Things are turning interesting again.

An interesting week saw that Brazilian real get hammered for 4.2%, as Brazil's stocks sank 6.2%. Venezuela Credit default swap (CDS) prices surged 158 bps to 1,464 bps (lagging Argentina at 1,840!). Turkish stocks were hit for 5.3%, in what Bloomberg called the emerging-market stocks' "steepest decline in 15 months." Commodities currencies were also pummeled. The Australian dollar dropped 3.6%, the South African rand 3.0%, the New Zealand dollar 2.1% and the Canadian dollar 1.9%. The Goldman Sachs Commodities Index was hit for 2.4%, trading this week to the lowest level since the tumultuous summer of 2012. Brent crude fell to a two-year low, wheat to a 50-week low and gold to an eight-month low. Spanish yields jumped 30bps, with Italian yields up 20 bps and France's 17 bps. U.S. junk bond CDS jumped 21 bps this week. In the face of unsettled global risk markets, 10-year Treasuries jumped 15 bps this week.

Market and macro analysis remains extraordinarily challenging. The U.S. economy shows momentum and financial conditions remain ultra-loose. Wall Street strategists are universally bullish. A recent survey (Investors Intelligence) had the smallest reading of bears since 1987. Sentiment is buoyed by the view that it will be years before the Fed raises rates to the point where they would weigh on risk asset prices.

It's no surprise that I see the greatest financial Bubble in history. I believe asset market inflation and Bubbles have been fueled by speculative leverage exceeding pre-2008 crisis levels. I see global financial and economic imbalances that have been exacerbated by six years of the most extreme monetary policy measures. By now, this type of analysis has been completely discredited. Few will care that I discern acute vulnerabilities.

There was important confirmation of my analytical thesis back in the spring of 2013. The so-called "taper tantrum" saw the emerging markets (EM) under heavy selling pressure. Global (highly correlated) risk asset prices began to falter. Importantly, in the face of heightened risk aversion, Treasury yields moved higher. This was problematic for many popular leveraged strategies that incorporate "safe haven" Treasuries as a hedge against other risk asset classes (equities, corporate debt, EM and commodities). I still believe overheated global markets were on the brink of a meaningful bout of "risk off" de-risking/de-leveraging. But immediate support from the likes of Bernanke ("The Fed will push back...") and Dudley ensured that fledgling "risk off" was transformed into an only more emboldened "risk on." Market prices are today higher and the latent risks only greater.

Assuming QE would wind down this year, I've been on guard for a reemergence of the "May/June (2013) Dynamic." Back in late-March I titled a CBB "The April, May, June Dynamic?" Spring - and most of summer - came and went. In spite of an alarming deterioration in the global backdrop, a determined "risk on" held sway.

This week, however, saw the emergence of a backdrop increasingly conducive to "risk off." Currency market instability is turning into a critical issue for global risk markets. The dollar index traded this week near the highest level since 2010. Importantly, EM currencies, for the most part having held their own, have now begun to show fragility. So far in September, the Brazilian real is down 4.4%, the Colombian peso 3.8%, the South African rand 3.2%, the Turkish lira 2.7% and South Korean won 2.1%. Arguably, "King dollar" is becoming an increasing risk to economies and financial systems around the world.

Federal Reserve post-2008 crisis reflationary measures were a catalyst for a momentous global "reflation trade." Fed zero rate policy and massive debt monetization both pressured the dollar and flooded the world with liquidity. The EM complex was the greatest beneficiary of this liquidity onslaught. On the back of unfettered domestic Credit expansions and torrential global financial flows, EM economies were well-placed to assume the role of global growth locomotives. Regrettably, an unusually protracted period of Credit, speculative excess and malinvestment has left the EM complex vulnerable to a reversal of "hot money" flows.

EM market and economic Bubbles were at heightened vulnerability back during the unfolding summer of 2012 crisis. Unprecedented measures (including open-ended QE) prolonged Bubble excess. One would have reasonably expected $1.5 TN of new Federal Reserve "money" to weigh on the dollar and stoke further commodity price inflation - in the process benefiting developing economies. This liquidity instead flowed freely to inflating securities markets, spurring price gains and issuance, including record prices and debt sales throughout U.S. equities and corporate Credit. Too much global liquidity chasing securities markets returns has provided powerful dollar support (reminiscent of the late-nineties "King Dollar" period).

How might the unintended consequences of QE and rate manipulations come back to jeopardize market stability? While not always readily apparent, ultra-loose finance often exerts its greatest impact upon the "marginal" players. Globally, "developing" nation governments, corporations and financial institutions over recent years have enjoyed the most favorable access to finance imaginable. The perception of a reflationary global backdrop ensured too many marginal EM borrowers accumulated too much debt of which too much was denominated in U.S. dollars. In the Eurozone, the periphery countries have been the overwhelming winners amid "do whatever it takes" and global liquidity overabundance. Here at home, junk bonds, leveraged loans and all varieties of "subprime" finance have flourished amidst the liquidity bonanza.

Importantly, the windfall at the Periphery has run unabated despite the impending conclusion of Fed QE. For the most part, there has been scant indication of waning liquidity overabundance. The bulls point to a dovish Yellen Fed, hence prospects for a supportive rate backdrop for some time to come. Furthermore, they see ongoing BOJ QE and a Draghi ECB willing to grab the QE baton from the Federal Reserve. Negative global dynamics have nourished the bullish imagination.

What could go wrong? Well, all analytical eyes should now be focused "at the margin." It is the nature of speculative Bubbles to create their own self-reinforcing liquidity. It's the inherent nature of Bubbles to "overshoot" - the nature of speculative melt-ups to overwhelm markets right in the face of deteriorating fundamentals. I still see the end of QE as a pivotal development, although exuberance and speculative leveraging have continued to fuel the perception of limitless cheap liquidity. Stated differently, I believe the markets are at this point acutely vulnerable to any shift from risk embracement to risk aversion. The policy backdrop has ensured that markets remain excessively bullish in the face of bearish prospects. The various "Peripheries" would appear today be acutely vulnerable to a destabilizing reversal in market sentiment and flows.

The question is always, "Doug, what's the catalyst?" How about increasingly unstable global currency markets? How about the trials and tribulations of King Dollar? How about the potential for a serious bout of "risk off" speculative de-deleveraging unfolding without the benefit of Bernanke's reliable liquidity backstop?

I do suspect there is unprecedented global leverage in various currency "carry trades" - perhaps the key unappreciated source of speculative leverage for this global Bubble cycle. I have posited that the "yen carry" (short/sell low-yielding yen instruments to fund higher-yielding securities around the world) could be history's greatest speculative wager. Recent yen weakness has supported this huge winning trade. At the same time, recent currency market volatility and general instability have meaningfully elevated the risk of leveraged "carry trades"/speculations. Indeed, the currency markets have become a veritable minefield of risk.

The U.S. economy today commands a decent head of steam, bolstered by record securities prices, ultra-loose finance and record corporate debt issuance. This provides ammunition to the Fed hawks, boosting policy and market uncertainty. Despite unprecedented QE and a devalued yen, the Japanese economy has performed dismally. Do Japanese policymakers double-down or begin to recognize the risks associated with faltering yen confidence? Throughout Europe, economies have performed poorly. Mario Draghi talks a tough game, but there is in reality considerable uncertainty as to the ECB's ability to implement quantitative easing. There is great uncertainty and potential for the Europe to disappoint on multiple fronts. And with their currency basically tied to ours, what impact does King dollar have on a weakening China beset by overcapacity and a plethora of uneconomic industries?

The U.S. dollar has been winning on multiple fronts - European and Japanese stagnation and prospects for more central bank monetization. An increasingly alarming geopolitical backdrop has boosted the perception of dollar as safe haven. The dollar was boosted further from British pound weakness as a nervous marketplace cut exposure heading into what appears will be a close referendum on Scottish independence. And each bump in the dollar feeds the prospect for a big dollar market overshoot, in the process increasing probabilities for a destabilizing unwind of various trades around the globe and across asset classes. As commodities prices have wilted, pressure on the so-called "commodities currencies" has further inflamed King Dollar. And as U.S. securities outperform globally, more "hot money" flows to the U.S. at the expense of The Peripheries. Unprecedented liquidity abundance has provided sufficient liquidity for all. But for how long?

September 12 - Financial Times (Andres Schipani in Bogotá and John Paul Rathbone): "Venezuela is struggling to meet its international bond payments, raising the spectre of an Argentine-style default despite the Opec country's massive oil reserves. Yields on Venezuelan bonds, the third-largest constituent of JPMorgan's global emerging bond index, have risen since Caracas put Citgo, the country's US refining operation, up for sale and scrambled to reassure investors it can refinance $7bn coming due this year on its more than $80bn of sovereign debt... A Venezuelan default could be widely felt. The country accounts for 7% of emerging market benchmarks, meaning a default could force redemptions of other investments by passive index-tracking funds... Until recently, bond investors drew comfort from Venezuela's $85bn annual oil exports. But confidence was shaken this week as yields on short-dated bonds issued by PDVSA, the state owned oil company, shot above 25%."

Venezuela CDS surged 163 bps this week to 1,443. King dollar weighs on Venezuela on multiple fronts. The strong dollar places downward pressure on crude prices, Venezuela's big export. Weak commodities prices feed market nervousness and a tightening of finance for commodity-based economies and perhaps even EM generally. And a tightening of financial conditions for EM would weigh on confidence in the global economy, which would further weigh on commodity prices...

It is worth nothing that the Brazilian real dropped 1.8% Friday and 4.2% for the week. Brazil's Bovespa equities index sank 2.4% Friday and 6.2% for the week. With a weak economy and looming elections, Brazil is vulnerable. And with Brazil distinguished as a "core" Periphery market, a lot may be riding on market sentiment. To this point, exuberant global markets have been willing to overlook a litany of troubling fundamental developments - including festering social tension.

And on the topic of social instability, it is worth noting that estimates placed the number of Catalonian pro-independence protestors at 1.8 million in Barcelona on Thursday. Spain's Prime Minister Rajoy has called the referendum for an independent Catalonia unconstitutional - and has stated it won't be tolerated. Energized by next week's Scottish referendum, the Catalan independence movement appears unwilling to take Madrid's no for an answer. Spain's, at the "core" of the Eurozone Periphery, saw its bonds get walloped this week.

When I look at the likes of the UK/Scotland, Brazil and Spain, I can't help but feel that these troubling backdrops are anything but isolated and anything but unrelated to all the central bank "money" that's been slushing about. This QE onslaught continues to feed the most inequitable distribution of wealth in history. The post-2012 central bank-induced melt-up in global securities prices has too conspicuously enriched the wealthy with few trickledown benefits for the frustrated majority. There is also little doubt in my mind that Western dominance of global finance is at the heart of the alarming deterioration in the geopolitical backdrop, certainly including an aggressive Russia and increasingly assertive China.

And it's fair to question how my global macro analysis could potentially impact the U.S. markets and economy. The abbreviated response focuses on the global nature of today's Bubble. As we saw in the spring of 2013, worries of potential EM outflows can translate into fears that EM central banks might be forced to sell some of their horde of Treasuries. Moreover, currency market instability and losses in global markets lead to general risk aversion that can feed into U.S. markets through various channels.

Back in June 2012, a bout of global risk aversion corresponded to a reversal of flows from various ETF projects. This impact was felt most acutely in some of the products that traffic in less than liquid underlying securities, including municipal debt and small cap stocks.

It is certainly notable that the marketplace seemed to be showing some liquidity nervousness late this week. Friday saw the small cap Russell 2000 drop 1.0%, while the REITs were smacked for more than 2%. The week also saw outflows from both junk bond and bank loan funds. Especially with the U.S. economy bustling and the M&A market on absolute fire, the pipeline of corporate debt to sell is plumb full. From my perspective, it would appear an especially inopportune time for a surprising bout of "risk off."

Yet all that's required for a problematic bout of "risk off" is for the leveraged players to turn more cautious, spurring a reversal of flows out of U.S. equity and corporate Credit ETFs. And with bullish sentiment and global uncertainties both at extremes, one really should expect the unexpected. That Treasuries and global bond markets so overshot on the upside before abruptly reversing course this week only adds to general market instability. That the global leveraged speculating community is struggling with performance also only adds to market vulnerability.

For the Week:

The S&P500 declined 1.1% (up 7.4% y-t-d), and the Dow lost 0.9% (up 2.5%). The Utilities were slammed for 3.1% (up 9.6%). The Banks gained 1.2% (up 5.9%), and the Broker/Dealers surged 4.1% (up 8.2%). Transports slipped 0.6% (up 15.6%). The S&P 400 Midcaps dropped 1.3% (up 5.9%), and the small cap Russell 2000 declined 0.8% (down 0.3%). The Nasdaq100 slipped 0.5% (up 13.3%), and the Morgan Stanley High Tech index declined 0.7% (up 9.4%). The Semiconductors sank 1.7% (up 19.6%). The Biotechs dipped 0.2% (up 32.2%). With bullion hit for $39, the HUI gold index was down 4.0% (up 10.8%).

One-month Treasury bill rates closed the week at zero and three-month bills ended at one basis point. Two-year government yields were up five bps to 0.56% (up 18bps y-t-d). Five-year T-note yields jumped 13 bps to 1.82% (up 8bps). Ten-year Treasury yields rose 15 bps to 2.61% (down 42bps). Long bond yields gained 12 bps to 3.35% (down 62bps). Benchmark Fannie MBS yields jumped 14 bps to 3.30% (down 31bps). The spread between benchmark MBS and 10-year Treasury yields narrowed one to 69 bps. The implied yield on December 2015 eurodollar futures rose nine bps to 1.085%. The two-year dollar swap spread rose three to 24 bps, and the 10-year swap spread gained one to 13 bps. Corporate bond spreads widened. An index of investment grade bond risk rose four bps to 60 bps. An index of junk bond risk jumped 21 to 336 bps. An index of emerging market (EM) debt risk gained three to 274 bps.

Ten-year Portuguese yields rose 18 bps to 3.24% (down 290bps y-t-d). Italian 10-yr yields jumped 20 bps to 2.46% (down 167bps). Spain's 10-year yields surged 30 bps to 2.35% (down 181bps). German bund yields jumped 15 bps to 1.08% (down 85bps). French yields were up 17 bps to 1.43% (down 113bps). The French to German 10-year bond spread widened two to 35 bps. Greek 10-year yields gained 14 bps to 5.71% (down 271bps). U.K. 10-year gilt yields rose six bps to 2.53% (down 49bps).

Japan's Nikkei equities index jumped 1.8% (down 2.1% y-t-d). Japanese 10-year "JGB" yields rose three bps to a 10-week high 0.57% (down 17bps). The German DAX equities index declined 1.0% (up 1.0%). Spain's IBEX 35 equities index fell 2.3% (up 1%). Italy's FTSE MIB index was hit for 1.5% (up 11.1%). Emerging equities showed signs of vulnerability. Brazil's Bovespa index was slammed for 6.2% (up 10.5%). Mexico's Bolsa lost 0.9% (up 7.2%). South Korea's Kospi index slipped 0.4% (up 1.5%). India's bubbly Sensex equities index added 0.1% to another all-time high (up 27.8%). China's Shanghai Exchange added 0.2% to a 15-month high (up 10.2%). Turkey's Borsa Istanbul National 100 index sank 5.3% (up 14.8%). Russia's MICEX equities index fell 1.1% (down 3.0%).

Debt issuance remained quite strong ($bn from Bloomberg). Investment-grade issuers included WEA Finance $3.5bn, Goldman Sachs $2.36bn, Dow Chemical $2.0bn, John Deere Capital $1.25bn, Kinder Morgan $1.2bn, 21st Century Fox $1.2bn, US Bancorp $1.0bn, Amphenol $750 million, Brandywine $500 million, US Bank Cincinnati $500 million, Southern California Gas $500 million, Valmont Industries $500 million, New York Life $350 million, Starwood Hotels $650 million, Buckeye Partners LP $600 million, Harley-Davidson $600 million, Owens & Minor $550 million, Private Exporting Funding $400 million, Cleveland Clinic Foundation $400 million, Hospitality $350 million, PACCAR Financial $300 million, Peco Energy $300 million, Washington Aircraft $150 million, National Penn Bancshares $150 million and Washington Gas $100 million.

Junk funds saw outflows of $766 million (from Lipper). Junk issuers included California Resources Corp $5.0bn, Sanchez Energy $1.15bn, W.R. Grace & Co $1.0bn, Air Lease Corp $500 million, Whitewave Foods $500 million, AK Steel $430 million, JC Penney $400 million, American Energy $350 million, EnPro Industries $300 million and Harbinger Group $200 million.

Convertible debt issuers included Twitter $1.8bn.

The long list of international dollar debt issuers included Brazil $4.3bn, British Sky Broadcasting $2.0bn, Sweden $2.0bn, European Bank of Reconstruction & Development $1.5bn, Neder Waterschapsbank $1.5bn, Banco BTG $1.3bn, BCPE $1.25bn, Jupiter Resources $1.1bn, Ghana $1.0bn, El Salvador $800 million, Credit Suisse $780 million, Mexichem $750 million, Inversiones CMPC $500 million, ICICI Bank of Dubai $500 million, United Overseas Bank $500 million, Teine Energy $350 million, Caisse Centrale Desjardin $1.25bn, Golden State RE $250 million and Dynagas LNG Partners $250 million.

Freddie Mac 30-year fixed mortgage rates were up two bps to 4.12% (down 45bps y-o-y). Fifteen-year rates declined three bps to 3.21% (down 38bps). One-year ARM rates jumped five bps to 2.45% (down 22bps). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed rates up six bps to 4.61% (down 23bps).

Federal Reserve Credit last week expanded $4.2bn to a record $4.378 TN. During the past year, Fed Credit inflated $762bn, or 21.1%. Fed Credit inflated $1.567 TN, or 56%, over the past 96 weeks. Elsewhere, Fed holdings for foreign owners of Treasury, Agency Debt slipped $0.4bn last week to $3.338 TN. "Custody holdings" were down $15bn year-to-date, while posting a one-year increase of $62bn.

M2 (narrow) "money" supply slipped $2.1bn to $11.471 TN. "Narrow money" expanded $685bn, or 6.3%, over the past year. For the week, Currency was little changed. Total Checkable Deposits jumped $27.4bn, while Savings Deposits fell $27.3bn. Small Time Deposits were about unchanged. Retail Money Funds declined $1.7bn.

Money market fund assets gained $6.5bn to $2.593 TN. Money Fund assets were down $126bn y-t-d and dropped $66bn from a year ago, or 2.5%.

Total Commercial Paper increased $3.2bn to a two-month high $1.051 TN. CP was up $5.1bn year-to-date, with a one-year gain of $16bn, or 1.5%.

Currency Watch:

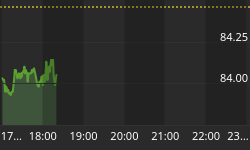

The U.S. dollar index added 0.6% to 84.24 (up 5.3% y-t-d). For the week on the upside, Danish krone and euro gained 0.1%. For the week on the downside, the Brazilian real declined 4.2%, the Australian dollar 3.6%, the South African rand 3.0%, the New Zealand dollar 2.1%, the Japanese yen 2.1%, the Canadian dollar 1.9%, the Mexican peso 1.7%, the Norwegian krone 1.3%, the South Korean won 1.1%, the Singapore dollar 0.7%, the British pound 0.4%, the Swedish krona 0.3%, the Swiss franc 0.2% and the Taiwanese dollar 0.2%.

There was notable weakness in EM currencies. The Colombian peso declined 3.1%, the Turkish lira 2.9%, the Russian ruble 1.9%, the Ukrainian hryvnia 1.4%, the Chilean peso 1.1% and the Thai baht 0.8%.

Commodities Watch:

The CRB index dropped 2.1% this week (up 0.6% y-t-d). The Goldman Sachs Commodities Index sank 2.4% (down 7.4%). Spot Gold fell 3.1% to $1,230 (up 2.0%). September Silver declined 2.9% to $18.606 (down 4%). October Crude declined $1.10 to $92.27 (down 6%). October Gasoline dropped 2.5% (down 10%), while October Natural Gas rallied 1.7% (down 9%). December Copper declined 2.0% (down 9%). September Wheat sank 6.3% (down 18%). September Corn was down another 2.2% (down 20%).

U.S. Fixed Income Bubble Watch:

September 11 - Bloomberg (Christine Idzelis): "Investors withdrew $766 million from U.S. funds that buy high-yield bonds in the past week, the second straight outflow, according to... Lipper. The pullback brings net outflows for the funds to $9.7 billion this year... Investors also pulled $342 million from U.S. leveraged loan funds, the ninth straight weekly outflow, according to Lipper."

September 12 - Bloomberg (Christine Idzel):"Junk-bond buyers have indigestion again. Speculative-grade borrowers from Jupiter Resources Ltd., an energy firm backed by Apollo Global Management LLC, to AK Steel Holding Corp. had to sweeten terms yesterday to sell at least $8.7 billion of debt. The offerings struggled as investors pulled $766 million from funds that buy the bonds in the past week. After recovering in August from a 1.3% loss in July, the worst month in almost a year, gains on the debt are evaporating again... Junk bonds have tumbled 1% this month as concern mounts that investors who've gobbled up $258 billion of the debt in 2014 are paying too much for it with too few protections just as the Federal Reserve winds down stimulus that has bolstered the market... Speculative-grade companies have sold $27.5 billion of bonds this month, the busiest start to a September on record..."

September 11 - Bloomberg (Matt Robinson and Laura J. Keller): "The riskiest borrowers are leading the busiest September in at least six years for speculative-grade bond sales in the U.S. as Moody's... warns that protections in the debt are declining. J.C. Penney Co., the retailer whose liquidity Goldman Sachs Group Inc. warned a year ago was under strain, is among issuers that have sold or are planning more than $17.5 billion in bonds this month... AK Steel Holding Corp., which hasn't posted an annual profit since 2008, is selling $430 million of notes. Clear Channel Communications Inc., the most leveraged U.S. broadcaster, raised $750 million... Companies are issuing debt with the fewest investor protections since at least 2008, according to a Sept. 8 report from Moody's."

September 12 - Bloomberg (Lauren Coleman-Lochner and Matt Townsend): "RadioShack Corp.'s effort to seek financing and stave off bankruptcy raises a key question for investors, analysts and the customers who've shunned the electronics retailer for years: What's worth saving here? The company, which said yesterday it was in advanced talks with creditors and other parties on a potential rescue package, has suffered three years of declining sales and 10 straight quarterly losses. The stores have become increasingly irrelevant to shoppers, who can get their mobile devices and electronic doodads from e-commerce sites or Wal-Mart Stores Inc."

September 8 - Bloomberg (Kristen Haunss): "More than a year after regulators warned about deteriorating standards in leveraged loans, a Moody's... report shows that risks to lenders are growing. The percentage of the debt that Moody's considers as having weak or the weakest investor protections known as covenants climbed to 65% of the market in the first half of this year from 60% in 2013 and 42% in 2012... That's the highest since at least 2008... 'Lenders are being exposed to rising risk as they forfeit key levers they have traditionally been able to pull when a company is starting to experience financial distress,' Moody's analysts led by Jessica Reiss wrote..."

September 9 - Bloomberg (Christine Idzelis): "The biggest investor retreat from the U.S. leveraged loan market since 2011 is taking place just as a flurry of mergers and acquisitions needs to get funded with non-investment grade debt. Dealmakers are planning more than $85 billion in loans, including about $10 billion that's now being marketed... The drop in demand for leveraged loans that last month led companies including Charter Communications Inc. to German chemicals company Styrolution Group GmbH to postpone merger financings has continued in September with investors pulling $435 million from funds that buy the debt last week, bringing net withdrawals for the year to $4.3 billion. The flight has led borrowing costs to jump to a more than two-year high."

September 8 - Financial Times (Judith Evans): "Investors have been piling into bond exchange traded funds at an accelerating pace, lured not only by the search for yield but the promise of liquidity that may be greater than that of the underlying market. But as ETFs form an ever growing part of the bond markets they mirror, watchdogs including the International Monetary Fund have raised concerns about the potential for liquidity freezes in the event of a sell-off... What was a $60bn global bond ETF market in 2007 had swelled to $390bn at the end of July 2014, according to... ETFGI. Post-crisis regulations have led to a fall in dealers' fixed-income inventories, which has reduced liquidity and trading volumes for individual bonds, pushing institutional investors into ETFs instead. Tactical use of bond ETFs is also on the increase, says Nikolaos Panigirtzoglou, global market strategist at JPMorgan Chase & Co in London. 'ETFs are being used as vehicles to gain access to asset classes that are not very liquid, such as high yield and emerging market bonds,' he says. 'As a result, ETFs now account for a decent proportion of total trading volumes.' ...Some $39.3bn of assets flooded into fixed income ETFs between the start of 2014 and the end of July, almost double the amount for the same period last year."

September 9 - Financial Times (Tracy Alloway): "Sales of bonds backed by riskier US corporate loans have surged to their highest level in seven years, helping to fuel a leveraged lending boom that is concerning regulators. So-called collateralised loan obligations, or CLOs, have staged a striking recovery in the years since 2008, when securitised bundles of subprime mortgages were blamed for inflating the housing bubble and exacerbating the ensuing financial crisis. Bonds backed by home mortgages not guaranteed by the US government's housing financiers have since largely disappeared, but sales of CLOs comprised of leveraged loans made to low-rated companies are poised to overtake levels last seen in the 2006-2007 credit boom as investors look for higher-yielding assets and companies take advantage of low borrowing costs. Some analysts predict this year's issuance volume could eclipse the record $97bn worth of deals sold at the height of the credit bubble back in 2006. On Friday, analysts at JPMorgan Chase increased their forecast for full-year sales from $90bn-$100bn to $105bn-$115bn... Leveraged loan issuance stands at $404.7bn so far this year - slightly below the $424.4bn sold in the same period last year but still at hefty historical levels. Meanwhile, CLOs now boast a record 55% ownership of the total leveraged loan market, according to S&P Capital IQ - up from 48.2% back in 2006. 'Borrowing costs are low right now so people are taking full advantage of that to get loans and get them funded through the CLO market,' said Mr Flanagan."

September 10 - Bloomberg (Sarah Mulholland): "The U.S. government probe into auto loans made to people with spotty credit is doing little to derail sales of bonds backed by the debt, even as investors demand more to own the riskiest pieces. Lenders are planning about $2 billion of securities that are either predominantly backed by subprime loans and leases or include significant chunks of the debt... The pending sales show how cheap funding for firms that make the loans is continuing with little disruption as fixed- income investors seeking an alternative to low interest rates buy up the debt. Even before the latest deals, companies sold $14.2 billion of the securities through Aug. 19, compared with $21.5 billion issued in all of 2013, according to Barclays Plc. The pace is the fastest since the record $27 billion in 2006."

Federal Reserve Watch:

September 8 - Financial Times (Robin Harding): "The US Federal Reserve's forward guidance on future interest rates has come up for debate after a stream of central bank officials declared the current wording needs to change. In the past few days, officials from every part of the rate-setting Federal Open Market Committee - hawks and doves, regional presidents and Washington governors - have called for new language. Their remarks could mean a move at the September FOMC meeting in 10 days, although there is little consensus yet on new wording, so a shift might have to wait until next month. A particular issue is the Fed's guidance of low rates for a 'considerable time' after it stops buying assets in October... 'Significant parts of the FOMC statement need to change,' said Jerome Powell, a Fed governor... 'I believe it is time for the Committee to reformulate its forward guidance,' said Loretta Mester, president of the Cleveland Fed, in a speech..."

September 9 - Bloomberg (Cheyenne Hopkins and Jesse Hamilton): "The biggest U.S. banks must decide whether to voluntarily reduce their size and complexity or face capital charges that are some of the toughest in the world, the Federal Reserve's top financial-regulation official said... Fed Governor Daniel Tarullo outlined the central bank's plans for capital surcharges surpassing those of international regulators at a Senate hearing on progress in implementing rules to prevent a repeat of the 2008 credit crisis... 'We're all trying to come to grips with what we really need in order to provide more assurance that these firms do not threaten the financial system,' Tarullo told the Senate Banking Committee... Banks will have to weigh a trade-off between complexity and capital demand and may choose to trim the cost by shrinking their 'systemic footprint.'"

U.S. Bubble Watch:

September 9 - PRNewswire: "As college students across the country move into their dorm rooms, firm up their class schedules and embark on a new chapter in their lives, many will do so with the help of a student loan. Experian... analyzed student loan trends spanning from 2008 through 2014 in the United States. Findings from the study show that consumer debt is decreasing in every major consumer lending category, with the exception of student loans. Student loans increased by 84% since the recession (from 2008 to 2014) and surpassed home equity loans/lines of credit, credit card and automotive debt."

September 12 - Bloomberg (Laura J. Keller, Jodi Xu and Matt Robinson): "Twitter Inc. raised $1.8 billion after boosting its first-ever debt offering, selling notes that owners can convert into the microblogger's stock at a price that's 47% above yesterday's closing level."

September 9 - Bloomberg (Michael Bathon and Christopher Palmeri): "Trump Entertainment Resorts... filed for bankruptcy, putting a fifth Atlantic City casino in danger of closing if it fails to negotiate concessions with union members... Its Trump Plaza is set to cease operations on Sept. 16. The Trump Taj Mahal may also shut in November, the company said. It's the company's third bankruptcy. Three other casinos have closed in the city this year, including Caesars Entertainment Corp.'s Showboat and the bankrupt Revel Casino Hotel last week. If the Taj Mahal shutters along with the Plaza, another 2,800 employees will be put out of work in a city already losing 5,200 casino jobs this month."

September 9 - New York Times (Michelle Higgens): "What will $1 million buy in New York City? A diamond-encrusted Cartier men's watch. A small fleet of 2014 Bentley Continentals. Or maybe your very own parking spot in SoHo. A new development, 42 Crosby Street, is pushing the limits of New York City real estate to new heights with 10 underground parking spots that will cost more per square foot than the apartments being sold upstairs. The million-dollar parking spots will be offered on a first-come-first-served basis to buyers at the 10-unit luxury apartment building being developed by Atlas Capital Group at Broome and Crosby Streets, itself the former site of a parking lot."

Central Bank Watch:

September 10 - Bloomberg (Corina Ruhe): "Options for monetary policy that the ECB can take have reached their limits,' Eurogroup Chairman Jeroen Dijsselbloem tells Dutch lawmakers... Dijsselbloem also says: 'All measures the ECB takes cannot be sufficient unless countries take measures themselves... The measures ECB takes, with low inflation and the expensive euro, I understand and I can defend. But these decisions will not have a permanent impact when countries don't carry out the structural reforms we expect.' 'France is not there by far, according to the latest numbers... It's essential for France and Italy to catch up on structural reforms... The additional two years France received from the commission are nearing their end. The latest French numbers show it's far away from that limit..."

September 11 - Wall Street Journal (Brian Blackstone and Ulrike Dauer): "The European Central Bank's recent decision to buy private-sector debt instruments isn't a prelude to purchases of government bonds, ECB executive board member Yves Mersch said Wednesday, suggesting his hurdle remains high for the ECB to follow other major central banks with large-scale public debt purchases. 'The purchase of government bonds would raise substantial institutional, instrumental and legal questions,' Mr. Mersch said..."

Europe Watch:

September 11 - Bloomberg (Charles Penty and Esteban Duarte): "Spanish Prime Minister Mariano Rajoy says there's no doubt the constitutional court will stop Catalonia voting on independence. Investors aren't so sure. Spain's 10-year yields have risen for three straight days since a poll in Scotland showed the pro-secession Yes campaign has wiped out the Noes' advantage with less than two weeks to go before a referendum on Sept. 18. Catalan separatists aim to bring more than 1.5 million people onto the streets of Barcelona today to pressure Rajoy to let their vote go ahead in November. 'There has been a bit of contagion from Scotland for the first time and with these important dates coming up, the markets will get more nervous,' said Serafi Rodriguez, a fixed income trader at Morabanc Grup SA, which oversees almost 7 billion euros ($9 billion). 'If Scotland has its vote, then people will say it has happened there, why can't it happen here?' Rajoy told a meeting of his ruling People's Party... that he has prepared 'all measures' to prevent Catalans from holding the independence referendum. The vote can't take place because it would be unconstitutional, Rajoy says."

September 10 - Financial Times (Chris Bryant): "Berlin dashed hopes that it might open the door to higher public investments to spark a recovery in the eurozone when its finance minister insisted that spending funded by new debts would not deliver growth and employment. Wolfgang Schäuble, German finance minister, told the lower house of parliament... that calls 'for the use of more and more public money and the acceptance of higher deficits and debts is leading us astray'. 'Growth and jobs don't come about via higher deficits as if that were the case we [in Europe] really wouldn't have any problems at the moment... Only innovation, structural reforms, investment and reliable [investment] conditions and, above all, trust in the sustainability [of public finances] will help.' Mr Schäuble spoke amid rising pressure on Germany to act to alleviate the threat of prolonged stagnation and deflation in the eurozone."

September 9 - Reuters (Francesca Piscioneri and Gavin Jones): "Italian Prime Minister Matteo Renzi said... that the country's economic growth would be about 'zero' this year, a sign the euro zone's third-biggest economy is struggling to climb out of its third recession in six years. Renzi's forecast is far lower than the government's previous prediction for a 0.8% increase... Italy needs to slash 20 billion euros in spending next year to keep its deficit at or below the EU deficit limit of 3% of output while making labour-tax cuts and maintaining recent income-tax reductions."

Germany Watch:

September 10 - Bloomberg (Rainer Buergin and Brian Parkin): "German Finance Minister Wolfgang Schaeuble said he's working with his French counterpart on ways to create a market for asset-backed securities that's strong enough not to rely on the European Central Bank as the main buyer. Small and medium-size companies in Europe face obstacles tapping capital even though the ECB has provided an 'overabundance of liquidity,' an impasse that can't be resolved by adding even more, Schaeuble said in a speech in the lower house of parliament... 'We're working on the revitalization of a market for high- quality securitizations in Europe, which were discredited by the banking crisis... Creating securitization standards doesn't mean that central banks have to be the main buyers of such securitizations. We want to make them marketable.'"

September 9 - Bloomberg (Alessandro Speciale): "German exports rose above 100 billion euros ($129bn) for the first time in July and the trade surplus climbed to an all-time high, even as escalating sanctions against Russia threatened trade flows. Exports gained the most in more than two years, climbing 4.7% from June to 101 billion euros... The trade gap widened to 23.4 billion euros from 16.6 billion euros."

Global Bubble Watch:

September 8 - Reuters (Chris Vellacott): "With returns on government bonds at rock-bottom prices, sovereign wealth funds are muscling into stock markets and other higher-yielding assets like real estate at a rate that private investors warn could destabilize the world economy. Since central banks cut interest rates to record lows in a bid to shore up flagging economic growth, world governments have had to look further afield to grow public pension money or central bank currency reserves. But the resulting tide of money is in danger of distorting markets, causing prices to reflect political priorities rather than financial reality, insiders say. It's also threatening to inflate the very price bubbles that central bank teams globally are working so hard to prevent, experts suggest. 'There is quite clearly both an actual and a potential conflict of interest... There should be some sort of code of practice,' said David Marsh, managing director at the Official Monetary and Financial Institutions Forum (OMFIF)... Sovereign investors manage assets worth $29.1 trillion - equivalent to 40% of the global economy - which are held by 157 central banks, 156 public pension funds and 87 sovereign wealth funds, according to OMFIF."

September 10 - Bloomberg (Kiel Porter and Sabrina Willmer): "Some of the world's biggest investors in leveraged-buyout funds are themselves using unprecedented levels of debt to boost returns. 'Leverage is a double-edged sword,' said Oliver Gottschalg, a professor at French business school HEC Paris. 'It can boost the performance on the upside and rapidly eat into capital on the downside. The more leverage you apply, the more extreme the outcome will be for the investor.' ...Investors are poised to buy $30 billion of fund stakes this year, according to Evercore Partners Inc., twice the amount in 2007, before the credit crisis. Borrowing lets the investors get cash upfront from their holdings, rather than wait for assets in a fund to be sold, or helps them fund new investments without having to ask their backers for money immediately. For banks, the loans can produce higher returns relative to loans to companies of a similar credit quality, said Bill Murphy, a managing director at advisory firm Cogent Partners LP. The number of banks willing to provide funding has more than tripled in recent years. Bank of America, JPMorgan Chase & Co. and Nomura Holdings Inc. have joined smaller lenders such as Lloyds, Natixis and Royal Bank of Scotland Group Plc that have traditionally served the market..."

September 8 - Financial Times (Andrew Bolger): "The buoyant European market for corporate credit reached a new high with Lufthansa issuing a €500m bond with a yield of just 1.125% - in spite of suffering its second pilots' strike in a week. The low coupon on the five-year bond, which was heavily oversubscribed on Friday, was notable because the German airline's debt has a 'junk' rating from Moody's. The deal could fuel concerns that investors' hunger for yield is blinding them to the potential risks in junk bonds..."

September 10 - Bloomberg (Julia Leite and Filipe Pacheco): "Traders are ratcheting up the cost to insure Brazilian debt by the most in 10 months after Moody's... said it's considering a downgrade of the nation to the cusp of junk... Brazil is now perceived to be less creditworthy than either Uruguay, Colombia or Panama, three countries in Latin America with the same rating from Moody's. The move comes less than a month before President Dilma Rousseff, who's struggling to jump-start an economy reeling from its first recession in five years, seeks re-election. Moody's... raised the possibility Brazil could eventually be lowered to non-investment grade status..."

September 10 - Bloomberg (Tom Metcalf): "Microsoft Corp.'s potential acquisition of Mojang AB, the Swedish developer behind the Minecraft online game, could make the game's 35-year-old creator Markus Persson a billionaire. Persson controls 71% of the business through holding company Notch Enterprises AB, according to its 2013 annual report. Notch Enterprises owns all of Notch Development AB, which owns Mojang and the licensing rights for Minecraft. Including dividends he's received since 2011, Persson would have a $1.5 billion fortune if the deal goes through..."

Geopolitical Watch:

September 8 - Bloomberg (Robert Hutton): "Scottish independence increasingly looks like an iceberg that could sink Prime Minister David Cameron's government and the opposition Labour Party. And like the passengers on the Titanic, they never saw it coming. Yesterday's YouGov Plc poll putting the Yes vote on 51% sparked a fresh effort from supporters of the union to urge Scots to come back from the brink. About 100 Labour lawmakers will travel to Scotland this week to campaign for a No vote, while Conservative Chancellor of the Exchequer George Osborne offered more powers over taxes and spending to the Scottish Parliament -- if voters opt to stay part of the U.K."

September 11 - Bloomberg (Esteban Duarte): "Hundreds of thousands of people marched through the center of Barcelona today demanding the right to vote on independence from Spain, in a direct challenge to Prime Minister Mariano Rajoy. Demonstrators chanted slogans and waved the red, yellow and blue flags of an independent Catalonia at a rally that filled the city's two main boulevards. Local police estimated 1.8 million people were gathered... 'Prime minister, open the polling stations,' shouted Carme Forcadell, lead organizer of the protest, as she addressed the crowd... 'We will vote and we will win.' As Scots wrestle with how to vote in a Sept. 18 referendum, Catalans are struggling with Rajoy's government over whether they'll get to hold their own ballot. Rajoy says the plan for a November referendum is unconstitutional and has pledged to prevent it. Nationalists say he can't just ignore the will of the people."

September 11 - Financial Times (Demetri Sevastopulo): "China and Japan are heading towards military conflict, according to a majority of Chinese surveyed on ties between the Asian powers in a Sino-Japanese poll. The Genron/China Daily survey found that 53% of Chinese respondents - and 29% of the Japanese polled - expect their nations to go to war. The poll was released ahead of the second anniversary of Japan's move to nationalise some of the contested Senkaku Islands in the East China Sea."

September 10 - Bloomberg (David Tweed and Ting Shi): "The U.S. should stop its 'close in' aerial and naval surveillance of China, a senior Chinese military officer told President Barack Obama's National Security Adviser Susan Rice, the PLA Daily reported. General Fan Changlong told Rice on the last day of her three-day visit to Beijing that China hopes the U.S. can take the 'correct view' of the development of China's military, better manage and control frictions, and decrease and even stop close-in military, ship and aircraft surveillance, the state-run newspaper of the People's Liberation Army."

September 12 - Xinhua: "Cooperation between China and Russia is advancing smoothly, as can been seen by the increase in high-level contact since 2013. Thursday' s meeting between Chinese President Xi Jinping and his Russian counterpart, Vladimir Putin, ahead of the 14th summit of the Shanghai Cooperation Organization (SCO)... is their fourth this year. Xi has held talks or met with Putin nine times since becoming China's President in March 2013. Energy cooperation has been the highlight of China-Russian relations... Alongside successful energy cooperation, there is a fresh impetus in financial areas. China is the fourth-largest source of investment for Russia. Last year, direct investment in Russia hit 4 billion dollars, five times the amount in 2012. On the horizon are specific plans for joint endeavors in high-speed rail and satellite navigation, with other large-scale projects-- development of a long-range wide-body passenger jet and heavy-lift helicopter..."

September 12 - Xinhua: "China supports Russia taking over the presidency of the Shanghai Cooperation Organization (SCO) next year, Chinese President Xi Jinping said... Xi made the remarks at a meeting with his Russian counterpart, Vladimir Putin, ahead of the 14th summit of the SCO, which groups China, Russia, Kazakhstan, Kyrgyzstan, Tajikistan and Uzbekistan. On the upcoming Dushanbe summit, the two leaders agreed that under the current situation, SCO members should strengthen unity, mutual trust and cooperation, and promote the simultaneous advancement of security and economy... Besides its six members, the SCO also has Afghanistan, India, Iran, Mongolia and Pakistan as observers, and Belarus, Turkey and Sri Lanka as dialogue partners."

China Bubble Watch:

September 12 - Bloomberg: "China's broadest measure of new credit trailed analyst estimates in August, adding to the government's challenge to meet its economic-growth target amid a slumping property market and a pullback in manufacturing. Aggregate financing was 957.4 billion yuan ($156bn, compared with the 1.135 trillion yuan median estimate... New local-currency loans were 702.5 billion yuan, and M2 money supply grew 12.8% from a year earlier. Today's report adds to evidence the economy is losing steam after July aggregate financing slumped and recent data showed moderation in manufacturing and a drop in imports."

September 12 - Bloomberg (Raymond Colitt): "A Chinese bank was saddled with $650 million of defaults from an off-balance-sheet lending arrangement that channeled money to one of its shareholders and an affiliate, according to a state media report. Evergrowing Bank... repaid 3.7 billion yuan ($600 million) of principal and 300 million yuan of interest on Aug. 29 as guarantor for the borrowing, the People's Daily said... Intricate structures for some off-balance-sheet lending by China's banks make it harder for investors to assess risks to the financial system after an explosion in shadow banking. In some cases, banks have channeled money to companies through trusts or brokerages to bypass government limits on lending and requirements relating to provisions and capital."

September 11 - Dow Jones (Colum Murphy): "Car sales in China showed signs of cooling in August, adding to the uncertainty facing foreign auto makers there as authorities push ahead with antitrust investigations of industry players. Sales of passenger cars rose 8.5% last month from a year earlier, the weakest pace of expansion since a 7.9% gain in March..."

September 8 - Bloomberg: "China's trade surplus climbed to a record in August as exports rose on the back of increased shipments to the U.S. and Europe, while imports fell for a second month as a property slump hurt domestic demand. Exports increased 9.4% from a year earlier... Imports unexpectedly dropped 2.4%, leaving a trade surplus of $49.8 billion... Languishing domestic demand underscores risks to the government's economic-growth target this year of about 7.5% as home prices and construction fall..."

September 8 - Bloomberg: "Jiang Jianqing, chairman of Industrial & Commercial Bank of China Ltd., earned less than 2% of Jamie Dimon's compensation last year while reporting twice the profit of JPMorgan Chase & Co. Instead of a reward, Jiang is poised for a pay cut. China's government said last month it will reduce salaries for executives at state-owned companies because 'unreasonably high' incomes have become a source of public discontent. The biggest banks have pledged to implement the plans, part of President Xi Jinping's campaign to bolster support by tackling government waste and corruption. The risk is that lenders will bleed talent just when China needs skilled managers to grapple with interest-rate deregulation, an explosion in shadow banking and rising levels of soured credit."

Latin America Watch:

September 12 - Bloomberg (Raymond Colitt): "Marina Silva gradually would unwind Brazil's currency intervention program that has helped the real become the only major Latin American currency to appreciate this year, the presidential candidate's economic adviser Eduardo Giannetti said. 'It's not part of our philosophy to surprise with an unexpected shock,' he said... 'We want to do things gradually and previously announced.' The real weakened 1.9% to 2.3421 per U.S. dollar..., the biggest decline this year on speculation a Silva administration would immediately halt the central bank currency intervention."

September 10 - Bloomberg (Camila Russo): "Argentina is tightening its grip on the country's currency market as international reserves decline following its second debt default in 13 years. Argentine banks must now seek government authorization for dollar purchases of $150,000 or more, down from a previous threshold of $300,000... South America's second-biggest economy is boosting controls on dollar purchases to retain foreign-currency reserves it relies on to pay debt and imports..."

September 10 - Bloomberg (Jose Orozco and Nathan Crooks): "Venezuela's annual inflation accelerated at the fastest pace in 16 years as collapsing imports made the few products made locally dearer. Consumer prices rose 63.4% in August from last year, exceeding the 62% increase in July... Tighter dollar rationing caused a 33% decline in imports in the first half of the year compared to the same period in 2012, the biggest import contraction since the 1980s..."

September 12 - Bloomberg (Michael McDonald): "Costa Rica's fiscal deficit could widen to 8.2% of GDP by 2019 from a forecast of 6.7% next year if changes aren't made to the country's tax code, deputy Finance Minister Fernando Rodriguez said... 'Debt is the main problem because now we will need to go into debt in order to pay our debt.'"

EM Bubble Watch:

September 10 - Bloomberg (Ye Xie): "The European Central Bank is overtaking the Federal Reserve as the biggest driver of emerging-market assets, giving bonds from Brazil to Poland a boost from lower borrowing costs in the euro area, according to Goldman Sachs Group Inc. The... 90-day correlation between bond yields in emerging markets and euro-zone countries has increased to 0.52 from 0.18 in May... President Mario Draghi unexpectedly cut all three of the central bank's main interest rates on Sept. 4 and signaled at least 700 billion euros ($906bn) in stimulus, just as the Fed is paring back its monetary accommodations."

September 9 - Bloomberg (Ken Kohn and Minh Bui): "China and Hong Kong led a slowdown in net inflows into U.S. exchange-traded funds that invest in emerging-market equities during the holiday-shortened week ended Sept. 5. Total flows into emerging-market ETFs that invest across developing nations as well as those that target specific countries decreased to $363.1 million from $1.3 billion in the previous week..."

September 10 - Bloomberg (Constantine Courcoulas): "The [Turkish] lira slid to the lowest level since March and government bonds fell after weaker-than-expected economic growth data raised concern that central bank interest- rate cuts weren't doing enough to spur domestic demand... Yields on 10-year bonds climbed five basis points to 9.19%, taking a three-day gain to 28 bps. The Borsa Istanbul 100 Index of equities decreased 0.9% to the lowest level since Aug. 25. Turkey's gross domestic product grew 2.1% in the three months through June, missing the 2.8% median estimate..."

India Watch:

September 12 - Bloomberg (Jeanette Rodrigues): "India's retail inflation held near 8% while growth in factory output slowed more than economists estimated before the central bank reviews one of Asia's highest interest rates... Industrial production rose 0.5% in July versus 1.8% predicted in a separate survey..."

September 10 - Bloomberg (Anoop Agrawal, Shikhar Balwani and Yumi Teso): "Indian companies are raising record amounts from overseas bond sales amid the lowest debt costs in at least nine years and policy efforts to revive the economy. The $15.1 billion of offerings so far this year exceeds issuance in the whole of 2013. The average yield on Indian dollar securities slid 131 bps in 2014 to 4.39%..."

September 10 - Bloomberg (Bhuma Shrivastava and Santanu Chakraborty): "India's stock-markets regulator is extending its reach into mango orchards, timeshare resorts and goat farms in a crackdown on unregistered investment funds to root out suspected Ponzi-like schemes. The Securities & Exchange Board of India... has issued orders against 40 companies since May, five times the number it censured in the previous 12 months... 'Where there is money, there are bound to be some sharks,' Finance Minister Arun Jaitley told Parliament's lower house..."

Japan Bubble Watch:

September 8 - Reuters (Leika Kihara): "Japanese policymakers warned on Tuesday that rapid fluctuations in the yen were undesirable for the economy, suggesting that further sharp declines in the currency may be unwelcome after its drop to a six-year low against the dollar. Economics Minister Akira Amari said that while markets, not policymakers, determine yen levels, it was desirable for the Japanese currency to stabilize at levels that reflect economic fundamentals. 'It's not good for Japan and the global economies for currencies to have big fluctuations, regardless of whether they move up or down,' Amari told a news conference..."

September 10 - Bloomberg (Mariko Ishikawa and Masaki Kondo): "The Bank of Japan might have paid more than face value for treasury discount bills yesterday as it pushes ahead with unprecedented monetary easing. The BOJ bought 500 billion yen ($4.7bn) of securities maturing in less than a year from the secondary market yesterday, including securities that yielded minus 0.004% the previous day... 'The BOJ could have avoided buying negative-yield bills and it didn't, meaning it showed willingness to offer negative yields,' said Naomi Muguruma, ...economist at Mitsubishi UFJ Morgan Stanley Securities..."