It is common knowledge that Japan is in extreme financial difficulties, and that the currency is most likely to sink and sink. After all, Government debt to GDP is over 250%, and the rate of increase of retirees has exceeded the birth rate for some time. A combination of population demographics, escalating welfare costs, high government debt and the government's inability in finding a solution to Japan's ongoing crisis ensures for international speculators that going short of the yen is a no-brainer.

Almost without being noticed, the Japanese yen has already lost about 30% against the US dollar and nearly 40% against the euro over the last two years. The beneficiaries of this trend unsurprisingly are speculators borrowing yen at negligible interest rates to speculate in other markets, expecting to add the yen's depreciation to their profits. Thank you Mr Abe for allowing us to borrow yen at 1.06 euro-cents two years ago to invest in Spanish 10-year government bonds at 7.5%. Today the bonds yield 2.65% and we can buy back yen at 0.72 euro-cents. Gearing up ten times on an original stake of $10,000,000 has made a clear profit of some $300,000,000 in just two years.

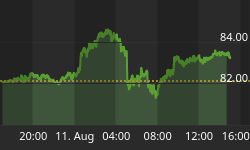

Shorting the yen has not been profitable this year so far, with the US dollar falling against the Japanese yen from 105.3 on December 31st to 101.5 at the half-year, an annualised loss of 7.2%. This gave a negative financing return on all bond carry trades, which in the case of Spanish government debt deal cited above resulted in annualised losses of over 5%, or 50% on a ten times geared position. The trader can either take the view it's time the yen had another fall, or it's time to cut the position.

These returns, though dependent on market timing, are by no means unique. Consequently nearly everyone in the hedge fund and investment banking communities has been playing this lucrative carry game at one time or another.

Not only has a weak yen been instrumental to lowering bond yields around the world, it has also been a vehicle for other purchases. On the sale or short side, another commonly agreed certainty has been the imminent collapse of the credit-driven Chinese economy, which will ensure metal prices continue to fall. In this case, gearing is normally obtained through derivatives.

However, things don't seem to be going according to plan for many investment banks and hedge funds, which might presage a change of strategy. Copper, which started off as a profitable short by falling 12.5% to a low of $2.93 per pound, has recovered sharply this week to $3.26 in a sudden short-squeeze. Zinc is up 6.4% over the last six months, and aluminium up 6%. Gold is up 11%, and silver 8.5%. So anyone shorting a portfolio of metal futures is making significant losses, particularly when the position is highly geared through futures.

It may be just coincidence, but stories about multiple rehypothecations of physical metal in China's warehouses have emanated from sources involved with trading in these metals. These traders have had to take significant losses on the chin on a failed strategy, and may now be moving towards a more bullish stance, because China's warehouse scandal has not played out as they expected.

So two certainties, the collapse of both the yen and of Chinese economic demand don't seem to be happening, or at least not happening quickly enough. The pressure is building for a change of investment strategies which is likely to drive markets in new directions in the coming months.