U.S. stocks closed higher on Friday, with major indexes notching a fifth straight weekly advance after China's central bank cut its benchmark interest rate and its euro zone peer announced asset purchases in efforts to boost each region's economy. China and maybe Europe are taking over the lead in providing "easy money" after The People's Bank of China said it was cutting one-year benchmark lending rates for the first time in more than two years. The move came after European Central Bank head Mario Draghi said "excessively low" inflation had to be raised quickly by whatever means necessary, rekindling expectations the ECB will move to stimulate the euro zone economy. The ECB said it started buying asset-backed securities to encourage banks to lend and revive the economy. "What it suggests is that these central banks are prepared to do even more to stimulate growth, to stimulate demand, and that always equates to better stock markets," said Quincy Krosby, a market strategist at Prudential Financial.

Listen up, you can find 100 or 1,000 analysts who will proffer conflicting opinions on why the market should've or shouldn't have performed as it has since the recession started. But I don't care who you talk to, no knowledgeable market watcher can seriously deny that worldwide central banking authorities various forms of Quantitative Easing (QE) is the steroid that has juiced stock markets to stratospheric levels. We can talk about and debate innumerous theories on how to price stocks and what factors will influence whether shares will go up or down. However, at its most basic core, what drives the price of any investment is the straightforward, simple supply and demand equation. If there are more buyers (demand) than there are sellers (supply) the price has to go up and will continue to rise until there is equilibrium with demand equaling supply. Conversely, if there is more supply (sellers) than there are buyers (demand) the price will always drop until there is equilibrium. You can do quantitative analysis and apply all the advanced economic theory you want, but in the end it is the basic demand = supply equation that will drive the price. The reason all the 'expert' financial prognosticators keep getting it wrong about a market correction, crash, etc. is because they ignore that fact central banks around the word have supplied unlimited demand 'QE' to keep stock prices afloat. Company earnings, political system dysfunction, global political and economic unrest, chronically poor labor markets, etc., none of it have really mattered. A lot of folks will make the claim that the strengthening economy is why the stock market is making record highs, if that were really true there is no way the Democrats would have gotten crushed in the election weeks ago if the economy was thriving the way the Obama administration claims. "Central bank intervention is the No. 1 thing investors worldwide are looking at right now," said Mike Serio, regional chief investment officer at Wells Fargo Private Bank.

Both the Dow and S&P ended at records. For the week, the Dow rose 1 percent; the S&P added 1.2 percent and the Nasdaq rose 0.5 percent. It was the fifth straight weekly advance for all three. The latest records extended a comeback in the S&P 500, which has increased 11 percent since plunging in mid-October. A strong third-quarter earnings season, on top of a recent string of positive U.S. economic data on housing, jobs and manufacturing, have helped put investors in a buying mood.

Another tool to help confirm the overall market trend is the Bullish Percent Index (BPI). The Bullish Index is a popular market "breadth" indicator used to gauge the internal strength/weakness of the market. It is the number of stocks in an index (or sector) that have point & figure buy signals relative to the total number of stocks that comprise the index (or sector). So essentially it is the percentage of stocks that have buy signals. Like many of the market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. If the market is strong and moving up, the BPI should also be moving up as more and more stocks make the "buy list." When the market moves higher, the BPI should also move higher to confirm the market's strength. As seen in the chart below, the S&P 500 BPI has been heading higher for the past month, which confirms the index's overall strength.

Similar to the S&P 500 index above, the NYSE Bullish Percentage Index below further confirms large cap stocks longer-term bullishness over the past month.

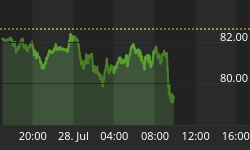

In the updated chart below the strong dollar is keeping a lid on treasury securities and commodity prices such as precious metals.

Market Outlook

Let's talk turkey. According the Stock Trader's Almanac, trading around Thanksgiving has a bullish tendency perhaps buoyed by the "holiday spirit" that was first published in the 1987 Stock Trader's Almanac. For 35 years prior to 1987, the Wednesday before and the Friday after Thanksgiving combined were up 33 times. The only declines were in 1964 and 1965. Subsequently, this trend changed. In the 27 years since 1987, there have been 11 declines and 16 advances. The best short-term trade appears to go long into weakness next week or on Monday of Thanksgiving week and selling into any subsequent rally by the end of Thanksgiving week, but remain nimble as events like Greece's debt crisis in 2011 can cancel Thanksgiving on Wall Street. Also of note is the change in the yearend rally. Prior to 1987, from the close of trading on the Friday after Thanksgiving to yearend, the DJIA rallied only 18 times in 35 years. As Thanksgiving bullishness lost steam in 1987, the rally afterwards occurred more frequently. Since 1987, DJIA has logged gains in 22 of 27 years from the close on Friday after Thanksgiving to yearend.

Asset classes that benefit from low inflation and are considered 'safe bets' continue to be fourth-quarter market leaders. A positive sign for equities is the smaller capitalization indexes like the Russell 2000 and Midcap 400 continue to lead the stock market over their larger cap brethren. This suggests that investors are willing to accept higher risk and also means they expect the domestic economy to remain strong compared to global economies.

Recently we mentioned "...Expect a price breakout from the current tight trading range..." as presented in the updated chart below, the Momentum Factor ETF (MTUM) broke out above its resistance level. A basic technical analysis mantra is when the price rises above a resistance level, that level converts to the new support line. If this analysis is confirmed look for the price to continue moving higher with the dotted line below as the support level. One reason the price moved higher is the low volume noted below. It is relatively easy to move the market higher with low trading volume if everybody is rowing in the same direction, especially if momentum is neutral.

According the Stock Traders' Almanac, since last closing at a new all-time high on March 4, 2014, the Russell 2000 has had more than its fair share of underperformance. Such poor performance has frequently been cited as a "worrisome" market divergence. However this divergence is not at all unusual from March to late November than many would believe. In the chart below, thirty-six years of daily data for the Russell 2000 index of smaller companies are divided by the Russell 1000 index of largest companies, and then compressed into a single year to show a yearly pattern. When the graph is descending, big blue chips are outperforming smaller companies; when the graph is rising, smaller companies are moving up faster than their larger brethren. In a typical year the smaller fry stay on the sidelines while the big boys are on the field. Then, around late November, small stocks begin to wake up and in mid-December, they take off. Should the Russell 2000 fail to show signs of strength by the end of the year, then its lagging performance would then be a concern.

Circled in the graph below is the point where we said last week "...Notice in the one-week CBOE Volatility Index (VIX) graph below the indicator is beginning to creep higher as investors get a little nervous with stocks at lofty levels..." In the updated graph you can see the Volatility index sank back to its lows as the S&P 500 index reached new all-time highs.

Options Put/Call ratio is another metric that we monitor for warning signs of an overextended market. The box below highlights the total Put/Call ratio number, which is currently extremely low. Normally, the number is close to "1.00" for a balanced market, but a lower number means investors are overinvested in call options. This is an extremely bullish reading and if the market turns lower investors will need to unwind these long calls to avoid loses.

The current American Association of Individual Investor Survey (AAII) survey bullish percentage dropped significantly from a week ago as retail traders got cautious with stocks trading in a tight range. Befitting its contrarian nature, as soon as individual investors retrenched, the market shot up higher to end the week. The bullish reading is still relatively high and considered an indication of a looming price pullback.

Third-quarter National Association of Active Investment Managers (NAAIM) exposure index averaged 71.09. Last week the NAAIM exposure index was 85.43%, and the current week's exposure is 72.06%. Money managers reduced their equity exposure from extremely high levels a few weeks ago. This supports the view that the stock market should finish the year strong because investors are sitting on sufficient cash to reposition assets and chase prices higher.

Trading Strategy

All 10 sectors in the S&P 500 index rose last week with materials stocks' climbing the most, that sector is up 9 percent this year. Energy stocks were among the big gainers, getting a boost from a rebound in oil prices. Some traders anticipated that OPEC will decide to cut production at a conference next week. Last week we said "...The biggest change from recent weeks is the plunge in the Utilities sector which had been leading the market. This suggests that traders are looking to accept riskier assets at the expense of dumping risk adverse assets like Utility stocks..." for a standard strategy to construct an investment portfolio, the best technique to provide diversity is to invest in top performing stocks from each of the leading sectors. Selling shares in lagging sectors like Energy and Financials to invest in leaders such Industrials and Technology is a smart move that offers a high probability of success.

Regards,