Come get your commodities and inflation swaps here! Big discount on inflation protection! Come get them while you can! These deals won't last long!

Like the guy hawking hangover cures at a frat party, sometimes I feel like I am in the right place, but just a bit early. That entrepreneur knows that hangover cures are often needed after a party, and the people at the party also know that they'll need hangover cures on the morrow, but sales of hangover cures are just not popular at frat parties.

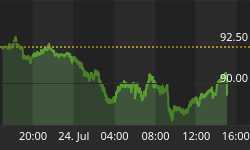

The 'disinflation party' is in full swing, and it is being expressed in all the normal ways: beat-down of energy commodities, which today collectively lost 3.2% as front WTI Crude futures dropped to a 2-year low (see chart, source Bloomberg),

...10-year breakevens dropped to a 3-year low (see chart, source Bloomberg),

...and 1-year inflation swaps made their more-or-less annual foray into sub-1% territory.

So it helps to remember that none of the recent thrashing is particularly new or different.

What is remarkable is that this sort of thing happens just about every year, with fair regularity. Take a look at the chart of 10-year breakevens again. See the spike down in late 2010, late 2011, and roughly mid-2013. It might help to compare it to the chart of front Crude, which has a similar pattern. What happens is that oil prices follow a regular seasonal pattern, and as a result inflation expectations follow the same pattern. What is incredible is that this pattern happens with 10-year breakevens, even though the effect of spot oil prices on 10-year inflation expectations ought to be approximately nil.

What I can tell you is that in 12 of the last 15 years, 10-year TIPS yields have fallen in the 30 days after October 15th, and in 11 of the past 15 years, 10-year breakevens were higher in the subsequent 30 days.

Now, a lot of that is simply a carry dynamic. If you own TIPS right now, inflation accretion is poor because of the low prints that are normal for this time of year. Over time, as new buyers have to endure less of that poor carry, TIPS prices rise naturally. But what happens in heading into the poor-carry period is that lots of investors dump TIPS because of the impending poor inflation accretion. And the poor accretion is due largely to the seasonal movement in energy prices. The following chart (source: Enduring Investments) shows the BLS assumed seasonality in correcting the CPI tendencies, and the actual realized seasonal pattern over the last decade. The tendency is pronounced, and it leads directly to the seasonality in real yields and breakevens.

This year, as you can tell from some of the charts, the disinflation party is rocking harder than it has for a few years. Part of this is the weakening of inflation dynamics in Europe, part is the fear that some investors have that the end of QE will instantly collapse money supply growth and lead to deflation, and part of it this year is the weird (and frustrating) tendency for breakevens to have a high correlation with stocks when equities decline but a low correlation when they rally.

But in any event, it is a good time to stock up on the "cure" you know you will need later. According to our proprietary measure, 10-year real yields are about 47bps too high relative to nominal yields (and we feel that you express this trade through breakevens rather than outright TIPS ownership, although actual trade construction can be more nuanced). They haven't been significantly more mispriced than that since the crisis, and besides the 2008 example they haven't been cheaper since the early days (pre-2003) when TIPS were not yet widely owned in institutional portfolios. Absent a catastrophe, they will not get much cheaper. (Importantly, our valuation metric has generally "beaten the forwards" in that the snap-back when it happens is much faster than the carry dynamic fades).

So don't get all excited about "declining inflation expectations." There is not much going on here that is at all unusual for this time of year.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"