If it seems that the frequency of my posts has diminished of late, it is no illusion. There are many reasons for that, many business-related, but there is at least one which is market-related: a three-month-long, 20bp range in real and nominal yields and a year-to-date S&P return that seems locked between +2% and -2% with the exception of the January dip offers precious little to remark upon. Along with those listless markets, we have had plenty of economic data that it was very evident the market preferred to ignore and blame on "severe weather." And, to the Fed's lasting credit (no pun intended), the decision to start the taper under Bernanke and thus give Yellen a few months of simply sitting in the captain's chair with the plane on autopilot has short-circuited the usual rude welcome the markets offer to new Fed Chairmen.

These sedate markets irritate momentum traders (you can't trade what doesn't exist) and bore value traders - at least, when the markets are sedate at levels that offer no value. For individual investors, this is a boon if they are able to take advantage of the quiet to pull their attention away from CNBC and back to their real lives and jobs, but for professional investment managers it is frustrating since it is hard to add value when markets are becalmed.[1] Yes, successful investing - which is presumably what successful investment managers should be practicing - is very much about patience, and this is doubly or trebly true for value managers who eschew investing heavily into overvalued markets. I am sympathetic with the frustrations of great investors like Jeremy Grantham at GMO, but I will point out that his frustrations are more acute among less-legendary managers. It is, after all, much easier to pursue the patient style of a Hussman or Grantham...if you are Hussman or Grantham.

Again, I'm not whining too much about our own difficulty in securing good performance, because we've done well to be overweight commodities and with some of our other position preferences. I'm more whining about the difficulty of writing about these markets!

But let's reset the picture, now.

The very weak Q1 GDP figure from last Wednesday (a mere +0.1%, albeit with strong consumption) is old news, to be sure, and investors are right to underweight this information since we already knew Q1 growth was weak. But at the same time, I would admonish investors who wish to patiently take the long view not to get too ebullient about Friday's jobs figure. Payrolls of +288k, with solid upward revisions, sounds great, but it only keeps us on the 200k/month growth path that we have had since the recovery reached full throttle back in late 2011 (see chart, source Bloomberg).

As I wrote back in August, 200k is what you can expect once the expansion is proceeding at a normal pace, and that's exactly what you've gotten for a couple of years now. Similarly, if you project a simple trend on the Unemployment Rate from late 2011 (see chart, source Bloomberg) you can see that the remarkable plunge in the 'Rate merely operated as a 'catch-up' from the winter bounce higher.

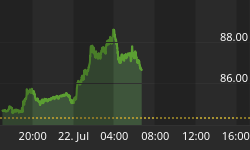

If you believe that inflation is caused when economies run out of slack (I don't), then the low unemployment rate should concern you - not because it fell rapidly, because it is nearer to whatever threshold matters for inflation. If you rather think that inflation is caused by too much money chasing too few goods, then you've already been alarmed by the continued healthy rise in M2 and the fact that median inflation rose to 2.1% this month. So, either way, people (and policymakers) ought to be getting at least more concerned about inflation, no matter what their theoretical predilections. And, in fact, we see some evidence of that. Implied core inflation for the next 12 months (taking 1-year inflation swaps and hedging energy) has risen in the past month to about 2.25% from 1.75%. To some extent, this seems to be seasonal, as that measure has risen and peaked in the last three March/April periods. Investors tend to mistake the rise in gasoline prices that normally happens in the spring to be inflation, even though it ordinarily falls back later in the year. But right now, the implied acceleration in core inflation from the current level of 1.7% is the highest it's been in three years (see chart, source Enduring Investments).

The bigger spike, on the left side of that chart, corresponds with the significant fears around the time of QE2. But what's interesting now, of course, is that the Fed is actually tightening (providing less liquidity is the definition of tightening) rather than easing. Some of this is probably attributable to base effects, as last year's one-off price decline in medical care services due to sequestration-induced Medicare spending cuts is about to begin passing out of the data. But some of it, I suspect, reflects a true ... if modest ... rising concern about the near-term inflation trajectory.

[1] Unless, that is, you are overweight commodities...which we are. The DJ-UBS is +8.9% year-to-date.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"