The major indexes suffered a third consecutive week of declines, as investors reacted to a steep drop in oil prices and a jump in the value of the dollar. The Dow lost 107.47 points, or 0.6 percent this week and the S&P 500 index ended down 17.86 points, or 0.9 percent. The Nasdaq was the biggest weekly loser among the major equity indexes losing 55.61 points, or 1.1 percent. The sell-off came at the end of a volatile week and sets the stage for a Federal Reserve policy meeting next week. Investors will be watching closely for clues about the central bank's views on the economy and interest rates. "This week has really been about investors' outlooks adjusting in the face of higher interest rates later this year," said Gabriela Santos, a global market strategist at JPMorgan Funds.

The Dow is down 73.76 points, or 0.4 percent year-to-date with the S&P 500 index is down 5.50 points, or 0.3 percent. The Nasdaq is still positive for the year up 135.70 points, or 2.9 percent. Smaller equity indexes like the Midcap and Russell 2000 are also positive for the year. After an outstanding performance for most of the year the bottom fell out of gold stocks and these shares are the biggest loser.

Right now all eyes should be on the Russell 2000 index. In the chart below you can see how the Russell 2000 has diverged higher from the other major equity indexes. If the Russell 2000 breaks down and follows the other indexes lower that is a strong negative for near term market direction. We want to see the other indexes catch up to the Russell to signal investors are buying the current dip.

A tool to help confirm the overall market trend is the Bullish Percent Index (BPI). The Bullish Index is a popular market "breadth" indicator used to gauge the internal strength/weakness of the market. It is the number of stocks in an index (or sector) that have point & figure buy signals relative to the total number of stocks that comprise the index (or sector). So essentially it is the percentage of stocks that have buy signals. Like many of the market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. If the market is strong and moving up, the BPI should also be moving higher as more and more stocks are purchased.

Last week's commentary concluded "... most of the major indexes have converted into range-bound trading. The relatively tight range suggests that very soon, prices will break out either higher or lower...contained in a tight trading range. The near term probability is that the price breakout will be to the downside..." As we surmised, the current S&P 500 Bullish Percent Index is in a confirmed downtrend. Most likely, investors' reaction to next week's Federal Reserve Open Market Committee meeting will determine whether the downtrend line is broken.

The U.S. dollar continued its advance against other major currencies. The U.S. dollar index, which measures the dollar against a group of other currencies, is up 6.4 percent over the past month. The dollar's advance can be tied to two factors, strategists say. The U.S. economy is getting better, as seen by the strong jobs report last week, and the Federal Reserve is poised to raise interest rates sooner rather than later. In comparison, the European Central Bank is trying to drive down interest rates by buying government bonds, a tactic the Fed used until last fall. The ECB's program has been driving down the value of the euro. For the entire month the dollar has gone parabolic and is putting unrelenting downward pressure on commodities. In particular the bottom has fallen out of precious metals such as gold.

Market Outlook

The stock market was hit hard with a third straight week of losses as investors reacted to a steep drop in oil prices and a jump in the value of the dollar. Utilities, companies that make basic materials like steel and major exporters had the biggest declines. The drop-off came at the end of a volatile week and sets the stage for a Federal Reserve policy meeting next week. Investors will be watching closely for clues about the central bank's views on the economy and interest rates.

Volatility may increase at the end of the week due to quadruple witching day, which is the expiration date of various stock index futures, stock index options, stock options and single stock futures. All stock options contracts expire on the third Friday of each month and once every quarter - on the third Friday of March, June, September and December - all four asset classes expire on the same day. Because futures and options investors must close out of their positions on those days, they often witness increased trading volume. The term "witching" comes from the fact that in the past, the expiration of futures and options contracts occurred not only on the same day, but also at the same time. This often resulted in a period of greater-than-normal market volatility, which became known as the "witching hour." Due to this increased volatility and frenzied market activity, many investors approach the markets differently on witching days.

So far in the first quarter of the year, investors have developed an appetite for riskier stocks. As evidenced in the graph below, Russell 2000, Nasdaq and MidCap 400 are far and away the leading indexes for the quarter. Market pundits are debating how soon the U.S. Federal Reserve will start raising interest rates; rate sensitive asset classes are going underwater.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend.

Recent Momentum Factor ETF (MTUM) chart analysis said "...stocks are displaying a topping action that precedes the next move higher or lower...noted is declining momentum which supports the contention an upward price move is stalling out...The current downtrend is strong and we need to look for signs the selloff is dissipating..." We got what we were looking for as the downtrend is slowing down. Now the question is, is this just a pause before stocks head lower or will prices bounce higher?

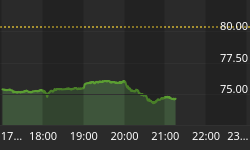

The updated chart below shows the how the S&P 500 index briefly dipped below the Volatility Index last week. After the dip below the VIX the S&P bounced up and was heading back down at weeks end. Expect continued fluctuation between the S&P and VIX as traders move the market thru daily triple digit up and price moves.

Recent analysis is confirmed when we said, "...The current Put/Call Ratio has an exceptionally high number of puts as traders purchased downside protection during last week's market pullback. This ratio is overly bearish and suggests the current stock downturn might be due for a pause..." You can see how the current total put/call ratio has basically equalized and indicates traders are no longer overly bearish. This backs our contention of near-term range-bound trading.

Last week's analysis proved to be on point as we stated "...The higher than normal neutral percent supports our analysis indicating near-term range-bound trading..." The current American Association of Individual Investor (AAII) Sentiment Survey result is disproportionately neutral at the expense of the bullish number that has been shrinking the past four weeks. The current survey results support the current range-bound trading with daily triple-digit price moves.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by association members. The green line shows the close of the S&P 500 Total Return Index on the survey date. The purple line depicts a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. Fourth-quarter NAAIM exposure index averaged 67.77%. Last week the NAAIM exposure index was 92.15%, and the current week's exposure is 65.68%. Institutional Investors current exposure is the lowest level of the year. Investors are getting nervous about economic uncertainty and responded by pulling money out of the market and sitting on cash until after the dust settles.

Trading Strategy

The graphic below confirms the fact that money managers have been dumping stocks in droves the past week. Healthcare is the only S&P sector that is above water over the past month. After a short countertrend bounce energy stocks got pounded back down to remain the worst performing group. Stocks that pay higher dividends, such as utilities, also had big losses. Be very careful with trading next week and it is prudent to enforce tight stops on open positions. Don't be surprised if volatility soars higher next week as a reaction to the Federal Reserve meeting and announcement, plus there is quadruple witching at week's end.

Feel free to contact me with questions,