Swiss Economy Winners and Losers

In reference to Rabbit Hole Intervention Fails: Wild Moves in Swiss Franc as Switzerland Abandons Euro Peg; Morals of the Story, reader "Grandaddy" a Swiss citizen living in the US, asks "How will removal of the peg affect the Swiss economy/outlook in the long run?"

Intuitively Obvious

It's an interesting question because what seems intuitively obvious at first glance is not necessarily correct over the long haul or even the short haul.

For example, conventional wisdom is that Swiss exporters will be crucified and importers will benefit. Certainly there is an initial shock. But long-term, look at it this way: The price of materials used in exports (metals in watches and Swiss-made machinery) will get cheaper.

This may balance out over time, or not. One would have to look at input and output prices for every company to see.

Right now, Luxury Watch Makers Bemoan Move. Nonetheless, I have to wonder: Are top-end luxury items so ridiculously overpriced and so dependent on price-insensitive status buyers that the price change will not matter that much?

One widely recognized "big loser" is the tourism industry. For sure, hotel prices in Switzerland rose as much as 40% overnight compared to prices elsewhere.

But Swiss grocery shoppers buying food imports from France, Spain, and the rest of Europe benefit mightily.

Which of those is more important? I suggest the benefit to Swiss shoppers is more important, at least in the grand scheme of things. Moreover, those consumers will have more money to spend on other things ... like restaurants, travel and hotels.

Net-net this is likely to be a loser for the tourism industry, but it may not be the total carnage most expect.

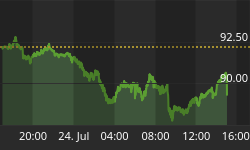

The big short-term loser was the financial industry. You can easily see that in the reaction of the Swiss Stock Exchange.

SMI Swiss Market Index

In two days the Swiss stock market plunged 1375 points, from a high of 9274 to a close of 7899, a decline of nearly 15%.

Pressure Cookers and Central Bank Sponsored Stability

In a matter of minutes the Swiss franc plunged as much as 40%. Such is the nature of foolish attempts by central bankers to control volatility.

Brokerage Firm Gets Rescue

By attempting to keep things stable, the central bank created huge winners and losers on financial speculation.

For example, broker FXCM required a $300 million bailout to stay afloat.

In the quote of the day (going back to December), Drew Niv, FXCM's chief executive officer said "Without leverage no one would trade." Niv argued in favor of 50-1 leverage over proposed 10-1 leverage.

Niv got his way, and needed a huge bailout.

For details, please see Quote of the Day: "Currencies Don't Move Much. Without Leverage, No One Would Trade"

It Only Takes One

Also consider the biggest known loser to-date. Hedge fund manager Marko Dimitrijevic and his $830 million Everest Capital's Global Fund that lost everything overnight.

For details, please see It Only Takes One: Hedge Fund Manager Who Survived Five Debt Crises Wiped Out Overnight on Swiss Franc

Repercussions

This Swiss Franc peg story goes far beyond speculation on the Swiss franc. How many hundreds of billions of euros were bet on individual stocks? And what about interest rate bets?

Like the Swiss franc, volatility on interest rates was also amazingly low. But yields plunged across the board, and so did potential wins and losses.

Currency-Wise Who Won?

It's widely believes that for every loser on financial speculation there is a corresponding winner. Under this theory, it's a zero-sum game, with market-makers taking a slice out of every transaction.

Certainly, there were record net short bets on the Swiss franc by speculators. And market makers have to take the other side of client bets. It's what they do. For every long contract, there is an offsetting short contract. So presumably the market makers were the winners.

Not so fast. Market makers hedge (at least they are supposed to). If the market makers had perfect hedges or nearly so, they broke even and all the winners (and losers) were on the speculative side of the trade.

Thus, it is not necessarily true that anyone had to win!

But perfect hedging is impossible.

Depending on imprecise hedges, not only on the franc, but also on related interest rate bets and derivative bets on Swiss equities, there is ample room for market maker wins and losses on moves of this magnitude.

I suspect the reported losses by Citigroup etc., were combined losses on all of the above. Perhaps some market makers lost more on equities and interest rates bets than they made being forced-long on Swiss franc futures.

Comparison to Gold and Silver

The above is essentially the same setup as with gold and silver futures. How many times did we hear "If silver rises to $10, then $15, then $20, then $30, then $35 ... it will blow the commercial shorts of of the water".

It never happened and I maintain it never would, because the market makers were hedged.

But hedging does not imply no market manipulation, and on that score, I believe there was manipulation (in both directions, up and down).

Swiss Franc Winners

Even though there were net record shorts in Swiss francs, some individual speculators were long. Since no one has stepped forward, they were likely small individual speculators or small hedge funds with relatively small positions.

Unless and until a big player steps forward, that is the most likely outcome.

Lawyers Win

On the non-financial side, here is a clear cut winner: Lawyers. Lawsuits of all kinds will likely fly in the wake of this fiasco.

The 90% Lost

More broadly speaking (in reference to central bank tactics in general), the 90% lost. Central bank induced volatility, inflation policies, and interest rate manipulations benefits those with first access to money: the banks, the political class, and the already wealthy. Everyone else loses.