The following is part of Pivotal Events that was published for our subscribers February 5, 2015.

Signs of The Times

"If we haven't achieved what we want to achieve, then we will have to do more."

- Italian Central Bank Governor, Bloomberg, January 23.

"The loans were for used [cars], many with tens of thousands of miles on their odometers, some more than a decade old. They were also one of the hottest investments around. So many asset managers clamored for [the bonds]...that the offering was increased 35%."

"Across the country, there is a booming business in lending to the poor."

- The New York Times, January 27.

"Chinese banks seeking to profit from the country's stock market frenzy have bought into the recent surge in margin finance, roiling regulatory efforts to reduce debt-fueled speculation."

- Reuters, January 29.

Perspective

The first quote from the Bank of Italy reminds that one of the most magnificent defaults in history was that of LTCM in 1998. The extremely-leveraged hedge fund was so highly regarded that some senior central banks loaned directly to LTCM. The Bank of Italy was the only one to take an equity position.

Now the BoI is out to inflate the world.

Private Chinese lenders that are bypassing the Bank of China by funding margin accounts directly could be called "wildcat" bankers. It is not the first example. As credit naturally tightened up in the fateful spring of 1929, the Fed wanted to look in charge. Fed Chair Roy Young issued some warnings about excessive speculation. Then markets came under some pressure and Charles Mitchell, president of the National City Bank, defied the policy and poured money into the call market. Mitchell was also a director of the New York Federal Reserve Bank and a fully committed bull. He stated that his bank had "an obligation which is paramount to any Federal Reserve warning."

Known as "Sunshine Charley", Mitchell suffered a major setback as the Roaring Twenties ended. National City is now known as Citigroup.

On the other hand, Albert Wiggin, as president of Chase National Bank, personally shorted his own stock - in a timely manner. During the mania and bust, Chase's economist Benjamin Anderson had a very good handle on inflation in financial assets.

Caught up in the confidence that goes with a perpetual boom, all classes of banks from central to commercial to investment have become overly ambitious. As with the workings of the US administration, checks and balances are not tolerated.

Stock Markets

It is uncertain if the confidence of central bankers is sublime or brazen. Perhaps some are just plain confident that their theories and practices will prevail over any risk. Others, perhaps aware of mounting risk, are belligerent in imposing remedies. As quoted above, the head of the Bank of Italy has joined Draghi.

Notwithstanding all of the debate at high levels about what central bank should do what, the financial markets are actually sorting it all out. For the stock market it has been sentiment and momentum numbers seen only at cyclical peaks. These have been registering since June and the NYA represents the broad US market.

The action is building a Rounding Top with key highs at 11105 in June, 11108 in September and 11068 in late November. The 40-Week ma provided frequent support on the way up to the Top in 2007 when late in that fateful year it was taken out. The same moving average provided similar support on this cyclical bull market. For the last few weeks this has been providing resistance.

It seems to be running a month or so behind the similar pattern in 2007.

Another guide in 2007 was the cyclical reversal in credit spreads that began in June. When credit markets are excited the seasonal turn in mid-year can reveal vulnerable positions. This was the case last June and while the trend is concerning it is not severe. It seems to be a month or so behind 2007.

So far, flattening of the yield curve has been constructive. Often booms have run some 12 to 16 months against flattening and when the curve reverses it signals the start of the contraction.

This is Month 13.

Sector Opportunity:

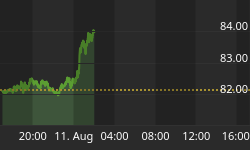

The bull market in REITS has been impressive with the index (IYR) rallying from very depressed at 59 in 2013 to 83 at the end of January.

The last outstanding rally reached a Weekly RSI of 81 in May 2013 at an index high of 71. It fell to 57 in that October.

On the big cyclical high the RSI reached 78.65 on February 15, 2007. The index crashed from 67 to 16.

This year's rally drove the Weekly RSI to 83.19 on January 26th. The index reached 83.54 and dropped to 79.56 at the first of the month. The rebound has made it to 82.23 earlier today. Taking out 80 would break an outstanding speculative thrust. Taking out 76 would likely push REITS into another bear.

The action in REITS has become vulnerable and the IYR trades rather well off of Weekly overbought signals.

Credit Markets

The "pause" in crude's slump has prompted a rally in Junk. JNK's plunge to 37.26 in December was sharp enough to register a Springboard Buy and the rebound made it to 39.17. The next decline was to 38.19 and now it is at 39.15. This is somewhat above the 50-Day ma, which is constructive.

However, the decline has been the most significant since 2008 and. merits close watching.

Credit spreads (chart follows) widened into a mini-panic in December, corrected and have resumed the trend. Quite likely, this has been a cyclical trend and the recent pattern seems similar to September 2007.

Long-dated Treasuries have accomplished an outstanding rally, which for the past month we have been describing as "ending action". That "Special" was sent out on January 20th.

The ChartWorks reviewed the action on February 2nd and on the 3rd. These reviewed the excesses and the one on Wednesday provided an initial target at the 143 level. The high was 151.80.

We had the "buy" in January last year. We are on the "Sell", which means getting defensive. We have been out of lower-grade bonds since June, and investors in this sector were advised to position 3 to 4-year US high-grade corporates, essentially for the currency play.

Commodities

Using a couple of determinants, January was likely to record the end of the initial plunge in crude oil prices. A "pause" has been possible and this has involved some impressive swings. Previous crashes in crude ran for some 6 to 7 months and that counted out to January. Previous crashes have taken a number of months to set an important bottom. A "V" bottom seems unlikely.

Although crude's swings have been wild, it should net out to a sideways trend before starting an intermediate rally.

As this works out other commodities would firm up.

Currencies

It was last May (How the time does fly!) when we noted that the rally in the DX could go from overbought to super-overbought. The latter could have been reached a few weeks ago when a more recent target of 92 to 94 had been exceeded.

Last week we noted that the Weekly RSI has reached 84 and was overbought. A period of correction for the DX is possible.

Today's ChartWorks noted that the plunge in the Canadian dollar is severe enough to register Downside Capitulations. That's on the Daily, Weekly and Monthly readings. A rare "Trifecta" of extreme action. An intermediate rally seems likely.

Precious Metals

The precious metals sector has built what appears to be a solid base. In November the HUI became the most oversold in a year. The action since has been constructive.

Our November 5th study on gold "Caveat Venditor" outlined the possible end to the bear market in precious metal stocks. Essentially, this was based upon gold's real price, which had been increasing since its cyclical low in June. The real price continues its advance and it will soon prompt a bull market for gold miners.

The bottom for the sector was dependent upon gold stocks beginning to outperform the bullion price and silver beginning to outperform gold. Both continue favourable.

The advice on November 5th was to begin to accumulate gold and silver stocks on weakness as equities would likely outperform the prices of silver and gold.

Representing real gold stocks, the HUI set its low at 146 in early November and tested it at 150 in the middle of December. The break above the 50-Day ma occurred in early January and the rally made it to 211, which was right at the 200-Day ma. That was a couple of weeks ago and the 200-Day has constrained the advance.

A correction down to the 50-Day at 180 could offer another buying opportunity.' Gold's real price is in a cyclical bull market and the stocks should soon set a technical bull market.

Credit Spreads

- Spreads narrowed into June which was seasonally ideal for a significant reversal.

- The widening trend is well established, which we take as a cyclical trend.

- The sharp spike to the middle of December was impressive and the correction was modest.

- Recent trading swings seem similar to September 2007.

Link to February 6 Bob Hoye interview on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2015/02/canadian-dollar-relief-rally