For the Nasdaq-100 Index, the Bull market turned five years old in November. Wall Street hopes the hard-charging Nasdaq Bull - that has more than tripled investors' money since Nov 2008 is still in good enough shape to keep the gains coming in Year Six. Many Main Street investors are still wary of the "Least Loved" Bull market, - and they've missed out on the money minting rally. Since the turnaround began on March 9th, 2009, the S&P-500 index has chalked up gains of +175%, - ranking it as the fourth longest bull market of all-time. In cash terms, the US-stock market has generated $13.5-trillion in paper wealth.

In the past year alone, the market value of US-listed stocks increased by more than $4-trillion. On the flip side of the coin, the average bond fund suffered a loss of -5.7% last year, wiping out $2.4-trillion of wealth for US-bond holders. The sharp divergence between booming stock markets and slumping bond markets, - has been dubbed the "Great Rotation." It's been ongoing for the past 1-½ years. Only until the second half of 2013 did the small retail investor decide to jump abroad the "Great Rotation," by yanking $193-billion out from bond mutual funds and plowing $175-billion into stock funds.

For market contrarians, the fact that Main Street investors are finally warming up to the high flying stock market in the fifth year of the Bull Run, is a warning sign to be on the lookout for a market top. On the flip side, Wall Street salesmen say the torrent of retail monies flowing into stocks is a Bullish signal, as it shows there is lots of fresh cash that's still sitting on the sidelines, mostly parked in money market funds, that can fuel further market gains. Yet even the Perma-Bulls on Wall Street admit that a long awaited correction of -10% or more is looming sometime in 2014, albeit, beginning from higher levels. Therefore, a possible climactic rally for the S&P-500 index to the 2,000-level, for example, would fizzle out and begin a descent to today's starting point, thus wiping the speculative froth out of the marketplace.

Stock market Bulls say the "Least Loved" rally is the real thing, and it has the potential to extend into a decade long Mega or "secular bull" market. They point out that the biggest buyers of stocks are the S&P-500 companies themselves. They're generating around $1-trillion in profits each year, and hold about $2-trillion in cash. From late 2009 through all of 2013, the S&P-500 companies spent $1.5-trillion of their surplus cash, buying back their own company shares on the open market. Of course, companies sell stock too, but the net reduction from share buy-ins minus new offerings was an extraordinary $1-trillion in four years . Last year, stock acquired under buyback programs equaled 6.4% of the daily trading volume in the Russell-3000 Index through Sept 30th, exceeding 2007's level of 4.1-percent.

The stock market Bears were blind sighted by the buyback binge. It's estimated that financial engineering was responsible for about 60% of the increase in Earnings per Share (EPS) for the S&P-500 companies, while cost costing, automation, and organic growth padded the rest. The Bears also underestimated the inflationary effects on equity prices that were engineered by the Federal Reserve and the Bank of Japan (BoJ). With their double barreled QE-schemes, the Fed injected $1-trillion into the US-money markets, and the BoJ pumped ¥56-trillion ($500-billion) into the Tokyo money market in 2013, and in turn, fueled powerful rallies in the European, Japanese, and US-stock markets.

Last year, the market value of the Nasdaq-100 index exhibited a +87% degree of correlation with the expansion in the MZM money supply. In the four years leading up to 2009, the correlation was just +36%. So while US-share markets were soaring to record highs, it became clear that the liquidity created by the central banks wasn't flowing to where it is most needed, like business investment. Instead it followed the path of least resistance, ending up in the hands of speculators to bid up equity values.

And the higher the stock prices climb, the more enthusiastic Corporate CEO's and directors become for buying back the company's shares and so on, thus inflating the share price upon which their stock option plans are based. A lot of what's called investment these days is just a transfer of cash to shareholders at ever-inflating prices. The Fed's QE scheme did strengthen the demand for Tiffany bags and Ferraris and fine wines and equities, but the "trickle down" effect to the struggling masses was too small to boost the stagnant wages of the working class. Instead, the Fed's QE-scheme has simply widened the schism of wealth inequality in America. This is so, since 10% of the US-households own 82% of the listed shares.

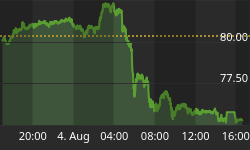

During the course of 2013, there was a brief interruption in the Nasdaq'-100's parabolic ascent. There was a pullback of -7.3% in the May-June timeframe, when Fed chief Ben Bernanke shocked the markets, saying the central bank would soon begin to reduce the size of its money injections. Bernanke tried the calm shareholders, saying "Tapering" of QE is not the same as "Tightening." He pledged to keep the federal funds rate locked at 0.25% for as far as the eye could see. As such, the Nasdaq-100 index quickly regained its footing and zoomed +27% higher in the second half of 2013.

On Dec 18th, the Fed said it would begin tapering its QE injections, starting with a modest reduction of $10-billion per month in January to $75-billion. Again, despite the Fed's alert, the stock Bulls were unfazed, and continued bid-up the share prices of high flyers such as Amazon, Google, Price-Line, MasterCard, Visa, and Boston Beer.

In Tokyo, Bank of Japan (BoJ) chief Haruhiko Kuroda put a positive spin on the Fed's decision to begin winding down its radical QE-3 scheme, saying it's a sign the US-economy is steadily recovering, and that it can continue to grow without the need of extraordinary stimulus, - which bodes well for global growth and Japan. While Kuroda spoke, the US-dollar hit a fresh five-year high of ¥ 104.60 . " Frankly speaking, the correction of excessive yen strength has had a positive effect on Japan's economy. Corporate earnings have risen and sentiment has improved," Kuroda said , as the Nikkei-225 index crossed the 16,000 line.

Soon after taking office in Dec '12, Japan's Prime Minister Shinzo Abe promised to end the 15-year bout with deflation and pull the world's third largest economy out of a recession. Firing the first arrow of "Abenomics" - the BoJ began to unleash a sharp devaluation of the Japanese yen against the currencies of its major trading partners. On April 4th, 2013, the BoJ vowed to double the amount of Japanese yen in circulation to ¥270-trillion, within a time span of just 2-years. "The BoJ's policy steps could indirectly result in a weaker yen and boost share prices, helping to lift corporate earnings," Abe declared .

Tokyo got the green light from its Group-of-20 peers at a Feb '13 meeting in Moscow for its aggressive plans to weaken the yen. With liquidity injections of ¥7-trillion per month, Tokyo has engineered the yen's -18% devaluation against the US$, -23% against the Euro, -15% against the Korean won, and a -12% slide against the Chinese yuan. For Nissan Motor, which gets 80% of its revenue outside of its home market, whenever the US-dollar's value rises by 1-yen, it boosts its operating income by ¥ 15-billion ($151-million). Sony and Honda Motor get more than 65% of sales outside Japan, and also profit from a weaker yen. As a result, profit for Japanese companies listed on the broader Topix index increased to ¥ 74.70 /share last year, up from ¥ 50.29 in 2012, and ¥ 38.05 in 2011. The $4.3-trillion Topix index posted a +49% advance last year, - its best annual gain since 1999.

Yen Carry Trade lifts Dow Industrials to all-time highs, The BoJ's extraordinary effort is making big waves, driving down the value of the yen and lifting Japanese share prices in Tokyo. The BoJ has taken a page out of the Fed's QE playbook, - but multiplied by 3-times . The BoJ is buying ¥7.5-trillion of government bonds (JGB's) per month, and intervening directly in the equity market, by purchasing ¥1 trillion of exchange-traded funds linked to the Nikkei-225 each year. The BoJ aims to inject $1.4-trillion into the Tokyo money markets by April '15, equal to a third of the size of Japan's $5-trillion economy.

And the effects are also being felt overseas. The BoJ's radical policy enables traders to borrow yen at virtually zero percent interest rates in order to invest in US- blue chip stocks or higher yielding junk bonds. In effect, it's better than money for nothing; a speculator gets paid to borrow in ever-depreciating yen. Since it became apparent that Shinzo Abe would pursue a policy to devalue the yen, - carry traders have reaped a double windfall in both US-listed stocks and the foreign exchange market. The general movements of the Dow Jones Industrials have closely tracked the US$'s gyrations versus the yen. As such, US-equity traders are keeping a close eye on every wiggle in the US$ /yen exchange rate.

Not only is the yen losing ground because of the prospect of higher US-bond yields, as a result of the Fed winding down its QE-scheme, but the yen is also weakening because it was regarded a safe-haven currency, but now it's sold because traders are buying risk again. The problem with carry trades though is that they tend to get overcrowded with the bankers and hedge funds that play them. History shows that these trades tend to move in one direction as everybody jumps aboard the bandwagon. Carry traders bet on an infinite continuation of a trend (down) in the yen and low volatility. As long as it is working, no worries.

However, the yen carry trade becomes extremely dangerous if everyone is taking a lot of leveraged risk in an equity rally that starts to fizzle out. And it will all be OK until, one day, it isn't. Once something happens to interrupt that pattern, the mayhem begins. Forget the VIX. The new fear gauge for markets is the Japanese yen. A strengthening of the exchange rate of the yen -- is a warning flag for global stock markets.

Euro hits 5-year high vs Yen - The Euro's extended climb against the Japanese yen has also been a key driver fueling the German DAX-30's advance to record heights in Frankfurt. 1-½ years since European Central Bank (ECB) chief Mario Draghi pledged to do "whatever it takes to save the Euro," - it's been a big game changer. Draghi's proposal to buy unlimited amounts of sovereign debt that would be sterilized, took the systemic risk out of the notion of a break-up of the Euro currency. " And believe me, it will be enough," he warned on a warm summer day in London. Since then, the Euro has climbed ¥50 higher to around ¥145 today.

Alongside the Euro's +50% advance against the yen, - the German DAX-30 index catapulted an identical +50% higher (thanks to carry traders) to above the 9,500-level - it's highest in history, and +15% above its 2007 high. The powerful DAX rally caught many analysts by surprise. After-all, exports are the mainstay of the blue-chip DAX companies that earn 75% of their revenue from outside the country. Yet during the first 10-months of 2013, German exports totaled €917-billion, a drop of -0.7% compared with a year earlier. The best that can be expected for 2013 as a whole, according to the Federation of German Wholesale, Foreign Trade and Services (BGA), is an increase of +1-percent. Still, despite flat export sales, Euro /yen carry traders still bid-up the DAX-30 index to the stratosphere.

Korea objects to "Abenomics" - As the Fed begins to print less currency than the BoJ - (sometime in Q'1 of 2014), - more hedge funds could jump upon the "yen carry" trade bandwagon, and knock the yen even lower. So far, European exporters are not publicly crying foul at the BoJ's QE-scheme, that has sent the Euro to a five-year high against the yen. However, Korea's oligarchs are feeling the pain from the fallout. On Jan 3rd, Seoul says it's ready to take action to counter the yen's slide versus the Korean won.

Since the summer of 2011, the Japanese yen has lost a third of its value compared to the Korean won, falling to as low as 10.15-won last week, - it's lowest level in five years, prompting Korea's Finance chief Hyun Oh-seok to warn, "We are closely monitoring market volatility ." The yen's slide to nearly 10-won sent the share prices of major Korean exporters such as Samsung Electronics and Hyundai Motor tumbling -10% lower on concerns their competitiveness in world markets would suffer. Together, these two companies equal 21% of the entire market value of Korea's Kospi index. Unlike, the booming Japanese stock market, the Korean Kospi index ended unchanged in 2013. The Kospi kingpins were weighed down by the slumping yen /won exchange rate, which is especially important as Korean and Japanese exporters compete head to head in items from smart-phones, to TV's, to ships and autos.

Indeed, a few days after Korea's MoF issued its threats to stop the yen's slide versus the won, on Jan 6th, Samsung Electronics (005930) posted its first profit decline in nine quarters - citing stiffer competition from Apple's (AAPL) newest iPhones and much cheaper smart-phones made by Chinese companies. As such, Samsung's operating profit fell -18% to 8.3-trillion won ($7.8-billion) in Q'4. Between Dec 24th and Jan 3rd, Samsung's stock price dropped -10%, and erasing about $19-billion of its market value. "We will strengthen our monitoring for offshore flows and when needed carry out stabilizing measures for financial and foreign exchange markets," Bank of Korea Governor Kim Choong-soo warned on Jan 3rd. While the Bank of Korea (BoK) regularly intervenes in the foreign-exchange market to help smooth volatility - it bought $2-billion in October - the warnings have only won a brief reprieve.

"Yen Carry" Trade to the Rescue in 2014, - Even if the Fed actually unwinds QE by its final meeting in Dec 2014, it could still end-up injecting an extra half-trillion dollars of liquidity into the US-banking system in the year ahead, before its task is complete. At the same time, the BoJ would pump around $850-billion worth of yen into the global money markets through the course of the year. The combined effort, - $1.35-trillion of additional liquidity would be used as a backstop to help prop-up the shares listed in Frankfurt, New York, London, and Tokyo, with a combined market value of $34-trillion, (out of a total of $63.5-trillion worldwide).

If the Fed does wind down QE, the "yen carry" trade could act as a stabilizer. As the Fed tapers QE, the yield spread between the US's 5-year T-note and Japan's 5-year note could widen further to +200-bps or higher, up from around +150-bps today. In turn, the US$'s exchange rate could also climb higher towards ¥110 to ¥115. Since the Japanese and US-stock markets are tracking the US$'s exchange rate against the yen, central bankers are hopeful the yen carry trade can energize the Bull market awhile longer.

"The stock market has become addicted to the Fed's easy-money polices," said Republican Senator Charles Grassley of Iowa. "The benefits to Main Street have been questionable at best. No one can deny that the risks are real and could be devastating if QE continues for too long," Grassley warned. Yellen's critics say the Fed has inflated stock and real estate bubbles that could burst and deeply wound the economy again. The S&P-500 index was up +30% last year, while earnings were up +5% and revenues were flat. At the same time, the level of margin debt to buy equities is at an all-time high, underscoring that the stock market is more about financial engineering and speculation - built on the quicksand of leverage.

Looking forward, the biggest headwind for the markets is the probability of a further half-percent increase in US and global bond yields in the months ahead, as the Fed scales down its intervention. A further +1% increase in US-bond yields could puncture the US-housing recovery, - a key engine of growth for the US-economy. As the Fed gradually unwinds QE, the artificial distortions in the marketplace would start to fade and the price discovery process would become based upon the collective judgments of millions of investors, and not upon the decision of a few central planners, - manipulating the markets behind closed doors.

There is a risk that the unwinding of the Fed's QE-3 scheme could re-incarnate the bursting of the dot-com bubble of the 2000's. As an added insurance policy, central bankers are hopeful the liquidity flowing from the "yen carry" trade could offset the negative impact on the Japanese and US-stock markets. "There's a lot of uncertainty about how a monetary policy exit will occur with a very large balance sheet," said New York Fed chief William Dudley on January 4th. "There's no question that there could be unintended consequences."

This article is just the Tip of the Iceberg of what's available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and future predictions about the (1) top stock markets around the world, (2) Commodities such as crude oil, Gold, copper and base metals, (3) Foreign currencies, such as the Australian and Canadian dollars, Brazil real, the Euro and Japanese yen, (4) Central bank interest rates and global bond markets, (5) Central bank Intervention techniques (6) and key Credit Default Swap markets.

GMT filters important news and information into (1) bullet-point, easy to understand reports, (2) featuring "Inter-Market Technical Analysis," with lots of charts displaying the dynamic inter-relationships between foreign currencies, commodities, interest rates, and the stock markets from a dozen key countries around the world, (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, posted Monday and Wednesday evenings, with the latest news and analysis on global markets. To order a subscription to Global Money Trends, click on the hyperlink below,

http://www.sirchartsalot.com/newsletters.php

or call toll free to order, Sunday thru Thursday, 8-am to 9-pm EST, and on Friday 8-am to 5-pm, at 888-808-7978. Outside the US call 561-391-8008.