Moneyization: The global financial phenomenon of individuals and businesses moving their funds to monies in which they have the highest confidence, or money which has a higher store of faith. |

Or, The Last Battles of Paper Debt

Last battle of paper assets is being fought. Paper assets appear to be losing. Real assets are continuing to gain ground as the grandeur of investing in paper fades slowly into history. Not many years ago investors were fed a huge dose of nonsense in the form of "Buy and Hold Strategy." As the first graph shows, it failed them. Now they gorge on trading schemes, paper and electronic. The results will be as dreary.

For Gold to be providing the higher return, money must be flowing into it from paper as s et s . Actually, decisions on several questions are being made. The answers for most lead to an investmort preference for Gold and Silver. First of these questions relates to what assets investors prefer to own. Investors are looking to the global changes t aking place and quite frankly do not see the preponderance of the equity markets offering the investments they desire.

Equity markets continue to be dominated by yes t erday's themes. Tomorrow's investment opportunities are not represented in the existing list of stocks, in large part. Yes, a few are able to nibble at the important trends of the future but not feed directly enough. Too much talk though of yesterday's technology darlings still dominates. Yesterday's popular technology plays are fading rapidly in economic importance, slowly moving to low margin businesses. For example if all the copies of MSFT software sold in the world are considered, the actual economic margin on those sales is far below what the company reports.

While many fund managers continue to be bogged in the names of yesterday and elaborate strategies doomed to failure, investors are moving on. Quite simply U.S.-based companies are not in the mainstream of today's economic shifts. Production and control of that production are moving to other countries. The global shift in the center of economic activity is away from North America and Western Europe.

Money around the world is trying to get in harmony with the trends of the future. Those trends include moneyization, China, and perhaps the finale for paper debt. Individuals have been and are shifting to stronger monies. Gold is simply one of them. China is a story well discussed, and clearly destined to be the epicenter of future economic activity. Investors are slowly moving to alternatives that match that shift. Commodity funds have become popular. Widespread is understanding that the Chinese renminbi might be a better money choice than the dollar. As of yet, investors can not buy the renminbi. Western financial markets as they are constructed today, do not offer the investment alternatives attuned to future.

Hedge funds losing money on "correlation trades" involving GM stocks and bonds are examples of the lack of real investment alternatives in markets. These funds do little if any investing, but focus on trading. Using computers to bet on red and black, CDOs, CDXs, or whatever is not investing. Today's trillion dollar hedge fund industry is simply creating fancy algorithms with the hope of beating the trading roulette wheel. The house will get their money, as it did with the GM trades. For good reason, trading of paper equities, derivatives and esoteric combinations of fictional financial vehicles will continue to provide inadequate returns. Lottery tickets have better odds.

Gold and Silver simply offer the best alternatives available. For that reason they have done better than equities. For that reason, those superior returns will continue into the future. Remember though that investment returns accrue over time, not every day or week or month. Until the Chinese economy is truly open for investment and until the dollar has its final crash, Gold should be the investment of choice for investors.

The bell has not rung yet on the Great Housing/Mortgage Paper Debacle. A bell did ring for the end of the technology bubble, but one had to be listening. Iridium Satellite was a multibillion scheme to provide satellite phone service to nearly every hill and dale in the world. Nice idea, but it was just a few years ahead of itself. The company failed in near silent solitude. In and of itself, the company's failure was not a monumental event. It was just a little bell that warned of the end of the technology stock bubble. We should all be listening for the tinkling of that little bell for the Housing Paper Debacle. Many will ignore the tinkling. Others will not be listening.

We do not know who will be the first left standing when music stops on Housing Paper. The source of the problem will be "debt." Someone owns that debt. Someone will lose an unimaginable amount of money in it. Who might be among the "someone" is t he really exciting question. When the mortgage debt implosion arrives, paper debt will be worth little. Fiat money is just debt of the government. In the case of the debt of the U.S., dollars, that debtor also will be striving to save itself from the billions of dollars of collapsing mortgage debt. The U.S. economy will be imploding. Who will be taken care of first? Those around the world that own those dollars? Or, those domestic firms hemorrhaging from mortgage debt gone sour?

Many have a decision to make. Should they continue to hold dollars? Should they continue to hold their national money? These worriers are not alone. Fiat money may be a serious financial casualty of the next paradigm. With China's currency not available, Gold and the Euro are what is left. Some of you have money destined for oblivion, and doing something about it now is appropriate.

About 117 distinctly different brands of national money exist in the world. Most of them make no economic sense, and have little reason for existing. Our second graph gives us a way of looking at these global monies. For each of those 117 brands of national money, the percentage each represents of the total global money supply has been calculated, based on the latest complete data available. As shown in the graph, the top five brands of national money represent about 80% of the global money supply. The next five brands of national money represent about 7%. The bottom 77 brands of national money represent a total of about 2% of the total world money supply.

Over time Darwin will take his toll on this structure of national monies. In the days before technology increased the speed of global finance, local money was needed. In today's world, local monies are not needed except for government imposed reasons. In the table below, the data for the top 11 money brands is presented. No need exists to discuss the rest. Investors have no business in the other brands of national money, except for filling scrapbooks for grandchildren to someday take to 'show and tell' at school.

Again, if your national money is not on this list, what you have is something that may someday have value to collectors. In short, some day it will not exist as money. Who else wants it? Where does it have use? In short, its functional domain is small and shrinking. Move your wealth and life to another brand of money. What about those on the list? Hong Kong will eventually converts to renminbi. Reason someday may develop in the UK, leading them to t he Euro. Switzerland eventually also goes Euro. Only reason for franc once being popular was financial privacy, the Gold backing and the inability to easily buy Gold. Those reasons are all fading. The dollar will fade as the UK pound has. Do you want to hold the dollar as it shrinks from over 20% of the world money supply to 7%, like the British pound?

| NATIONAL MONIES AS % GLOBAL MONIES(2003) | |

| Issuer Ranked by Size | % Total |

| US | 23 |

| EU | 21 |

| Japan | 20 |

| China | 9 |

| UK | 7 |

| Canada | 2 |

| Switzerland | 2 |

| Korea | 1 |

| Australia | 1 |

| Hong Kong | 1 |

| India | 1 |

At the present, the Euro is larger than the dollar. With Japan's economy in recovery that currency is likely to remain large. The world now has four large brands of national money, including Gold as one of them. When China joins fully the world economy and the renminbi becomes convertible, the Chinese brand of money will grow materially. In a number of years the renminbi may be competing with the Euro for money domination. In this coming battle for brand leadership between the renminbi and the Euro, how investors react is important. With collapsing dollar hegemony, this battle may simply be ignored. Investors and central banks after learning an expensive lesson on the value of debt and fiat money may indeed return to Gold.

In short, the world will have five large brands of money. The remainder are not necessary. Canada, so tied to the U.S., eventually will be forced to convert to U.S. dollar. Australia eventually uses the renminbi. Russia, and likely India too, move to the Euro. National monies representing 2% or less of world's money are not likely to rise to the top. If you are an investor in that group, two choices exist at the present: Gold or the Euro.

The central bank is the brand manager for a national money, or international money brand in the case of the top four. What we are seeking is a brand manager, central bank, that is aware of the world and the implications of its actions. Do we have that in the Federal Reserve? Many of us have been critical of the Federal Reserve's Housing Bubble Strategy. Federal Reserve policies of the past decade have resulted in the central banks of the world financing the deficit of the U.S. government. Had the Federal Reserve not created the problems with current account this situation would not exist.

That at some point the central banks of the world will have no choice but to let the dollar go where it may is generally now accepted. Central banks around the world have been financing the U.S. spending spree, as we well know. The Federal Reserve has not yet had to monetize the national deficit, but the trend seems to point in that direction. Inflation has moved up and the dollar has lost ground as central banks have simply slowed their buying. What will happen to U.S. inflation and the dollar as the Federal Reserve must increasingly fund the debt binge?

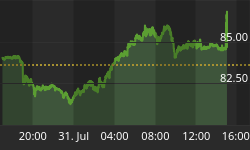

The longer term situation is well in place for Gold. Only crucial decision for investors is when to buy. Those times to buy Gold are when the optimism on the U.S. dollar has been pushed too far, as is the recent situation. Dollar optimism is to too high, and due for a sharp reversal. These are the times to buy Gold, as shown in the last graph. Now is the time to get on for the next leg of the journey to $1,300.