Quite a year.

All 2013 year-to-date price changes are as of the December 27th , but will be updated after the close on December 31.

In a CBB titled "Do Whatever it Takes" back in August 2012, I discussed a television program I had viewed (sometime back) that provided an intellectual framework for better understanding the escalation of aerial attacks against civilians during World War II.

From "Do Whatever it Takes:" "In September of 1939, President Roosevelt issued an "Appeal... on Aerial Bombardment of Civilian Populations" to the governments of France, Germany, Italy, Poland and Britain"... As the war commenced, efforts were indeed made by most "belligerents" to limit aerial attacks to military targets away from innocent civilians. It wasn't long, however, before civilian deaths mounted as bombs were unleashed ever closer to population centers. And then not much time elapsed before industrial targets were viewed as fair game, with civilians paying a progressively devastating price. Somehow, an increasingly desperate war mindset saw targeting population centers in much less unacceptable terms. Soon it was perfectly acceptable. War-time justification and rationalization saw conventional bombing of civilian targets regress into direct firebombing and incendiary raids on major cities in Europe and Asia. Less than six years passed between President Roosevelt's "Appeal" and the dropping of nuclear bombs on Hiroshima and Nagasaki."

My worst fears from the summer of 2012 central banker "Do Whatever it Takes" chorus came to fruition in 2013. The Fed injected a Trillion dollars (BOJ providing somewhat less) of new "money" directly into overheated financial markets in a non-crisis environment. And following several years of mind-numbing escalation, this year's egregious monetary inflation was met with nary a protest. To be sure, "war time" rationalizations and justifications turned more creative and sophisticated, as previously unimaginable monetary measures were heralded as "enlightened."

For the year, the Fed's balance sheet ballooned 37% to surpass $4.0 TN. Bank of Japan assets surged 42% to exceed $2.0 TN. From my analytical framework, it can be described only as "a year living dangerously." As he led the Federal Reserve deeper into the untested waters of contemporary monetary inflation, chairman Bernanke took time to proclaim Japan's parallel inflationary policy a case of "enrich thy neighbor" (in contrast to Depression-era "beggar thy neighbor").

As destabilized, speculative markets tend to do, they mounted an unpredictable reaction to the Trillions of new global liquidity. In most cases, global bond prices actually declined (yields rose). And emerging markets (EM) generally performed unimpressively at best. Back in 2012, QE2 funneled liquidity into the hot Treasury, MBS and emerging markets. In striking contrast, QE3 hit with cracks surfacing in bonds and EM. This ensured liquidity raged into Bubbling equities - the new speculative vehicle of choice. On the one hand, central bank liquidity accommodated record bond fund outflows, ensuring yield increases were contained and that markets did not dislocate. On the other hand, the new white-hot asset class (equities) could enjoy huge ("great rotation") flows without fretting over a possible bursting bond Bubble market accident.

Despite massive Fed buying, Treasury and MBS yields moved upward. After beginning the year at 1.76%, 10-year Treasury yields surged 124 bps to 3.00%. Treasury long bond yields jumped 99 bps to 3.94%. Benchmark 30-year MBS yields surged 138 bps to 3.61% (30-year conventional mortgage rates up 113 bps y-o-y to 4.48%). Not even short rates were immune to upward pressure, as two-year government yields rose 14 bps to 0.39% and five-year T-note yields jumped 101 bps to 1.74%.

Rising yields were a global phenomenon. Canadian 10-year yields jumped 100 bps to 2.77%. U.K. 10-year sovereign yields jumped 125 bps to 3.07%. German bund yields jumped 64 bps to 1.95% and French 10-year yields gained 57 bps to 2.57%. Australian 10-year yields jumped 100 bps in 2013 to 4.27%, and New Zealand yields surged 121 bps to 4.75%.

There is a misperception that inflation was a nonissue in 2013. Yet throughout key EM economies, advancing inflation was among the problematic manifestations resulting from protracted Credit and speculative excesses. In short, EM economies generally saw inflationary pressures rise as real growth slowed markedly in the face of ongoing rapid Credit expansions. This created an unappealing environment for global investors, with the more sophisticated "hot money" heading toward the exits.

Brazil's local (real) sovereign yields surged 393 bps in 2013 to 13.10%, while some major bankruptcies took a heavy toll on Brazilian corporates. Political instability contributed to the 379 bps jump in Turkish (lira) 10-year yields, to 10.35%. Mexican yields rose 116 bps to 6.50%. Indonesia was an EM problem child, as 10-year yields surged 314 bps to 8.33%. India confronted a worsening inflation backdrop, with 10-year yields jumping 91 bps to 8.95%. Inflationary pressures also hurt Russian bonds, as 10-year sovereign yields jumped 91 bps to 7.81%.

For the most part, EM currencies suffered. On the downside, the Argentine peso declined 24.3%, the Indonesian rupiah 20.1%, the South African rand 19.5%, the Turkish lira 17.2%, the Brazilian real 12.3%, the India rupee 11.1%, the Chilean peso 8.6%, the Peruvian new sol 8.7%, the Colombian peso 8.4%, and the Philippine peso 7.6%.

EM equities for the most part also underperformed. Brazil's Bovespa dropped 15.9% and Turkish equities were hit for 18.3%. Stocks in Indonesia (down 2.4%) and Thailand (down 6.7%) posted 2013 declines. South Korean equities were little changed. Meanwhile, India (up 9.1%), Taiwan (up 10.9%) and Hong Kong (up 2.6%) posted modest gains. Eastern European equities were mostly lower. On the downside, Ukraine stocks fell 10.3%, with Russian equities down 5.3%. Stocks were mixed in Poland and Hungary, while declining in the Czech Republic. Stocks rose in Bulgaria and Romania.

As "King of EM", circumstances in China deserve special attention. First and foremost, Chinese Credit and economic Bubbles inflated to new extremes in 2013. After a couple years of cautious measures ("tinkering") intended to restrain housing inflation and general Credit excess, Chinese authorities were compelled in June to move more forcefully to rein in Bubble excess. As is always the case, missing the timing for needed monetary policy restraint comes with a price. By this past June, China's Bubble economy had begun to slow in the face of rising inflation and escalating financial excess. Belated efforts to rein in a runaway Bubble immediately confronted acute financial and economic fragilities - and policymakers quickly reversed course. The Chinese Credit Bubble bounced back as strong as ever. And as the year came to a close, it appeared Chinese officials were again attempting to impose some restraint.

In one of history's most spectacular Bubbles, total 2013 Chinese Credit growth will approach $3.0 TN. The year will see record mortgage Credit growth and likely record growth in China's ballooning "shadow banking" system. On a hypothetical chart of systemic risk, surging volumes of progressively riskier loans ensure a parabolic spike in risk at the late "terminal phase" of Credit Bubble excess. Clearly, much of China's risky Credit has been intermediated through "trust deposits," "wealth management" instruments and other opaque "shadow banking" vehicles. Indeed, 2013 saw an increasingly dangerous disconnect between the deteriorating quality of Credit and the perception of safety for holders of myriad liabilities throughout the Chinese banking system - both traditional and "shadow" varieties.

It's worth noting that Chinese market yields rose in 2013. After beginning the year at about 60 bps, China sovereign CDS spiked to a high of 140 in June (before ending the year at 79). Chinese sovereign yields jumped 100 bps to 4.62%. Notably, Chinese corporate yields jumped to multi-year highs as the world began to take a dimmer view of Chinese micro and macro fundamentals.

For China, 2013 was the year of the "tions": inflation, pollution and corruption. There were growing pockets of unrest, as segments of the population increasingly question the quality of their air, food, government and lives. Dissent was met with a harsh crackdown on bloggers, journalists and dissidents. The new Xi Jinping government moved to combat corruption while planning for deeper economic reform, hoping to placate a population that has seen expectations inflate right along with its Credit system, apartment prices and economy.

The long-awaited audit report of local Chinese government debt is said to be imminent. The Chinese Academy of Social Sciences think tank this week reported that local government debt had doubled in two years to end 2012 at $3.3 Trillion.

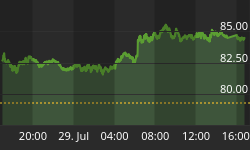

Here at home, the Fed has once again badly missed its timing and, in the process, further emboldened precariously speculative markets. From November trading lows to mid-May highs, the S&P 500 surged 25% (small caps up 32%). Excess throughout the corporate debt market were similarly conspicuous by the spring. The Fed needed to immediately conclude QE - and chairman Bernanke did state in May the Fed's intention to begin winding down the program. Yet not only did some market tumult have the Fed abruptly reversing course, chairman Bernanke went so far as to state the Fed would be ready to "push back" (with only larger QE) against any tightening of financial conditions. This was another costly policy blunder. The Fed's $85 billion of monthly market liquidity coupled with Bernanke's promised market backstop provided the ultimate flashing green light for equities speculation. From June trading lows, the S&P 500 surged another 18% in just over six months (small caps up 23%).

The Fed's skittish tapering reversal put an exclamation point on five years of unprecedented market interventions and distortions. The Federal Reserve and global central banks have provided profound advantages to speculating on the long side while severely impairing the shorts. On the one hand, a major squeeze (shorts forced to buy back stocks at rising prices to close out losing positions) has provided important fuel for the equities rally. On the other, with the depleted shorts largely out of the way, the emboldened longs could easily push stock prices higher - confident of a limited supply of stock to be sold in the marketplace. It was all too reminiscent of late-'90's market speculation, dislocation, manipulation and melt-up. Why not buy large quantities of out-of-the-money call options and then gun the stock market into year-end?

It was definitely the year of the short squeeze. The Goldman Sachs Most Short index surged 45.1%. Herbalife, surely the highest profile squeeze of 2013, enjoys a 2013 gain of 138%. The heavily-shorted solar stocks enjoyed big squeezes. Sunpower gained 414%, Solarcity jumped 377% and SunEdison 299%. The marketplace was equally smitten with 3D printing. 3D Systems jumped 155% and Stratasys rose 61%. Elsewhere, Netflix jumped 296%. Zillow rose 191% and TripAdvisor 95%. Micron Technologies jumped 239% and Best Buy 239%. Facebook advanced 108% and Yahoo! 103%. Tesla surged 346%.

In my now 24 years in the industry, I've witnessed my share of market exuberance and excess. Yet 2013 took speculation to a new level. I have argued the breadth of excess throughout U.S. equities surpassed even 1999. The S&P 500 returned (including dividends) 31.9%, while the S&P400 Midcaps returned 32.8% and the Russell 2000 small caps returned 38.5%. The Value Line Arithmetic (average stock) posted a 2013 gain of 37.7% (compared to 1999's 10.6%). The NYSE Arca Securities Broker/Dealer index gained 68.5%. The NYSE Arca Biotechnology index rose 51.5%. The Dow Jones Transports surged 38.5%, and the Morgan Stanley Cyclical Index gained 40.6%. The Philadelphia Semiconductor Index jumped 38.0% and the KBW Bank Index rose 34.7%. The Nasdaq Composite surged 37.8%, with the Nasdaq Industrial Index up 42.4% and the Nasdaq Bank Index gaining 39.3%. It will take a strong Q4 to push real 2013 U.S. GDP to 3%.

Somewhat ironically, it became an almost ideal backdrop for corporate Credit excess - perhaps the "perfect (speculative) storm." With Treasury, MBS and muni yields moving higher, bond funds suffered huge (over $70bn, surpassing '94's record) outflows. Yet Fed liquidity was there to readily finance the "great rotation" into corporate equities and debt securities, in the process providing a major boon to corporate Credit. The ongoing global yield grab ensured abundant liquidity flowed to junk, leveraged loans and other higher-risk corporate Credits. Rising rate concerns also stoked major flows into floating-rate debt funds and products, further bolstering the corporate liquidity bonanza. Unconventional "bond" funds, profiting handsomely from collapsing corporate risk premiums and other derivative bets, also enjoyed big inflows.

Measures of corporate Credit risk collapsed to levels last seen during booming/"still dancing" 2007. A widely followed index of investment-grade Credit default swap (CDS) prices sank to 63 bps (low since 10/'07) after beginning the year at 95 bps. And index of junk CDS collapsed 175 bps to 312 bps (low since 6/'07). The corporate debt market literally succumbed to panic buying, and I'll assume that the booming corporate Credit derivatives marketplace played a prominent role. Writing corporate Credit ("flood") insurance was an extraordinarily profitable undertaking in 2013. Leveraging in high-yield corporate debt was a home run. The Fed, the leveraged speculators and our desperate savers created a backdrop of essentially unlimited corporate Credit availability. And borrowers lined up.

The year 2013 saw record ($1.52 TN from Bloomberg) U.S. corporate debt sales. For the second straight year, investment-grade debt issuance set annual an annual record ($1.125 TN). Junk bond issuance ($360bn) set a new record, with record sales of payment-in-kind (PIK) and "cov-light" bonds. Junk-rated loan volumes surged to a record $683 billion, surpassing 2008's $596 billion (according to Standard & Poor's Capital IQ Leveraged Commentary and Data). Total global corporate bond issuance surpassed $3.0 TN. Global speculative-grade bond sales approached an unprecedented $500 billion (from S&P). Global IPO volumes jumped 37% from 2012 to $160 billion (from S&P).

At $233bn, private-equity buyouts reached their highest level since 2007 (Dealogic). The U.S. IPO market enjoyed its strongest issuance year since 2007. A total of 229 deals raised $61.7bn, with dollars raised up 31% compared to 2012. And it's certainly worth noting that hedge fund assets increased more than $360 billion during the year to reach a record $2.70 TN (from Prequin), despite ongoing ("crowded trade") performance issues.

And, of course, the more conspicuous the financial Bubble the more boisterous the bullish propaganda arguing that Bubble talk is ridiculous. Our central bank has clearly learned nothing from earlier crises. Rather than moving to tighten monetary policy, the FOMC near year-end stated their intention to pump at least another $500 billion into the markets, while promising to keep rates at near zero for some time to come.

U.S. corporate debt growth should approach 9.0% during 2013, the strongest pace since 2007's 13.5%. But even with heady corporate borrowings, total U.S. non-financial debt growth will likely slow in 2013 to less than 4% (down from 2012's 4.9%). With municipal bonds posting their worst year since 1994, Credit conditions tightened throughout much of muni finance. And with the Household sector still reluctant to take on significant additional debt, the overall Credit backdrop remained potentially problematic for economic growth, corporate earnings and inflated asset markets. Yet for 2013, the Fed's $1 TN monetary inflation again countermanded normal system behavior and relationships - most notably further inflating securities and asset prices.

In the end, over-liquefied and booming financial markets, with attendant massive inflation of perceived household wealth coupled with extremely loose corporate Credit, provided some momentum to the real economy. The Fed remained fixated on potential fragilities, again choosing to completely turn its back from the type of Bubble Excess responsible for what have become hopelessly interminable fragilities.

The OECD forecasts only 2.7% global growth for 2013. Cracks in China, Brazil, India and other EM economies, the previous global "growth locomotives," have created a tenuous backdrop. The popular global "reflation trade" came under intense pressure in 2013. Gold bullion sank 28%, with the NYSE Arca Gold BUGS Index (HUI) collapsing 55.4%. Resilient energy prices contained losses to the major commodities indices. Yet corn sank 39%, silver 34%, Canola 29%, wheat 22%, soybean oil 19%, coffee 19%, nickel 17% and aluminum 16%. The "commodities" currencies were hit, with the South African rand down 19.5%, the Australian dollar 14.7%, the Brazilian real 12.3% and the Norwegian krone 9.5% and the Canadian dollar 7.3%.

The dismal performance of the commodities complex in the face of massive QE caught most by surprise. My own view holds that 2013 saw major cracks develop in the global Bubble with the onset of financial and economic fragilities in China, Brazil and EM more generally. Fed and BOJ liquidity only exacerbated instabilities. Increasingly powerful equities Bubbles in New York, Tokyo and Frankfurt added to the magnetic pull away from EM, while fostering greater uncertainty for developed world economic prospects. To be sure, QE had a profound impact on the performance-chasing and trend-following global leveraged speculating community with assets measured in the many Trillions. As equities took off, caution - along with gold and other perceived safe havens - were thrown to the wind.

Surging Japanese stock prices were fueled by enormous Bank of Japan "money" printing and the resulting 17.5% yen (vs. the dollar) devaluation. Japan's Nikkei equities index posted a historic advance (up 55.6%).

Despite ongoing economic stagnation, 2013 saw European markets somewhat win by default. The euro was the strongest performing major global currency (up 4.2% vs. the dollar). The German DAX equities index jumped 26% to a record high, with the CAC 40 gaining 17.5% in the face of weak French economy. Especially after faltering EM bond markets fell out of favor, "periphery" European bonds (backstopped by the Draghi ECB) became a favored high-yield target for the global speculator community. Greek bond yields sank 226 bps this year (to 8.21%), with 10-year sovereign yields in Spain down 106 bps to 4.21%; Portugal down 70 bps to 5.96%; and Italy down 29 bps to 4.21%. Despite moribund economies, Spanish equities were up 21.1% in 2013 and Italian stocks gained 16.5%. I'd be curious to know the scope of leverage in European debt (and elsewhere!) financed by borrowing in or shorting the yen ("yen carry trade").

As an analyst of Credit, Bubbles and markets, 2013 was extraordinary. There was historic Credit growth (China), historic central bank monetary inflation (Fed, BOJ) and incredible speculative excess (U.S. equities & corporate debt, Japanese equities). The year provided abundant confirmation of the global Bubble thesis. In particular, the May/June period of market tumult illuminated mounting vulnerabilities. Five years of extreme monetary stimulus has spurred Trillions of flows into markets, products and instruments with significantly greater risk than generally perceived. There has as well been a proliferation of perceived low-risk strategies that incorporate varying degrees of leverage.

The May/June period gave a hint of how quickly latent instabilities can manifest when market downturns incite a reversal of flows. In particular, some ETFs and various "risk parity" strategies demonstrated how quickly perceived highly liquid markets can prove liquidity-challenged. Central bank liquidity provided a great deal of market balm throughout 2013. It also further inflated dangerous Bubbles that will ensure a fascinating 2014.

For the Week:

The S&P500 advanced 1.3% (up 29.1% y-t-d), and the Dow rose 1.6% (up 25.8%). The S&P 400 Midcaps rose 1.3% (up 31.0%), and the small cap Russell 2000 gained 1.3% (up 36.7%). The Banks rose 1.1% (up 34.7%), and the Broker/Dealers added 0.7% (up 68.5%). The Morgan Stanley Cyclicals were up 2.1% (up 40.6%), and the Transports gained 1.0% (up 38.5%). The Utilities slipped 0.3% (up 7.7%). The Nasdaq100 advanced 1.2% (up 34.3%), and the Morgan Stanley High Tech index gained 1.3% (up 31.0%). The Semiconductors jumped 1.5% (up 38.0%). The Biotechs surged 2.4% (up 51.5%). With bullion gaining $10, the HUI gold index rallied 4.3% (down 55.4%).

One-month Treasury bill rates ended the week at zero, and three-month rates closed at 6 bps. Two-year government yields were up a basis point to 0.39%. Five-year T-note yields ended the week 6 bps higher to 1.74%. Ten-year yields rose 11 bps to 3.00%. Long bond yields jumped 11 bps to a 29-month high 3.94%. Benchmark Fannie MBS yields were up 9 bps to 3.61%. The spread between benchmark MBS and 10-year Treasury yields narrowed 2 bps to 61 bps. The implied yield on December 2014 eurodollar futures increased 1.5 bps to 0.425%. The two-year dollar swap spread increased 2 to 10 bps, while the 10-year swap spread declined one to 6 bps. Corporate bond spreads narrowed further. An index of investment grade bond risk declined one to 63 bps (low since October '07). An index of junk bond risk fell 7 bps to 312 bps (low since June '07). An index of emerging market (EM) debt risk dropped 7 bps to 307 bps.

Debt issuance came to a virtual halt for the holidays. Investment grade issuers included Fei Xiang Two LLC $295 million and Questar Gas $60 million.

I saw no junk, convertible debt or international dollar debt issues this week.

Ten-year Portuguese yields were unchanged at 5.96% (down 79bps y-t-d). Italian 10-yr yields jumped 9 bps to 4.21% (down 29bps). Spain's 10-year yields rose 8 bps to 4.21% (down 106bps). German bund yields gained 8 bps to a three-month high 1.95% (up 63bps). French yields jumped 11 bps to 2.57% (up 57bps). The French to German 10-year bond spread widened 3 to a 23-week high 62 bps. Greek 10-year note yields were down 17 bps to 8.18% (down 229bps). U.K. 10-year gilt yields jumped 13 bps to a 28-month high 3.07% (up 125bps).

Japan's Nikkei equities index jumped 1.9% to a more than six-year high (up 55.6% y-t-d). Japanese 10-year "JGB" yields rose 2 bps to a three-month high 0.69% (down 9bps). The German DAX equities index jumped 2.0% to a new record high (up 26.0%). Spain's IBEX 35 equities index surged 2.2% (up 21.2%). Italy's FTSE MIB index rose 2.1% (up 16.5%). Emerging markets were mostly higher. Brazil's Bovespa index increased 0.2% (down 15.9%), and Mexico's Bolsa gained 1.3% (down 2.2%). South Korea's Kospi index gained 1.0% (up 0.3%). India's Sensex equities index added 0.5% (up 9.1%). China's Shanghai Exchange rallied 0.8% (down 7.4%). Turkey's Borsa Istanbul National 100 index sank 8.2% (down 18.3%)

Freddie Mac 30-year fixed mortgage rates added a basis point to a new three-month high 4.48% (up 113bps y-o-y). Fifteen-year fixed rates increased one basis point to 3.52% (up 87bps). One-year ARM rates slipped a basis point to 2.56% (unchanged). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed rates up 6 bps to 4.63% (up 55bps).

Federal Reserve Credit expanded another $27.1bn to a record $3.986 TN. Over the past year, Fed Credit was up $1.080 TN, or 37.2%.

Global central bank "international reserve assets" (excluding gold) - as tallied by Bloomberg - were up $693bn y-o-y, or 6.8%, to a record $11.540 TN. Over two years, reserves were $1.316 TN higher for 13% growth.

M2 (narrow) "money" supply gained $5.0bn to a record $10.977 TN. "Narrow money" expanded 5.7% ($588bn) over the past year. For the week, Currency increased $1.3bn. Total Checkable Deposits gained $4.4bn, while Savings Deposits declined $2.8bn. Small Time Deposits added $1.3bn. Retail Money Funds increased $0.8bn.

Money market fund assets jumped $22.1bn to $2.697 TN. Money Fund assets were up $30bn from a year ago, or 1.1%.

Total Commercial Paper jumped $15.5bn to an almost 11-month high $1.101 TN. CP was up $35bn over the past year, or 3.3%.

Currency Watch:

The U.S. dollar index slipped 0.2% to 80.39 (up 0.8% y-t-d). For the week on the upside, the Brazilian real increased 2.1%, the Swedish krona 1.1%, the British pound 0.9%, the South Korean won 0.7%, the euro 0.6%, the Swiss franc 0.5%, and the Norwegian krone 0.2%. For the week on the downside, the South African rand declined 1.6%, the Japanese yen 1.0%, the Canadian dollar 0.7%, the New Zealand dollar 0.6%, the Mexican peso 0.6%, the Australian dollar 0.6% and the Singapore dollar 0.2%.

Commodities Watch:

The CRB index increased 0.4% this week (down 3.7% y-t-d). The Goldman Sachs Commodities Index gained 0.6% (down 0.9%). Spot Gold recovered 0.8% to $1,213 (down 28%). March Silver rallied 3.1% to $20.05 (down 34%). February Crude gained $1.00 to a 10-week high $100.32 (up 9%). January Gasoline rose 1.2% (up 2%), while February Natural Gas declined 2.2% (up 30%). March Copper rallied 2.3% (down 7%). March Wheat declined 0.7% (down 22%), and March Corn fell 1.3% (down 39%).

U.S. Fixed Income Bubble Watch:

December 23 - Bloomberg Sridhar Natarajan and Krista Giovacco): "The amount of loans to the riskiest U.S. companies ballooned to a record this year, propelled by unprecedented demand for floating-rate debt that offers protection from rising interest rates. The market for junk-rated loans increased to $683 billion, exceeding the 2008 peak of $596 billion, according to Standard & Poor's Capital IQ Leveraged Commentary and Data. The $130 billion surge this year was fueled by borrowings that don't include typical lender protections such as limits on leverage. Loans, which suffered the biggest losses in the fixed- income market during the financial crisis, staged a comeback as investors funneled a record $64.4 billion into funds that buy the debt in anticipation the Federal Reserve would start unwinding its bond buying... The demand has enabled companies take on more debt for shareholder rewards, prompting regulators to warn that the excesses which contributed to the credit crisis may be creeping back. 'The worst deals are made in the best of times is a phrase we hear often,' Frank Ossino, a money manager... who oversees $2.5 billion of loans at Newfleet Asset Management LLC, said... 'While the default environment will remain low, ever more aggressive transactions become the seeds of the next default cycle.'"

December 25 - Wall Street Journal (Mike Cherney): "Municipal bonds are on track to post their worst annual performance in nearly two decades as 2013 ushered in more financial woes for U.S. cities. Municipal debt is down 2.58% so far this year... Bonds from states, cities and counties are having their worst year since 1994, when interest rates spiked. Bond markets have sold off broadly this year as investors braced for the Federal Reserve to start dialing back easy-money policies that had supported credit markets since the financial crisis."

December 27 - Bloomberg (Michael B. Marois and Brian Chappatta): "California is poised to reclaim its spot as the biggest borrower in the municipal market after an improving budget outlook propelled the state's debt in a year when taxes rose for its wealthiest residents. California and its localities have sold $46.2 billion of long-term bonds in 2013 through Dec. 20, up about 13% from last year's pace... That puts the Golden State atop New York for the first time since 2010."

December 26 - Bloomberg (Matt Robinson): "Credit quality for U.S. companies is showing signs of weakening as issuers from Verizon Communications Inc. to Apple Inc. borrow unprecedented amounts of money to expand and reward shareholders. A total of 223 companies had their bond ratings cut by Moody's... in the six months ended November, compared with 172 increases, the highest proportion of downgrades since April. Issuers took advantage of borrowing costs that averaged a record-low 3.83% this year to sell an unprecedented amount of bonds, with 15% of offerings funding shareholder payouts, the most in five years."

Federal Reserve Watch:

December 24 - MarketNews International (Heather Scott): "Dallas Federal Reserve Bank President Richard Fisher... said he argued in favor of starting the pullback in the massive asset purchase program with a $20 billion cut, but said it was important to get the taper started... 'I think the market could have digested that,' Fisher told Fox Business... 'We'll just have to see how the economy proceeds.' Fisher, who will be a voting member of the Federal Open Market Committee in 2014 and has long advocated slowing the asset purchases... He repeated his concerns about the potential for the program to serve as 'kindling for future inflationary pressure," and although the Fed has an exit plan, 'It's become very complicated.' Although the Fed has helped to underpin a recovery, including improving home prices, 'the issue is how much (liquidity) is out there that we're going to have to sop up, and I'm frankly concerned about that over time but we're going to work hard to do it properly.'"

U.S. Bubble Economy Watch:

December 24 - Wall Street Journal (Steven Russolillo): "U.S. companies are showering cash on shareholders, powering the stock market's record-breaking rally. Share buybacks and dividends are reaching levels unseen since before the financial crisis, as persistent economic uncertainty prompts cash-rich companies to reward shareholders rather than invest in other activities. U.S. companies in the S&P 500-stock index bought back $128.2 billion of their own shares in the third quarter... That is the highest level since the fourth quarter of 2007. Combined, stock buybacks and dividends totaled $207 billion in the third quarter, also the highest in nearly six years..."

December 24 - Dow Jones (Matt Jarzemsky): "The last major initial public offering of 2013 closed its books this week, ending a long-awaited banner year for IPOs. This year saw 229 U.S.-listed IPOs come to market, up from 145 in 2012, according to Dealogic. The offerings raised $61.7 billion, up 31% from a year earlier and the biggest annual haul since 2007. Investors buying the newly minted stocks were rewarded, as well. Through Wednesday, shares of companies that went public this year were up 33%, on average, from their offer price."

December 24 - Bloomberg (Prashant Gopal): "U.S. house prices rose 0.5% in October from September as buyers competed for a tight supply of properties for sale... Prices climbed 8.2% from a year earlier, the FHFA said..."

December 24 - Reuters: "Applications for U.S. home mortgages fell for a second week and hit a 13-year low as mortgage rates rose due to a bond market sell-off following the Federal Reserve's decision to pare its bond purchase stimulus in January... The Mortgage Bankers Association said its seasonally adjusted index of mortgage application activity, which includes both refinancing and home purchase demand, fell 6.3% to the lowest level since December 2000. Mortgage applications have fallen sharply since this summer on a jump in home finance costs as benchmark Treasuries yields eventually rose to a two-year high."

December 24, 2013 - Wall Street Journal (Justin Baer and Julie Steinberg): "A strong rally in financial markets over the past two months is expected to add a last-minute boost to bonus packages for Wall Street's traders and investment bankers... The winners in financial firms this year are likely to be equity traders, who have reaped gains from soaring stock markets, and investment bankers, who have benefited from a pickup in initial public offerings and other deals. But the recent rally is unlikely to provide much help to bond traders, who have endured one of their toughest years since the financial crisis."

Global Bubble Watch:

December 24 - Bloomberg (Katya Kazakina and Scott Reyburn): "The priciest segment of the art market surged to record highs in 2013 amid demand from established collectors and wealthy new buyers from emerging- market economies. The top 10 auction lots of 2013 raised $752.2 million, a 27% increase from 2012 and an 82% jump from 2011... Every item in the group fetched more than $45 million. In November, Christie's International Plc sold $692 million of art in less than three hours, the highest auction tally ever. 'The top end of the market used to be $10 million; now it's $50 million,' said Philip Hoffman, chief executive of the London-based Fine Art Fund. 'The auction houses are getting new super-rich clients from China, Russia and the Middle East. These are very wealthy families and they want something amazing.' Collectors are bidding up art prices as easy-money policies among central banks and rising global stock markets boost the fortunes of the world's richest people. The combined wealth of the top 200 billionaires has surged by $422.2 billion this year through Dec. 20, according to the Bloomberg Billionaires Index."

December 23 - Bloomberg (Leslie Picker, Ruth David and Joyce Koh): "Twitter Inc. and Hilton Worldwide Holdings Inc. helped lead the best year for U.S. initial public offerings since the financial crisis, with strong trading debuts likely to stoke investor demand for new shares in 2014. Companies raised about $22 billion in U.S. IPOs in the fourth quarter, bringing the total for the year to $56 billion, the most since 2007, according to data compiled by Bloomberg. Sales in Europe and Asia also rose sharply, with global deals tripling from the prior three months... Companies will raise as much as $225 billion through IPOs globally next year, with about $75 billion in the U.S., according to estimates by Joe Castle, global head of equity syndicate at Barclays... That compares with about $190 billion globally -- including real estate investment trusts, special-purpose acquisition companies and closed-end funds -- in 2013..."

December 27 - Bloomberg (Sarika Gangar): "Corporate bond sales slipped from a record pace in 2013 as the slowest year in Europe since 2002 offset unprecedented U.S. issuance stoked by borrowers seeking to get ahead of the Federal Reserve's stimulus cuts. Sales of $3.78 trillion in 2013 fell 5.5% from last year's $4 trillion, an all-time high... European debt offerings plummeted 6% to 786.2 billion euros ($1.1 trillion) with financial institutions curbing issuance as they bolstered their capital while sales by U.S. issuers... reached an all-time high of $1.52 trillion."

December 27 - Bloomberg (Lucy Meakin): "Investors with more than $2 trillion of assets are shunning U.K. government bonds as a revitalized economy and waning demand for haven assets inflicts the worst losses on holders in almost 20 years. Gilts lost 4% this year through Dec. 23..."

EM Bubble Watch:

December 21 - Financial Times (Christopher Thompson): "Emerging market debt funds saw their biggest outflows in nearly half a year ahead of the US Federal Reserve's decision to taper its asset purchasing programme. Investors withdrew $2.2bn from global emerging market debt funds over the past week according to figures from EPFR Global, the data provider, the highest weekly outflows for 25 weeks."

December 26 - Bloomberg (Kyungji Cho and Yewon Kang): "Offerings of won-denominated company bonds in South Korea plunged the most on record as corporate failures from Tongyang Group to STX Corp. dimmed investor appetite for lower-rated debt. Total sales slid 42% in 2013, the biggest drop in Bloomberg-compiled data going back to 1999. Companies rated A or below led the slump, issuing 7.01 trillion won ($6.6 billion) compared with 12.87 trillion won in 2012. Investors are demanding the biggest yield premiums over government securities in almost two years after the collapse of shipbuilder STX and units of Chaebol Tongyang Group rattled markets."

Turkey Watch:

December 27 - Bloomberg (Selcan Hacaoglu and Onur Ant): "Turkish Prime Minister Recep Tayyip Erdogan lashed out at a widening graft probe that's ensnared his ministers, saying it was an attempt to derail the government and will only benefit financial speculators. 'The operations that started under the guise of corruption are an obstacle to building a new Turkey,' Erdogan said in a televised speech... Erdogan spoke after a top judicial body blocked his order requiring the government to be notified of probes, deepening a standoff that has sent markets tumbling. That ruling was unconstitutional, Erdogan said... 'They are attacking for the last time,' Erdogan said... 'God willing, and with the support of our nation, we will destroy this resistance and repel these attacks."

December 27 - Bloomberg (Taylan Bilgic): "The lira plummeted to a record and Turkish stocks slumped the most in the world as a showdown between the government and judicial powers triggered uncertainty over the country's political stability. The currency weakened as much as 2.3%... against the dollar... The Borsa Istanbul 100 Index dropped 4%... to the lowest level since July 2012. Turkey's two-year bond yield climbed for a second day, rising above 10%."

December 27 - Bloomberg (Selcuk Gokoluk and Ksenia Galouchko): "Foreigners are dumping Turkish bonds at the fastest pace in two years, deepening a selloff that's putting a blot on Prime Minister Recep Tayyip Erdogan's image as the architect of the country's economic turnaround. International investors pared their holdings of Turkish debt by $532 million to a three-month low of $53.8 billion in the week through Dec. 20 after selling a net $1.38 billion the week before... They've cut their holdings from a record $72 billion in May. The outflows are a reversal of the investment that helped finance Turkey's growth during Erdogan's 10-year stint, a period in which nominal gross domestic product more than tripled..."

December 27 - Associated Press (Suzan Fraser): "Turkish riot police blasted opposition protesters with water cannons, tear gas and plastic bullets in Istanbul on Friday in scenes reminiscent of the summer's mass anti-government demonstrations. Some of the protesters threw rocks and firecrackers at police, shouting, 'Catch the thief!' in reference to a widening corruption scandal gripping Prime Minister Recep Tayyip Erdodan's government... Thousands of Erdodan backers, meanwhile, gathered at other spots showing their support for the embattled Erdogan."

December 24 - Bloomberg (Selcuk Gokoluk): "It took Turkish politicians five days to undo what central bank Governor Erdem Basci spent almost $15 billion trying to achieve: lira stability. Trader expectations for future price swings in the currency posted the biggest weekly jump since August in the period ended Dec. 20. Implied volatility in the lira was 11.6% yesterday, the highest after South Africa's rand among peers in emerging Europe and Africa. The Turkish currency slumped to a record 2.0992 against the dollar today as a graft probe implicating four ministers and the chief executive officer of Turkiye Halk Bankasi AS shook investor confidence... 'Raising the fight against lira depreciation via foreign- exchange intervention is more likely to be a red flag to speculators than calm,' Christian Lawrence, a currency strategist at Rabobank International in London, wrote... 'The central bank doesn't have enough reserves to really fight the market.'

China Bubble Watch:

December 23 - MarketNew International: "The stock of local government debt outstanding may have doubled to nearly CNY20 trillion in the two years through end-2012, a senior advisor said... Li Yang, Vice-Director of the Chinese Academy of Social Sciences, cited research showing debt outstanding rose to CNY19.94 trillion from an end-2010 estimate by the National Audit Office of CNY10.7 trillion. Market participants have been waiting for the results of a sweeping audit of local government finances that the National Audit Office began in August... Beijing concluded at the recent Central Economic Work Conference that local government debt is an important task for 2014 policy-making... Fitch cut its China rating in April, the same month that Moody's lowered its outlook on Chinese sovereign debt, with both agencies warning about the risks stemming from local government borrowings. Total private and public sector debt was CNY111.6 trillion at the end of 2012, equivalent to 215% of GDP..."

December 24 - Bloomberg: "China's second cash crunch this year is revealing some of the risks behind pledges by the nation's leaders to elevate the role of markets, in a country where policy makers are unaccustomed to detailing their intentions. The central bank, which unlike counterparts in the U.S., Europe and Japan doesn't schedule decisions on its main policy tool, saw the seven-day interbank repurchase rate rise for a seventh straight session yesterday even after it released more than $49 billion to selected lenders. The People's Bank of China is 'confused' on whether to target the volume of liquidity or influence the price of credit, Bank of America Corp. says... While the PBOC has offered more public statements this time than in June, when it stayed silent for four days while rates jumped to a record high, lack of clarity remains on the pace of credit growth the central bank would be comfortable with."

December 27 - Bloomberg (Selcan Hacaoglu and Onur Ant): "The worst cash crunch since June is forcing Chinese companies to sell bonds at the highest yield since the 1997 Asian financial crisis, crimping their profits and increasing default risks. Evergreen Holdings Group Co., an AA- rated shipbuilder with 16.5 billion yuan ($2.7bn) of debt, sold one-year notes at 9.9% on Dec. 6, the highest among publicly issued onshore bonds since 1997... Fujian San'An Group Co., graded AA, issued similar-maturity securities at 9.4% on Dec. 10. Total note offerings more than halved from a year ago to 163.1 billion yuan in December."

December 27 - Bloomberg (Selcan Hacaoglu and Onur Ant): "China's top government auditor pledged... to watch levels of debt and spending closely to ensure the country's fiscal stability. 'We will look at fiscal sustainability, especially local government risk prevention and control,' Liu Jiayi, head of the National Audit Office, said... The office will also audit all officials in 'key regions, departments, agencies' at least once during their terms and conduct checks of government spending on conferences, meetings and office buildings, he said. China's national auditor has spearheaded central government efforts to increase scrutiny of local officials."

December 26 - Bloomberg (Kyungji Cho and Yewon Kang): "China estimates that growth slowed to 7.6% this year, with mounting challenges putting pressure on the nation's traditional growth model of investment-led spending... A 7.6% pace would mark a third straight annual drop in the expansion rate. 'We cannot deny a downward pressure on economic growth,' Xu Shaoshi, minister in charge of the National Development and Reform Commission, told legislators..."

December 23 - Bloomberg: "Chinese authorities are stepping up a crackdown on corruption, including confiscating the passports of some local leaders, in moves that underscore President Xi Jinping's determination to root out graft. Vice Minister of Public Security Li Dongsheng became the second member of the Communist Party's central committee to be probed this year for suspected corruption. The capital of southern Guangdong province told 2,014 village chiefs to hand in their passports to prevent corrupt local officials from fleeing abroad, the Guangzhou Daily reported."

December 24 - Bloomberg: "China aims to basically complete building over 4.8m social homes and start construction of at least 6m social homes in 2014, the official Xinhua News Agency reports..."

Japan Bubble Watch:

December 27 - Bloomberg (Andy Sharp and Sharon Chen): "Hurdles for Japan's economy next year may increase after Prime Minister Shinzo Abe's visit to a shrine honoring war criminals and others risked deepening tensions with his nation's largest trading partner. The economy, already facing the first bump in the sales tax in 17 years and contending with an erosion in household purchasing power as consumer prices rise, now confronts the potential for damage to exports."

December 23 - Financial Times (Jonathan Soble): "Japan's government has agreed a record initial budget for the coming fiscal year, under which it will increase spending on defence, public works and social security even as it aims to cut borrowing, thanks to an expected jump in tax revenues. Shinzo Abe, the prime minister, and leaders of his ruling coalition gave the go-ahead on Saturday for Y95.88tn ($921bn) in spending for the year beginning in April 2014, an increase of 3.5% over this year's initial budget."

December 27 - Bloomberg (Chikako Mogi and Masaaki Iwamoto): "Japan's inflation accelerated to the fastest pace since 2008 last month, bringing the rate closer to policy makers' target while threatening to erode household spending power unless employers boost wages. Prices excluding fresh food rose 1.2% from a year earlier... A separate report showed industrial output rose 0.1% from October, less than forecast, in a risk for projections of an acceleration in economic growth this quarter. Today's data raise the stakes for employers girding for annual wage negotiations..."

December 24 - Bloomberg (Kevin Buckland and Shigeki Nozawa): "Japan's government plans to decrease annual bond sales for the first time in six years, while boosting issuance of inflation-indexed notes to meet demand from pension funds... Investors such as banks and life insurers will be offered 155.1 trillion yen ($1.49 trillion) in the 12 months starting April 1, down from a record 156.6 trillion yen in the initial plan for the current fiscal year... Sales of linkers will increase by at least 1 trillion yen to a total of 1.6 trillion yen in the period, it said."

India Watch:

December 24 - Bloomberg (Kartikay Mehrotra): "For India's main opposition party, the mood in the world's second-most populous country is similar to that in 1979 Britain, when Margaret Thatcher came to power on a message of strong leadership and effective governance. 'Mrs. Thatcher won on the slogan of 'Labour can't govern - elect a government that rules,' Arun Jaitley, a leading member of the Bharatiya Janata Party, said... 'That's the sentiment that exists in India. The whole country is disillusioned.'"

Europe Watch:

December 27 - Bloomberg (Paul Gordon): "Bundesbank President Jens Weidmann says in interview with Bild that 'in any case subdued price pressure shouldn't be a license for arbitrary monetary-policy easing.'"