The prices of the monetary metals cascaded downward this week, and the ratio of the gold price to the silver price rose accordingly.

Many analysts and speculators are puzzled. With everything going on in the world, gold should go up. After all, China released its new gold holdings and the banking system in parts of the world (e.g. Greece) is a mess, and many central banks are printing money, etc.

We don't know if China's published number (1658 tonnes, up from 1054 in April 2009) is true or not. We don't care to speculate, as some have, about this topic (though since we're linking the article, we want to point out that the Chinese economy is not bigger than the US economy, unless one adjusts the measurement).

We do know that credit stresses are mounting, and it's not just Greece. There are signs of problems all over the world, including in China. It is important to keep in mind how credit stress works. Let's compare and contrast two players, we'll call them Beavis and Butthead.

Beavis owns gold. He is not happy about the falling price. However, being unleveraged, he can think about it at his leisure. He may decide to sell or to keep it, but the point is that his hand is not forced and he is under no pressure. Many readers of this Report may be in this position (we hope).

Butthead has borrowed to buy assets, including gold. With each drop in price, the pressure mounts. He has to look at his leverage ratio -- and so does his bank. If he gets a margin call, then his consideration occurs under circumstances that are anything but leisure. Of all his assets, he may choose to dump gold because its price is dropping. This is appropriate for two reasons. One, he hopes to cut losses and hold winners such as stocks. Two, his leverage may be tied to gold specifically, and not to his whole portfolio.

In any case, it leads to the situation we have now. Even gold's biggest fans -- those who expect the biggest profits from a rising gold price -- are puzzled. At best. And of course many turn to conspiracy theories about who is whacking gold, and what the motive may be (regardless, we have repeatedly documented that the alleged gold whacking cabal does not have the means).

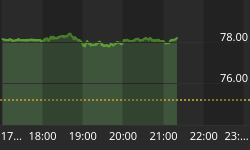

So here we are. Gold closed the week, broken down, below $1140. Silver is well under $15.

Our view is that breakouts and breakdowns cannot be determined from price charts. We want to know the fundamentals of supply and demand. If the price drops based on heavy selling of metal -- as has happened in silver since we began publicly documenting it 2013 -- then that's a fundamental move. We do not predict that fundamental moves should just causelessly reverse themselves, for the price to recover its previous high.

On the other hand, if the price drops based on selling of futures by leveraged speculators, that's a different story. Then we expect the price is likely to rise. This is because buyers of metal were already hungry at the higher price, and are incentivized even more at the lower price.

How do we measure this balance, this dynamic of changing equilibria in the futures and metal markets? Based on our theory of carry and decarry arbitrage, and using our proprietary model, we analyze the spreads between the spot and futures markets. This is the basis (pun intended) of our Supply and Demand Report.

Read on, for the only accurate picture of the supply and demand conditions in the gold and silver markets, based on the basis and cobasis.

First, here is the graph of the metals' prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can't tell them whether the globe, on net, is hoarding or dishoarding.

One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production (stocks to flows) can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential demand. At the right price, and under the right conditions. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals. For an introduction and guide to our concepts and theory, click here.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio moved up 2.2% this week.

The Ratio of the Gold Price to the Silver Price

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

The fact is that the price of gold dropped another $29 (i.e. the price of the dollar went up to another 0.67mg gold). The question is: why?

This graph shows a glaring picture of the action. Notice the red and green lines? Red is the cobasis (i.e. gold scarcity). Green is the price of the dollar (inverse to the conventional price of gold, measured in dollars). When the red and green lines move together like this, it means the price change is caused by speculators in the futures markets, who are repositioning. In this case, obviously, they're selling.

It is of note that the fundamental price of gold moved up $5 this week. It's now $65 over the market price.

Is this a good time to bet on gold? While other events could continue to dominate the fundamentals (temporarily), we can think of worse times for this trade.

Now let's look at silver.

The Silver Basis and Cobasis and the Dollar Price

The silver price dropped even more as a percentage, down -$0.71.

As with gold, look at the correlation of the scarcity measure and the dollar price. Silver, too, saw more selling of futures than of metal.

However, the silver cobasis didn't keep up with the gold cobasis. Our calculated fundamental price dropped from last week. It's still above the market price, but only 20 cents or so.

We don't normally comment on the market open, as we go to print Sunday evening (sometimes we wrap up this Report before the market opens). However, today it is noteworthy that the gold price has had a flash crash, hitting a spike low of $1073 (not a typo!) before settling at around $1106. The silver price did not flash crash, but it did drop, and now sits at $14.55.

There may be interesting buying opportunities coming up. Especially if you're not leveraged, not subject to margin calls, and have a longer time horizon than Butthead.