. 31, 2006... Mutual and exchange-traded funds that focus on the floating-rate debt have attracted about $45.5 billion of new money this year, increasing their assets by 60%... While the flows have helped speculative-grade companies refinance and lower rates on more than $300 billion of existing loans, concern is rising that the cash could flow out just as quickly, causing borrowing costs to soar. Mutual funds and ETFs now own about 20% of the U.S. leveraged-loan market, about the most ever, and may contribute to bigger price swings going forward, according to Fitch Ratings. 'I don't think it's all going to be smooth sailing,' Darin Schmalz, a director at Fitch in Chicago, said.... 'Looking at loans over time, it was a pretty stable asset class. We found out this can be a volatile asset class.'"

August 21 - Bloomberg (Brian Chappatta): "Michigan's Finance Authority is offering an interest rate 14 times higher than that on top-rated bonds to sell $92 million of one-year notes for Detroit's public schools. Today's deal is the first tied to the Motor City since it sought bankruptcy protection July 18. The bonds are backed by state aid payments. The securities maturing in August 2014 are being offered with a preliminary yield of 4.5%... That compares with a 0.32% interest rate on benchmark AAA munis due in one year."

August 19 - Bloomberg (Michelle Kaske and Mark Niquette): "Ohio's debt is headed for its worst annual return since 2008 because of a slump in the value of the state's tobacco bonds. Municipal bonds issued in Ohio have lost 5.7% since Dec. 31, compared with a 10% gain in 2012... The Buckeye State's debt is on track to lose the most value in five years even though an improving economy boosted state cash reserves to a record. Tobacco bonds are burdening the second-biggest economy among Midwestern states after Illinois. Debt backed by payments from cigarette makers is the worst-performing segment of the $3.7 trillion muni market with a 9.3% loss this year, after gaining 25% in 2012... A decline in smoking has reduced revenue from the companies."

U.S. Bubble Economy Watch:

August 23 - Bloomberg (John Gittelsohn and Heather Perlberg): "American Homes 4 Rent yesterday fired a group of workers, with a focus on acquisition and construction staff, after the housing landlord reported a fiscal second-quarter loss... The company, owner of almost 20,000 single-family homes, has cut about 15% of its workforce this year, including an earlier round of terminations before its initial public offering last month... The Malibu, California-based company, which raised $705.9 million in the IPO, had a net loss of $14 million... on revenue of $18.1 million in the quarter ended June 30... Single-family landlords have struggled to turn a profit while acquiring homes faster than they can fill them with tenants. Hedge funds, private-equity firms and real estate investment trusts have raised more than $18 billion to purchase more than 100,000 rental houses in the past two years."

August 23 - Bloomberg (Prashant Gopal): "U.S. house prices rose 7.7% in the year through June, extending a recovery that's spurring more homeowners to list their properties for sale. Prices climbed 0.7% on a seasonally adjusted basis from May... Price increases are drawing more sellers to a market where a tight supply of homes has pushed up values, said Paul Diggle, property economist at Capital Economics Ltd. in London. The inventory of unsold homes was a seasonally adjusted 5 months in June, up from 4.7 months in January..."

August 20 - Bloomberg (Kathleen M. Howley): "A five-bedroom house in Las Vegas sold in mid-July for $499,000, double the price it went for three months ago. In Phoenix, a similar house sold this month for $600,000, gaining $273,000 since March. Bubbles are inflating in Nevada and Arizona even as housing in the rest of the country recovers at a more sustainable pace. Gains in the two desert cities are the biggest since the height of the real estate boom, just before their plunge to the bottom of the national housing collapse. This year, Las Vegas and Phoenix have topped the nation in price increases, according to the S&P/Case-Shiller property-value index. 'They're clearly in bubbles,' said Karl Case, one of the creators of the index. 'What can go up can go down -- real quick.' In May, Phoenix prices jumped 21% and in Las Vegas, they rose 23% from a year earlier."

August 22 - Bloomberg (Sarah Mulholland): "Borrowing costs are rising for subprime auto lenders in the asset-backed bond market, squeezing profit margins and pressuring firms to make even riskier loans. A General Motors Co. unit that makes car loans to people with blemished or limited credit sold top-rated securities backed by the debt to yield 45 bps more than the benchmark swap rate on Aug. 7, almost double the spread it paid on similar notes in April... American Credit Acceptance Corp., the... buyer of 'deep subprime' loans, paid 225 bps over benchmarks to sell A rated debt on July 31, up from 165 in March."

August 21 - Bloomberg (Chris Christoff): "As many as 50,000 stray dogs roam the streets and vacant homes of bankrupt Detroit, replacing residents, menacing humans who remain and overwhelming the city's ability to find them homes or peaceful deaths. Dens of as many as 20 canines have been found in boarded-up homes in the community of about 700,000 that once pulsed with 1.8 million people. One officer in the Police Department's skeleton animal-control unit recalled a pack splashing away in a basement that flooded when thieves ripped out water pipes."

Federal Reserve Watch:

August 23 - Bloomberg (Joshua Zumbrun): "The U.S. central bank's bond buying is a less potent tool for stimulating growth than policy makers believe, two economists said in a paper released... at a Federal Reserve conference. The paper scrutinizes the stance of some Fed officials that so-called quantitative easing works through a 'portfolio- balance channel' in which Fed asset purchases induce investors to rebalance their investments to boost a wide range of financial assets. The research was presented at an annual Kansas City Fed symposium in Jackson Hole, Wyoming. 'The portfolio balance channel of QE works largely through narrow channels that affect the prices of purchased assets, with spillovers depending on particulars of the assets and economic conditions,' Northwestern University finance professor Arvind Krishnamurthy and University of California-Berkeley professor Annette Vissing-Jorgensen wrote... 'It does not, as the Fed proposes, work through broad channels such as affecting the term premium on all long-term bonds.'"

August 22 - Bloomberg (Jeff Kearns): "Federal Reserve policy makers considering when to reduce bond buying were 'broadly comfortable' with Chairman Ben S. Bernanke's plan to taper this year if the economy strengthens, with a few saying a reduction may be needed soon, minutes of their last meeting show. 'Almost all committee members agreed that a change in the purchase program was not yet appropriate,' and a few said 'it might soon be time to slow somewhat the pace of purchases as outlined in that plan,' according to the record... 'A few members emphasized the importance of being patient and evaluating additional information on the economy before deciding on any changes to the pace of asset purchases... Almost all participants confirmed that they were broadly comfortable' with the committee moderating 'the pace of its securities purchases later this year.'"

August 23 - Bloomberg (Steve Matthews): "Federal Reserve Bank of St. Louis President James Bullard, who has backed the Fed's $85 billion in monthly bond buying, said he would be wary of slowing asset purchases next month. 'I wouldn't rule it out,' Bullard told Fox Business Network... 'If it was just me, and I was dictator, I'd probably be for quite a bit of caution here.'"

August 23 - Bloomberg (Jeff Kearns and Steve Matthews): "Three Federal Reserve regional bank presidents differed over the timing for reducing the Fed's $85 billion in monthly bond buying, with one backing a tapering next month if the economy remains strong and two others saying policy makers should take time to assess economic data. 'We can take our time' on slowing purchases, St. Louis Fed President James Bullard... said... San Francisco's John Williams told CNBC he wants to 'taper our purchases later this year' if the economy doesn't flag, while Atlanta's Dennis Lockhart said he 'would be supportive' of slowing purchases next month if the expansion holds up. Williams didn't rule out a tapering next month."

Central Bank Watch:

August 19 - Bloomberg (Stefan Riecher): "The European Central Bank may raise rates if inflation pressure increases, even after it pledged to keep borrowing costs low, according to Germany's Bundesbank. The ECB's commitment 'is not an imperative statement, and it doesn't represent a change' in the monetary policy stance, the German central bank said... 'Forward guidance doesn't rule out an increase in the benchmark rate if greater inflation pressure emerges.' ECB President Mario Draghi said in July for the first time that the ECB will keep interest rates at current levels or lower for an extended period of time...'It is decisive to note that this statement is conditional' upon the unchanged obligation to guarantee price stability, the Bundesbank said. 'Therefore the euro system's forward guidance doesn't represent an unconditional promise about the future path of the benchmark rate.'"

Global Bubble Watch:

August 21 - Reuters (Natsuko Waki): "The world's biggest sovereign wealth funds may see their bumper profits of 2012 diminish this year as recent diversification into high-growth emerging markets starts to produce disappointing returns. Their long-term horizon may allow many sovereign funds, which globally control $5 trillion of oil and other windfall assets, to weather losses. But the sheer size of these funds may increasingly limit the window of opportunities even when emerging markets recover. SWFs have piled into emerging markets, crucially via public equity and debt markets, which are cheap to invest in and big enough to absorb sizeable investments... According to Thomson Reuters data, the world's top 38 sovereign funds which globally invest nearly $900 billion in listed public equities allocate more than a third of the total to emerging markets at $383 billion, up 18% from mid-2012."

August 19 - CNBC (Matt Clinch): "Outflows from U.S. bond mutual funds and exchange traded funds has accelerated in August, according to... TrimTabs, as fears grow of the threat that rising yields pose for the U.S. economy. 'We are concerned that the Fed is starting to lose control of the bond market, which is not good news for the stock market or the highly leveraged U.S. economy,' TrimTabs said... So far this month, U.S. bond mutual funds and ETFs have seen outflows of $19.7 billion, more than the $14.8 billion of outflows in July. August's outflow is already the fourth-highest on record, TrimTabs said, adding that since the start of June bond funds have lost $103.5 billion or 2.7% of total assets."

August 21 - Wall Street Journal (Juliet Chung and Rob Barry): "Short sellers are facing their worst losses in at least a decade, a Wall Street Journal analysis has found, as many of the rising stocks they bet against have only continued to soar. That has stung several high-profile hedge-fund managers, including William Ackman and David Einhorn, who have placed prominent short bets. In the Russell 3000 index, the 100 most heavily shorted stocks are sharply outperforming the average returns of stocks in the index, according to a Journal analysis of data provided by S&P Capital IQ. The shorted stocks are up by an average of 33.8% through Aug. 16, versus 18.3% for all stocks in the index. The gap between the performance of the most-shorted shares... and the market as a whole is wider than it has been in at least a decade... 'It's actually more painful now than it was in '99,' said veteran short seller Andrew Left of... Citron Research."

August 19 - Bloomberg (Jesse Westbrook and Lisa Abramowicz): "Two Brevan Howard Asset Management LLP credit traders left in recent weeks, as the firm scales back after its biggest hedge fund had the worst monthly loss since 2008 in June... At least a dozen traders have left Brevan Howard, Europe's second-largest hedge fund firm, since the end of May... The Master Fund, which accounts for more than two-thirds of Brevan's $40 billion of assets, fell 2.9% in June, its worst month since September 2008..."

August 16 - Bloomberg (Alastair Marsh): "Deutsche Bank AG is among banks increasing sales of structured notes comprised of subordinated financial bonds as investors take on more risk to boost returns. Germany's biggest lender sold $2.5 million of five-year junior notes tied to the debt of Credit Agricole SA, its third such offering this year... Structured notes package derivatives with debt, typically senior bank bonds, to offer customized bets to investors who are also exposed to the credit risk of the issuer. By selecting a bond lower down the capital structure, banks can create securities with higher potential returns. 'By taking on more credit risk, investors can receive coupons on subordinated bonds that can be noticeably higher than on the senior unsecured bonds usually used in structured products,' said Adrian Neave...managing director at Gilliat Financial Solutions..."

Bursting EM Bubble Watch:

August 21 - Bloomberg (Benjamin Harvey): "Turkey's central bank is running out of leeway to fight additional bouts of lira weakness without further increasing interest rates, according to Goldman Sachs Group Inc., BNP Paribas SA and Citigroup Inc. The central bank raised the average cost of funding to lenders to a one-year high of 6.53% on Aug. 15, up from this year's low of 4.52% on May 31. The lira has weakened 2.9% in the period, the biggest decline after Russia's ruble among emerging markets in Europe, the Middle East and Africa."

August 20 - New York Times (Landon Thomas): "In a city where skyscrapers sprout like weeds, none grew as high as the Sapphire tower in Istanbul. Today, it stands as a symbol of how far the mighty may fall. Like a vast majority of new buildings that have blanketed the Istanbul hills in recent years, the Sapphire -- at 856 feet it is the tallest in Turkey and among the loftiest in Europe -- was built on the back of cheap loans, in dollars, that have flooded Turkey and other fast-growing markets like Brazil, India and South Korea. The money began to flow when the Federal Reserve and other major central banks cut interest rates to the bone in 2009 and cranked up the printing presses in a bid to spur recovery in the United States and other advanced industrial nations. But now, with expectations mounting that the Federal Reserve, led by its departing chairman Ben S. Bernanke, may soon begin to tighten its monetary spigot, Istanbul's skyline could well be a harbinger of an emerging-market bust brought on by unpaid loans, weakening currencies, and, eventually, the possible failure of developers and banks."

China Bubble Watch:

August 21 - Financial Times (Josh Noble): "When China unleashed the largest stimulus package in its history in response to the 2008 crisis and slowing export markets in the west, it came at a price. Today China is grappling with a bill that some economists say has driven total debt to gross domestic product past 200%. While China offers the most extreme example of using debt to fund growth, it is a pattern that has been repeated across Asia. Without exports, central banks turned on the taps, leading to a jump in household and corporate borrowing. Now, as the US Federal Reserve considers a reversal of its ultra-loose monetary policy, the region faces a new challenge: coping with life after debt. And as investors gauge the impact of that transition, the ghosts of the 1997-98 Asian financial crisis have been reawakened. 'All this QE [quantitative easing] money has lead to a massive credit inflation bubble in Asia,' said Kevin Lai, chief regional economist at Daiwa Securities. 'The crime has been committed, we just have to deal with the aftermath. During that process there will be a lot of damage. It's like a margin call. Households will need to sell their assets. There will be a lot of wealth destruction."

August 19 - Bloomberg: "China's new home prices rose the most since January 2011 in the nation's four major cities, led by a 17% jump in Guangzhou and Shenzhen, on speculation the government will refrain from imposing tighter curbs. Beijing and Shanghai prices both increased 14% in July as 69 of 70 cities tracked by the government climbed from a year earlier... 'The new leadership seems to have a higher tolerance for rising home prices than the previous government,' Ding Shuang, a senior China economist at Citigroup Inc. in Hong Kong, said... 'It's unlikely that the government will issue nationwide curbs or ease policies. The government will likely aim at long-term policies by increasing more supply.'"

August 22 - Bloomberg: "Chinese manufacturing resumed expansion this month after shrinking the most in almost a year in July and output at European factories and services companies improved, a sign the global recovery is strengthening. A preliminary purchasing managers index for China by HSBC Holdings Plc and Markit Economics rose to 50.1 from 47.7..."

Japan Watch:

August 21 - Bloomberg (Arran Scott and Keiko Ujikane): "Bank of Japan Governor Haruhiko Kuroda said Japan's economy is strong enough to withstand a planned sales-tax increase, backing the measure before panels meet next week to study the impact on growth. The economy won't lose speed if the sales tax is raised as planned, Kuroda told the Mainichi newspaper in an interview published today. If a higher levy or changing conditions overseas heighten the risk of a slowdown, the central bank 'won't hesitate' to add to its unprecedented easing policy, Kuroda said..."

August 19 - Bloomberg (James Mayger and Andy Sharp): "Japan's exports jumped by the most since 2010 in July, aiding Prime Minister Shinzo Abe's efforts to drive an economic recovery even as rising energy costs boosted the trade deficit. Exports increased 12.2% from a year earlier after a 7.4% rise in June... Imports climbed 19.6%, leaving a trade deficit of 1.02 trillion yen ($10.5bn), the third biggest on record in data back to 1979."

India Watch:

August 21 - Bloomberg (Kartik Goyal): "India's central bank said it will buy long-dated government debt after cash-supply curbs to support the rupee prompted a surge in yields. Bonds and shares of lenders jumped the most in four years. The Reserve Bank of India will conduct open-market debt purchases of 80 billion rupees ($1.3bn) on Aug. 23 and 'thereafter calibrate them both in terms of quantum and frequency' based on market conditions... The earlier liquidity-tightening steps must not 'harden longer term yields sharply' and hurt lending, it said. India's 10-year bond yield touched 9.48% yesterday, the highest since 2001, as the nation struggles to curb capital outflows spurred by risks such as a record current-account deficit and speculation the U.S. Federal Reserve could taper stimulus."

August 22 - Bloomberg (Kartik Goyal): "The Reserve Bank of India said the nation's economic and monetary policies must preserve financial stability as the prospect of reduced U.S. Federal Reserve stimulus contributes to a slide in the rupee. Currency weakness could stoke already 'high' consumer- price inflation, the Reserve Bank said... Other challenges include a current- account deficit that exceeds sustainable levels, slowing growth, budget-deficit risks and rising bad loans at banks, it said. The rupee touched an unprecedented low today as concern the Fed will taper stimulus prompts investors to pull billions of dollars from emerging markets."

Asia Crisis Watch:

August 20 - Bloomberg (Shamim Adam and Kevin Hamlin): "Asia's role as the world's growth engine is waning as economies across the region weaken and investors pull out billions of dollars. The Indian rupee fell to a record low today, Thailand is in recession and Indonesian stocks have slumped about 20% since their peak. Chinese banks' bad loans are rising and economists forecast Malaysia will post its second straight quarter of sub-5% growth this week. The clouds forming in Asia as liquidity tightens and China's slowdown curbs demand for commodities and goods are fueling a selloff of emerging-market stocks, reversing a flow of money into the region in favor of nascent recoveries in the U.S. and Europe... 'The eye of the storm is directly above emerging markets now, two years after it hovered over Europe and four years after it hit the U.S.,' said Stephen Jen, co-founder of hedge fund SLJ Macro Partners... 'This could be serious for Asia.'"

August 21 - Bloomberg (Elffie Chew and Chong Pooi Koon): "Malaysia cut its forecast for growth this year after second-quarter expansion missed economists' estimates, adding pressure on policy makers to bolster confidence as the ringgit weakens. The economy may expand 4.5% to 5% in 2013, from a previous prediction of as much as 6%... Malaysia was swept along in the regional turmoil this week, as the prospect of reduced U.S. monetary stimulus and Asia's faltering growth outlook fueled a selloff of emerging-market stocks and currencies."

Latin America Watch:

August 21 - Bloomberg (Boris Korby, Raymond Colitt and Francisco Marcelino): "A year after it began, Brazil's municipal bond market has been brought to a standstill by the federal government after Credit Suisse Group AG and Bank of America Corp. provoked a backlash by collecting $140 million in fees from the first two borrowings... Brazilian Treasury officials, who approve state financing requests and provide guarantees backing loans, are starting to demand terms to curb the profits, seeking to protect taxpayers from being exploited and to limit their own borrowing costs while alienating bankers in the process. State officials at Mato Grosso and Parana say the demands are imperiling loans they're seeking from Credit Suisse, derailing a market the government had projected could grow to as big as $25 billion by 2014."

Global Economy Watch:

August 20 - Bloomberg (Jim Efstathiou Jr.): "A report from an international scientific team due next month will probably focus on a range of evidence that the Earth is warming rather than just changes in air temperature, according to a climate scientist who has seen drafts of parts of the study. The rate of polar ice melting, warming of oceans and the steady rise of sea levels all point to a planet heating up, said Kevin Trenberth, a senior scientist in the climate analysis section at the National Center for Atmospheric Research. He's a reviewer for the forthcoming United Nations climate report... 'There are other signs of warming that are abundantly clear,' Trenberth said... 'Those are some of the messages that I think might end up coming out of this report. It's really strong in areas other than just the global mean temperature or even regional temperatures around the world.'"

Europe Crisis Watch:

August 20 - Bloomberg (Rainer Buergin): "German Finance Minister Wolfgang Schaeuble said Greece will need a new aid program to reach its debt sustainability targets, while ruling out another debt cut. Speaking at an election event in the town of Ahrensburg near Hamburg today, Schaeuble said the first debt reduction for Greece was 'unique' and won't be repeated even as the country's economic situation remains difficult. 'There will have to be a program for Greece once again,' Schaeuble said... 'That's been said a long time ago. The public, the Bundestag have always been told.' Schaeuble's comments, made less than five weeks before German federal elections, are his clearest indication yet that the euro region will eventually resort to the 'further measures and assistance' for Greece that were agreed in principle by the bloc's finance ministers in November last year."

August 21 - Bloomberg (Scott Hamilton): "Britain posted its first July budget deficit since 2010 as an increase in government spending outstripped tax revenue. Net borrowing excluding temporary support for banks was 488 million pounds ($764 million) compared with a surplus of 823 million pounds a year earlier... Underlying tax receipts rose 3.4%, lagging behind a 3.7% increase in spending."

August 22 - Bloomberg (Saleha Mohsin): "Norway, western Europe's biggest oil and gas producer and home to a $760 billion wealth fund, is struggling to spur demand just as the rest of Europe surfaces from half a decade of economic pain. According to DNB ASA, the country's biggest bank, Norway will be the only European nation of the 15 it tracks whose economic growth won't accelerate next year... Norway, once a haven from Europe's debt turmoil, is failing to keep pace with recoveries in other developed markets. The $480 billion economy grew just 0.2% in the second quarter..."

Italy Watch:

August 22 - Bloomberg (Lorenzo Totaro and Chiara Vasarri): "Italian Prime Minister Enrico Letta's government will collapse if his Democratic Party votes to end Silvio Berlusconi's mandate as senator, a senior ally of the three-time premier said. 'If in a private company, a partner reports another one or tries to get rid of him, the business doesn't exist anymore,' Renato Brunetta, chief whip of Berlusconi's People of Liberty party in the parliament's lower house, said... The PD 'would provoke the government's fall,' he said."