Despite The List Of Concerns, Stocks Fail To Correct...Again

On May 14, we noted that by continually evaluating both the bullish and bearish case for the market, investments and economy, we can reduce personal bias and increase investment flexibility, a key element of success. A week ago, it would have been easy to build the back-of-the-napkin bearish case for stocks:

- The Fed has been a big part of the recent rise in asset prices; now they are in tapering mode.

- Geopolitical risks have been rising, providing a source of uncertainty. Markets do not like uncertainty.

- Europe can't seem to shake the low inflation bug, which allows the term deflation to remain in the picture. Deflation and bull markets make strange bedfellows.

- China is trying to shift from a credit-dependent, export-only economy to one that can lean more heavily on organic growth. The transition can lead to disappointing economic data.

- The U.S. economy is showing signs of vulnerability with housing leading the way.

If we had entered the week with a bearish bias, it would not have been particularly helpful. In the last five trading sessions the S&P 500 tacked on 22 points, and finished the week at a new closing high.

Correction Cases Have Been Easy To Find

The financial press has been littered with bearish pieces in recent weeks. From Forbes:

It looks like we are facing a stock market correction. That's not surprising, there is always a correction around the corner. It would be a new world if the stock market didn't have a tendency to correct and crash...Rule 1 of corrections is to answer the big question. Is this a crash or just a correction? A crash tends to need a big reason for its occurrence. The dotcom crash was a clear bubble. The credit crunch crash was caused by the freeing up of the massive credit markets. It normally needs something massive to make a true crash. If you think we are in such a dynamic, then bail....We all hate the prospect of a slump or a crash, but in fact they are little gifts to long-term investors. While the crazy speculators get toasted, savvy people get to buy stocks at knock down prices. So here is to the coming summer sale. Good luck.

On March 31, Bob Johnson penned a well-written piece on Seeking Alpha that noted the significance of the Fed's impact on equity prices:

There is a growing consensus that we are well overdue for a correction of 10% to 15% or 20%. This is not empty speculation, but is based on historical patterns as well as changes that are going on now in the economy and the market. We know that the economy and the market have been artificially stimulated and that the market has responded in lockstep with the release of money from the Fed. As we all know, that is going to stop. One would be naive to believe that the economy and corporate earnings are strong enough to continue the upward trend in the market.

Our purpose here is not to criticize the writings of others, but rather to point out the market's propensity to buck the consensus forecast. To be fair, we wrote the passage below in an article titled Is A Stealth Bear Market Already In Motion?

We have no problem assigning a "yellow alert" profile to the 2014 stock market. It is not time to run for the equity exits, but it is a good idea to locate the nearest escape hatch.

Despite the sound rationale for a pullback in stocks, the S&P 500 is higher now than it was in April.

Stocks Can't Correct Until This Happens

As noted in this week's stock market video, it is not possible for stocks to experience a multi-week or multi-month correction without a breakdown occurring in the major stock indexes first. The video covers what we will be monitoring in the coming holiday-shortened week.

The Other Side Of The Napkin

Markets are rarely 100% bullish and rarely 100% bearish, meaning there are usually two sides to any equity story. For example, we could have flipped the napkin over on May 17, and easily made the bullish economic case:

- Economic data was impacted by weather in Q1. We can expect some default improvement going forward.

- Investor expectations about future economic growth and corporate earnings remain low, meaning it won't take much improvement to exceed expectations.

- The Fed is not going away anytime soon. Even if stocks begin to weaken, the odds are high the Fed will step in based on this rationale.

- The European Central Bank may step forward as the Fed is stepping back. Economic stimulus is economic stimulus; markets do not care where it comes from.

- Markets can look past geopolitical concerns, especially if they perceive the spillover effects can be contained.

How did the past week play out in the real world? From Barron's:

Economic data continue a two-step-forward, one-step-back dance. Last week initial weekly jobless claims increased slightly but new-home sales improved. Friday, the Commerce Department said new U.S. single-family home sales rose to 433,000, modestly above consensus but better than March. While economic news has been generally supportive of higher share prices, the market remains hesitant and still has a wait-and-see attitude, says Timothy Leach, chief investment officer at U.S. Bank Wealth Management. Investors are apprehensive about the effect on the economy of the Federal Reserve ending its quantitative-easing strategy later this year, he adds. It's as if the market is trying to navigate a river of doubt, using each data point as a stone to hop across, he says. Separately, the venerable Dow Theory remains in a bullish trend for stocks, according to Ned Davis Research. For youngsters, the theory goes that industrials make the goods and transportation firms ship them, so when there's confirmation between the Dow and the Dow Jones Transportation Average, it's a signal about stock trends.

Frustrated With The Forecasting Game?

Why does Wall Street constantly produce forecasts, when we all know their track record is questionable at best? There is demand for them. In a 2014 outlook article, we posed the following question:

Are we better off basing investment decisions on forecasts or a method based on observing, tracking and adjusting?

The full article makes the complete case, but the main concepts are captured in this segment:

The weekly chart below tracks the desire to own stocks (SPY) relative to the desire to short stocks (SH). When the desire to own stocks is greater than the desire to short stocks, it speaks to a state of aggregate economic confidence. As of Monday's close, the ratio has experienced some relatively mild weakness. If the look of the chart morphs into something similar to points C and D below, our concerns about the stock market will increase. For now, the chart is calling for some patience with stocks.

Keep in mind, our analysis above does not involve the use of a Ouija board or palm reading. The changes in the market's risk tolerance are observable. If the bull market slips into a bear market, the ratio above will flip over to a bearish look. The beauty of math, data, and charts is they are free from emotions, opinions, and cloud-inducing bias.

Investment Implications - Better, But Still Some Hurdles

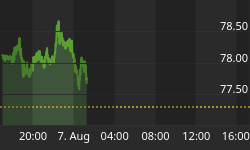

Bear markets are usually associated with economic contractions. While recent economic data has been somewhat soft, it is not hinting at a prolonged period of negative growth. As of Friday's close, the weight of the evidence still sides with the bulls. Our market model uses numerous inputs to assist us with a "monitor and adjust" approach, which is quite a bit different than an "anticipate and hope" strategy. The observable improvement that occurred over the last five sessions enabled the model to recommend a slight increase to the growth side of our portfolios. Therefore, Friday we added to our stock holdings (SPY) and reduced our money market balances. As shown in the chart of the S&P 500 below, this week's gains represented more of a baby step for the bulls, rather than a monumental bullish step. However, the S&P 500's weekly gain of 22 points far exceeded the expectations of many.

The evidence we have in hand still calls for some offsetting exposure to bonds (TLT), meaning we have not pushed all our chips to the center of the equity table. We will enter next week with a flexible and open mind. Fox Business provides an early look at the economic calendar:

Housing data and a report on gross domestic product will highlight next week's economic calendar. U.S. banks and securities markets are closed Monday for the Memorial Day holiday... On Tuesday a second GDP reading is due and economists believe it could be worse than the first... Also due next week are reports on consumer confidence on Tuesday and consumer sentiment on Friday. Both numbers are expected to move slightly higher as an improving U.S. labor market offsets concerns for rising food and energy costs.

Weekend Reading

Since the odds of good things happening for stocks improved a bit this week, the articles below cover still-relevant "what if stocks surprise on the upside" concepts:

- Concerned About Being Underinvested? You Should Be

- The 2 Most Important Questions For Investors

- Managing Risk In A Mature Bull Market

- Are The Markets Heading Back To The 1990s And Hammer Time?

- Respected Model Says Stocks Could Rise 12% By September