"Big surge in price of US homes fuels fears of bubble," writes the Financial Times newspaper. Meanwhile, another major news wire did a weekend report on the top 10 U.S. cities most susceptible to a hit in the event of a burst housing bubble. But what has been mostly overlooked has been the possibility that yet another wave of mortgage refinancing may be imminent, thanks in part to the fresh new lows in the 10-year Treasury yield, which mortgage rates are keyed off of.

Now that interest rates have once again taken center stage, a story of major proportions seems to be unfolding. A financial television commentator was overhead suggesting that a "new wave of mortgage refinancing could begin" with the new lows being made in the long-term interest rates. This is definitely a big development that must be followed closely in the coming weeks...

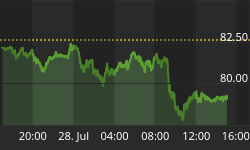

The bond market provided a preview of what could be even lower yields in the coming weeks/months ahead last week. In my commentary of May 21 entitled "The stock market and interest rate conundrum" I wrote, "My work on the 10-year Treasury Yield Index (TNX) tells me something interesting. Currently 41.25...it won't be long before TNX encounters a strong downward wave of resistance that will probably take the index lower over the next couple of months to as low as the 36.0-to-38.00 area before strong support is encountered. This area was last visited in March of 2004." As of this writing on June 3, TNX had visited the 38.00 area on an intraday basis, much sooner than expected, but the chance of a move further down to 36.00 in coming weeks is still high.

The rate of change slowdown in the monetary aggregates has been well documented by a host of analysts and observers in recent months. The lingering question everyone is asking seems to be, "How will the household economy survive the seemingly imminent economic contraction?" which the money supply slowdown is sure to evoke. Another round of mortgage refinancing could be just the (temporary) solution consumers need at such a critical time.

There are many ways in which a mortgage refinancing wave would help keep consumers solvent in the event of another mini-recession between now and 2006. As one analyst observed, "The corresponding decline in mortgage payments will help alleviate the financial pressure of large household debt burdens. This might keep a lid on net-chargeoffs due to bankruptcies as we move through this slow-growth economic period."

A reader recently sent me an e-mail which I think summarizes the current situation nicely: "Americans are addicted to credit-based spending and cannot be weaned from this addiction. They have the urge to spend, even if it means going further into debt. The market will allow them to continue this urge even in the face of a global economic slowdown by simply borrowing against home equity."

Another reader writes, "I have just read your article about the reasons why the housing bubble has been created. What I do not understand is how this will provide real wealth for those retiring. Is everybody meant to sell and cash up at the same time to a bunch of cashed up Chineese? If so where do they then live? I must be missing something, can you please explain how this works."

The observations made above are not a major concern of the financial controllers right now as there only interest is the complete integration of the global economy with American providing the chief engine leading the way toward total globalism. Once America has performed its task it will be assigned its role in the global economic framework with a lower standard than the one we've become accustomed to. (This necessarily follows based on the law of averages since those countries with the lowest rates of economic performance will necessitate a lowering of the average for all countries that are part of the global framework. More on this in a future commentary.)

With American's chasing the rate of highest return, real estate is now the only game in town. All their financial eggs are in one housing and property market basket, and for this reason the bubble will be protected from bursting in dramatic fashion in the coming months simply because the powers-that-be can ill afford this with the global economic integration effort not yet complete.

While the expectation of some economists of a decoupling of the rest of the world from the so-called "U.S.-centric" global economy is strong, this will most likely have to wait until after the next long-term cycle bottoms (namely the 8-year cycle) in 2006 and probably until 2009 when the last of the dominant Kress cycles peak. Until then - and as long as real estate forms the basis of U.S. consumer wealth - the real estate bubble will be jealously guarded with gamesmanship and monetary policy.