The entire gold-mining sector was crushed last month, suffering a full-blown panic. This was triggered by an extreme shorting attack on gold by American futures speculators. As fear-blinded traders rushed for the gold-stock exits, they claimed their selling was rational because gold miners' very existence was threatened by such low gold prices. But that's a total fallacy, this sector has no problem weathering sub-$1200 gold.

The recent pain in gold stocks has been excruciating. This sector's benchmark of choice these days is Van Eck Global's Market Vectors Gold Miners ETF, better known by its symbol GDX. It closely mirrors gold stocks' long-time leading sector index, the NYSE Arca Gold BUGS Index that trades as HUI. The carnage in these two gold-stock metrics has been incredible, shattering the resolve of most contrarian traders.

In just two weeks in mid-July, GDX plummeted 22.7% on an exquisitely-timed shorting attack on gold futures late one Sunday evening. A panic is formally defined as a 20%+ plunge in a major index in 2 weeks or less. Nearly half of GDX's panic losses hit that Monday morning immediately after that gold attack. That battered GDX to a new all-time low, the worst levels seen since it was born in May 2006!

Gold-stock investors and speculators were so terrified that they kept on selling, forcing GDX another 5.0% lower on close by early August. While such horrendous levels had never before been witnessed in the relatively-young GDX gold-stock ETF, they had been in the venerable HUI. Gold stocks were last trading at these recent lows 13.0 years earlier in July 2002, when gold was still meandering near $305!

Having deeply studied and extensively traded gold stocks over the past 15 years, I argued in late July that those panic gold-stock levels were fundamentally absurd. There was simply no way to justify gold-stock price levels being so darned low given the far-higher prevailing gold prices. In an essay I showed that gold stocks had never been cheaper relative to gold, the metal that drives their profits and ultimately stock prices.

These recent epically-extreme gold-stock lows certainly weren't righteous fundamentally, they were the product of wild fear run amuck. Yet as always in a panic-selling situation, the investors and speculators who succumbed to their own emotions to flee at extreme lows didn't want to hear the truth. Right after deluding themselves into selling at the worst possible time, they're convinced their decision was rational.

These traders had sold gold stocks as if gold was trading at just over a quarter of its recent lows, which was the height of folly. They sure didn't like me pointing that out several weeks ago, and unleashed a blizzard of angry feedback. That's par for the course at extremes when you're a rare contrarian fighting the groupthink herd. After writing 665 of these weekly essays over 15+ years, I really know how traders think.

Their main argument on gold stocks' panic-grade selloff being rational surrounded the costs of mining gold. There's a universal belief out there that the gold-mining industry isn't profitable under $1200 gold. I have no idea who started this, but I come across it constantly. And if $1200 is indeed the breakeven point, then $1100 or sub-$1000 gold would surely lead to widespread bankruptcies and a gold-stock apocalypse.

After 15 years of researching this sector more deeply than almost anyone else on the planet, I certainly didn't believe that $1200-per-ounce industry cost level was correct. But I couldn't prove it right away, as the gold miners hadn't released their second-quarter operating and financial results yet. But since the great majority finally reported Q2'15 in the last couple weeks, now we can dispel that $1200-cost fallacy.

Since these prevailing gold-stock prices are so ludicrously undervalued, we've aggressively redeployed capital into this sector in recent weeks. We've bought and recommended to our newsletter subscribers a bunch of elite gold miners with very low production costs than can survive gold prices far under recent lows. I could easily cherry-pick these elites to show gold mining remains very profitable at today's gold levels.

But a far-superior read on this industry's current cost structure comes from this sector as a whole. That flagship GDX gold-stock ETF currently holds 39 major miners. This week I waded through the latest quarterly results of all of them. Collectively GDX's component stocks account for the vast majority of the world's gold mining, so they effectively are the gold-mining industry. And their costs are far lower than thought.

I built a couple tables that could fit in the top 34 of GDX's 39 components. Collectively they account for a whopping 97% of this entire leading gold-stock ETF, essentially all of it. To get an idea about the survivability of this sector, I looked at each miner's cost structure, cash on hand, debt levels, cash flow generated from operations, debt payments, and more. The key results are summarized in these tables.

A couple notes before we shatter that myth that gold miners' very existence is threatened at prevailing gold prices. GDX holds a wide range of gold miners trading around the world. Since foreign markets have different financial-reporting standards than the United States, not all data was available for every company. When any miner didn't report a specific data point, I had no choice but to leave that field blank.

GDX also contains royalty and streaming companies, which have very different cost structures than the miners. They generally offer miners large up-front payments to help finance mine builds. And in return they're entitled to collect small recurring payments on these miners' production over the lives of their mines. They don't report costs the same way producers do. This gold-stock ETF also oddly contains silver miners!

But here are the latest quarterly results of the leading companies in the gold-mining industry. Each stock's symbol and exchange is noted, along with its weighting in GDX and its market capitalization. Then the particular 2015 quarter the data is taken from is noted, followed by miners' costs per ounce produced. These include cash costs and all-in sustaining costs for that quarter, and full-year 2015 AISC guidance.

Gold miners' cost structures greatly affect their cash positions and cash flow, which are obviously critical for their survivability. Here each miner's cash in the bank at quarter-end is listed, with the percentage of their current market capitalizations that represents. That is followed by the cash flows generated from operations. Companies with strong positive cash flows have virtually zero risk of facing bankruptcy.

Finally, each miner's quarterly production is noted. My spreadsheet to evaluate this sector had many more columns with other metrics, but these are the key ones that fit in these tables. Taken as a whole, the gold-mining industry is much stronger financially than virtually everyone believes today! This is super-bullish for gold stocks given the choking cloud of extreme fear that is still suffocating this sector.

Since the 1990s, cash costs have been the dominant measure of gold-mining cost structure. That is what it actually costs to mine each ounce of gold. Cash costs include direct production costs, onsite administration, regulatory, royalty, and tax expenses, along with smelting, refining, and transport costs. Cash costs are the acid-test measure of what it costs the gold miners to bring their product to market.

And cash costs remain far below current gold levels, averaging just $649 and $620 in Q2'15 for the actual gold miners among GDX's top 17 and next 17 component companies! That's way lower than even today's dismal prevailing gold prices, which means the gold-mining industry will have no problem at all weathering $1100 or even $1000 gold. Their current mining operations could easily survive even at $800!

Now I certainly don't expect gold prices to slip under $1000, let alone plunge to $800. Gold's recent lows were totally artificial, the product of unsustainable extreme record gold-futures shorting. But since these low gold prices breed endless hyper-bearish commentary, realize that even if the bears miraculously prove right the gold-mining industry is not at risk. Today's mix of major gold miners could keep right on producing.

And the whole notion of sector-wide bankruptcy risk is silly given the way large gold miners operate. They run multiple gold mines, all with their own cost structures. So when times get tough, they can simply mothball the mines with cost levels too high for prevailing gold prices. And even within individual mines, they have a lot of leeway in choosing to mine higher-grade ore if necessary to lower per-ounce costs.

During this year's second quarter where gold prices averaged $1172 before gold was attacked by the futures short sellers in July, the gold miners' cash costs were much lower than widely assumed. In theory, gold miners can survive as long as the gold price exceeds their cash costs along with general corporate expenses. They are not included in cash costs like mine-level administrative expenses are.

But gold mines are depleting assets, with all deposits finite. So in order for gold miners to continue to be viable going-concern businesses, they need to constantly discover new gold to mine. This involves lots of exploration, which is very expensive. So back in June 2013, the World Gold Council introduced a new gold-mining cost measure known as all-in sustaining costs. They include far more than cash costs.

In addition to all the direct cash costs, all-in sustaining costs include all corporate-level administrative expenses along with all costs required to maintain and replenish existing production levels. The major items included are reclamation and remediation along with all the exploration, mine-development, and capital expenditures necessary to sustain current production levels. This is definitely a superior cost measure.

When gold-stock bears claim the gold-mining industry needs $1200 gold to survive, it's these all-in sustaining costs they are referring to. Yet in Q2'15, again before the recent shorting-fueled gold woes, industry-wide all-in sustaining costs per ounce were far below that $1200 threshold. GDX's top 17 component gold miners had average AISCs of $936, while the next 17 looked even better averaging $857.

So even $1000 gold, which again is super-unlikely as gold rebounds dramatically on massive futures short covering, isn't a problem at all for gold mining's survivability. While there are certainly higher-cost and lower-cost gold producers, as an industry current production levels are sustainable at well under $1000 per ounce. That's not a threat at all, despite being falsely implied as one in today's gold-stock prices.

And Q2 certainly wasn't an anomaly on the AISC front. Most gold miners provide AISC guidance for the entire year. And since gold-stock investors are so focused on costs these days with gold prices so low, the gold miners tend to be conservative in their AISC outlook to avoid disappointing. And the full-year-2015 AISC projections from these major gold miners are right in line with their actual second-quarter results!

The gold miners' current low cost structure relative to prevailing gold prices was reflected in their cash positions too. Most are sitting on cash hoards so large that they are equivalent to big fractions of these companies' total market capitalizations! That means they could actually afford to lose money from their operations for many quarters, although that certainly isn't in the cards anywhere above $950 gold levels.

Even better, these cash positions were growing fairly rapidly in the latest quarter due to high positive operating cash flows in this industry. When any business is generating large cash flows in its ongoing operations, it has virtually no risk of going bankrupt. And many of the elite GDX gold miners reported operating cash flows that were large relative to their current cash positions and even market capitalizations.

Positive cash flows from mining are exactly what you'd expect when prevailing gold prices are well above current costs. I didn't come across a single miner in these tables that was actually losing money in operations. Amazingly given the extreme bearishness on gold stocks out there, this industry is still strongly cash-flow-positive. Gold miners aren't just surviving under $1200 gold, they're actually thriving!

But unfortunately few investors and speculators realize this, for a couple key reasons. Since popular fear remains so extreme, traders are seeking out bearish analysis and commentary in order to rationalize their own pessimism. They don't want to admit they were fools to flee gold stocks near fundamentally-absurd 13-year lows reflecting gold prices around a quarter of today's levels! They want to think that was smart.

Popular bearishness is always most intense and extreme right near major secular lows, when traders are wrongly convinced an already-devastated market will keep spiraling lower indefinitely. And for the hardened contrarian traders who can overcome this groupthink orgy of gold-stocks-to-zero nonsense, they are often scared away by gold miners' accounting earnings. Many if not most are showing losses now.

But these nonexistent price-to-earnings ratios are very deceiving. As gold miners' Q2 results proved, they are generating large positive cash flows by mining gold today. The negative accounting earnings are not from operating losses, which would indeed threaten the viability of gold-mining companies. These losses are from huge write-offs of gold-mine and gold-deposit asset values sometime in the last four quarters.

Since gold in any particular deposit essentially has a fixed cost to mine, lower gold prices erode future potential profit margins of that deposit. Accounting rules force gold miners to write down the value of these properties even if the recent gold lows are temporary anomalies. These non-cash impairment charges can be very large, overwhelming normal operating profits until the write-downs roll off the books.

In any other sector in all the stock markets, such large one-off write-downs would be ignored by analysts since they don't reflect ongoing profitability. But since virtually no professional analysts follow this despised and forgotten sector, there is no analysis to separate ongoing operations from one-off events. So until four quarters after large write downs, they greatly skew P/E ratios and scare investors away.

But as long as the gold price recovers from its recent artificial extreme-shorting-spawned lows, which is already starting, write-offs are really irrelevant. Taking impairment charges not only has zero cash impact, but it certainly doesn't affect the gold contained in any deposit. That gold in the ground is all still there and waiting for higher gold prices, which will quickly restore its economic value and mineability.

The gold-mining industry's existence certainly isn't threatened with today's $1100 gold, let alone that false $1200 number always thrown around. The vast majority of the world's gold production today would be profitable on a sustaining basis at $1000, and could easily survive a temporary panic-grade plunge under $800. Thankfully the odds of that happening are virtually zero since gold traders already capitulated.

Gold is overdue to mean revert sharply higher as American speculators are forced to cover their extreme record gold-futures shorts, and the usual massive Asian seasonal buying ramps up. These higher gold prices will not only greatly boost gold miners' profitability, but more importantly traders' confidence in this left-for-dead sector. And as we've witnessed recently, that's going to lead to the gold stocks just soaring.

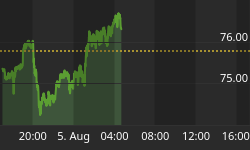

As of the middle of this week, GDX had rocketed 18.6% higher in just 5 trading days since its all-time record lows of early August! The notion that gold stocks priced as if gold was near $305 was righteous was ridiculous, and investors and speculators are finally starting to overcome their crippling fear and understand that. So they are returning to gold stocks, which will accelerate the rally and beget more buying.

The gold miners' latest quarterly results just reported in the last couple weeks decisively prove that this industry is far healthier than universally assumed. Production costs are still way below current gold price levels, in both cash-cost and the more-importantly all-in-sustaining-cost terms. This has left these miners with massive cash war chests and large positive operating cash flows, revealing surprising financial strength.

With the gold stocks still trading near all-time lows relative to the price of gold which drives their profits, there's never been a better time to throw heavily long this contrarian sector. GDX is a great ETF which offers exposure to the world's biggest and best gold miners. Nevertheless, the best opportunities in gold stocks are in the smaller miners. Many have lower costs and higher profits, leading to low actual P/Es today.

At Zeal we've been aggressively buying these elite smaller miners with potential gains running from 4x to over 10x as gold mean reverts higher. These new trades are detailed in our acclaimed weekly and monthly newsletters. They draw on our decades of exceptional market experience, knowledge, and wisdom to explain what's going on in the markets, why, and how to trade them with specific stocks. Since 2001, all 700 stock trades recommended in our newsletters have averaged annualized realized gains of +21.3%! Subscribe today before gold stocks soar, and take advantage of our 33%-off sale!

The bottom line is the gold-mining industry's cost structure is far lower than that $1200 number often thrown around. The world's biggest gold miners are producing gold on an all-in-sustaining basis for well under $1000 per ounce. And on a cash-cost basis, they could weather an $800-gold anomaly for many quarters. Gold miners' survivability is not in question at today's gold prices, they have zero bankruptcy risk.

Amazingly given the irrational bearishness cursing this sector today, most of the larger gold miners are sitting on massive piles of cash. And these are growing rapidly thanks to high positive operating cash flows. Soon this will be reflected in P/E ratios as the asset-impairment write-offs roll off of current-year earnings. Investors and speculators will suddenly realize just how epically cheap gold stocks are today.