Participants who buy gold futures in London [known to be a physical market] are more inclined to want physical metal. Participants who buy [or sell] at COMEX, in the New York "paper market" are more likely to be speculating on the price movement in the underlying product or commodity - not wanting to get involved with moving, insuring and warehousing physical metal. While the two markets trade at identical prices while they are both open for business [between 8:20 am ET and 11:00 am ET], the difference is material and much more than nuance.

Until one appreciates the difference between the physical [London] and paper markets [COMEX, New York] for gold, it is difficult or impossible to comprehend the importance or significance of gold market price action. This is never explained by mainstream financial news outlets like CNBC when they say, as a typical for instance, "The price of gold fell 12 dollars today". Even if not intended, in many cases statements like this are VERY misleading - even if the price of gold was in fact 'down' 12 bucks in a given day. In many cases, what might be a more accurate description is: 11 dollars worth of a 12 dollar price drop occurred between 11:00 a.m. EST [when London closed] and 1:30 p.m. [when N.Y. COMEX closes]. Understanding this difference and interplay is material to understanding the case of gold bugs like the folks at GATA - that the gold market is manipulated.

This is relevant because shorting a commodity implies selling something you do not own, with the hopes of buying it back cheaper at a later date. This necessarily involves borrowing the goods sold, to make delivery by the settlement date, unless a corresponding purchase has been made to offset the short. What this figuratively means is: if you short gold in London, there is a better chance you will be called on to deliver the physical product. If you short gold at the N.Y. COMEX you statistically stand a far greater chance of settling your trade with an offsetting purchase for your 'paper-short' commitment - hence less worry of the need to deliver the underlying metal. So, it would be accurate to say: if anyone was going to unscrupulously attempt to suppress the price of gold, they would want to do so by selling on the N.Y. COMEX, not in London.

The vast majority of the most savage sell offs in the price of gold take place immediately after 11:00 a.m. ET when the London market closes for the day - lessening the seller's likelihood of being required to deliver physical metal. This happens with such regularity and precise timing; its occurrence cannot be other than planned and coordinated. So the logical question then becomes - why and by whom?

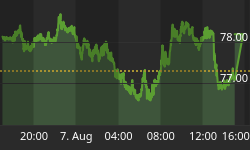

The type of market action referred to above blatantly appeared again today, Friday June 24, 2005 as illustrated here:

I would like everyone to take special note of the pronounced plunge of the "spot" gold price at immediately after 11:00 am. E.T. Notice how the gold price was 'instantaneously managed' down, seemingly for a '3 dollar elevator ride' to a level just under 439 per ounce - which coincidentally just happened to be a purported crucial 'chart point' - a close above which would be technically positive for the price of gold? To the uninitiated, I would like to point out that stark, precipitous price movements in other financial instruments like the 'elevator ride' depicted above are typically associated with 'other than expected economic releases', or 'reporting surprises', on the part of officialdom. This type of movement in the gold price has become all too familiar with gold bugs - typically, for no other reason than it being the very moment when the London Bullion Market packs their bags to go home for the night. I would suggest, to anyone who wants to listen, that these are merely the entrails of acts of desperate and dangerous people attempting to manipulate the gold market's technicals and sentiment. The prospect that oft repeated price movements such as this -virtually always skewed to the downside - are the result of free or random markets is completely and utterly beyond incredulity.

When markets are managed or rigged, the miscreant typically [even in the face of denial] leaves an unavoidable and identifiable footprint [like hitting bids in a rising market or offering limitless amounts at a static price in a rising market] - somewhat like a fingerprint or the DNA of a perpetrator. One man whose work has brought to light this phenomena in the gold market is GATA consultant, Mike Bolser. Bolser employs statistical regression analysis to perform what amounts to forensic statistical accounts of how there appears to be an 'invisible participant' involved in the trade whose actions dictate they are not motivated by "profit maximization".

This is graphically [and scientifically] explained in the following graph:

Table 1: Compliments G. M. Bolser http://www.interventionalanalysis.com

According to Mike Bolser himself,

"Recall that preemptive selling, which is a fraud detection algorithm, measures very aggressive COMEX gold market selling when compared to the London gold market (LBMA). Table 1 displays the percentage of days per month in which the COMEX gold price falls 300% more than the London gold price. The probability of changing macroeconomics being the cause for such extreme New York price drops is highly diminished because the two markets trade the same commodity on the same day. Preemptive selling should not be confused with price volatility or rate of change, which are measures of rapid price fluctuation. In addition, preemptive selling is a measure of relative activity between two markets. Recall also that it does not measure the volume of comparative selling, only its effect as measured by gold market prices."

Bolser describes the relevance of the std. dev. spikes as follows, "The numbered spikes are correlations to other gold-related events as follows: (1) Federal Reserve assumes two board seats at Bank for International Settlements; (2) steadily rising gold price threatens to pierce $400; (3) important change downward in the long-term gold price; (4) failure of Long-Term Capital Management, reportedly involved in the gold carry trade; (5) Washington Agreement provokes sharp rise in gold prices; and (6) Canadian Imperial Bank of Commerce works to resolve Ashanti hedge book failure."

The long and short of it, folks, the work and analysis depicted above amounts to a lie detector. The odds of the events depicted above happening in "free" markets are something in the magnitude of perhaps once every 2,000+ years or worse. Officials at the U.S. Treasury and Fed expose themselves as market riggers when they fail this test miserably - one might call this incriminating if they were of that mind.

The spot gold market in particular trades in peculiarly repetitive fashion, in that most if not all bullish [for gold] economic news releases would produce rallies that make their highs in the first 30 minutes of COMEX trading. After the gold price makes this immediate high it never fails to meet fierce resistance at 6 bucks up, effectively capping any rally for the rest of the day regardless of volume [demand]. Bearish news, on the other hand, can and typically does cause gold to plummet 15 or more dollars on any given day, with successively lower lows throughout the session - even on lighter volumes. Statistically speaking, free markets do not trade this way, ie. Price action always markedly skewed to the downside. The actions outlined above are categorically not representative of players trying to maximize profits.

Economics 101 tells us that players in free markets always try to maximize their returns. This is one of the cornerstones, and if you will - "givens" - of Capitalism. As GATA Chairman - Bill Murphy has so aptly and often pointed out, time and time again in his Daily Midas columns at www.Lemetropolecafe.com - the gold price fixers virtually always swing into selling action, invoking "the six dollar rule" when the price of gold climbs by 6 dollars in one day. These observable price capping maneuvers along with the statistical analysis of Mike Bolser show that, indeed, the gold market is 'rigged'. This assertion is factually based in the tenets of mathematics and the fundamentals of Capitalism folks, not emotion or here say.

We should all care about this chicanery because it makes a mockery of claims that our financial markets are free and fair. That we have a media, that claims to be "the freest in the world" - that refuses to report on these facts is beyond scandalous and more than shameful. The scale of duplicity outlined here makes the shenanigans committed at Enron, World Com, Adelphia and budding problems at AIG look like child's play. It's at the root of why interest rates are so mysteriously low [it's really not a conundrum, you know?], the problems with major pension plans defaulting, spiraling commodity and asset prices as well as a structurally over inflated U.S. dollar. More so, it goes a long way to explaining why a dollar today only buys about 10 cents worth of goods in 1970 dollars. Pointing this out does not mean that one chases flying saucers, is anti-business or they are not patriots as folks like Larry Kudlow would have us believe - but that's a story for another day, ehh?

We should all care about this chicanery because it makes a mockery of claims that our financial markets are free and fair. That we have a media, that claims to be "the freest in the world" - that refuses to report on these facts is beyond scandalous and more than shameful. The scale of duplicity outlined here makes the shenanigans committed at Enron, World Com, Adelphia and budding problems at AIG look like child's play. It's at the root of why interest rates are so mysteriously low [it's really not a conundrum, you know?], the problems with major pension plans defaulting, spiraling commodity and asset prices as well as a structurally over inflated U.S. dollar. More so, it goes a long way to explaining why a dollar today only buys about 10 cents worth of goods in 1970 dollars. Pointing this out does not mean that one chases flying saucers, is anti-business or they are not patriots as folks like Larry Kudlow would have us believe - but that's a story for another day, ehh?