Below is a summary of my post-CPI tweets. You can (and should!) follow me @inflation_guy or sign up for email updates to my occasional articles here. Investors with interests in this area be sure to stop by Enduring Investments. And sign up to receive notice when my book is published! The title of the book is What's Wrong with Money?: The Biggest Bubble of All - and How to Invest with it in Mind, and if you would like to be on the notification list to receive an email when the book is published, simply send an email to WWWM@enduringinvestments.com.

-

core CPI+0.13%, softer than expected. Core y/y rose from 1.77% to 1.80% due to soft year-ago comparison.

-

Next month we drop off an 0.05%, so we will almost surely get a core uptick. Surprising we haven't yet. Waiting for breakdn.

-

Both primary rents and owners' equiv accelerated slightly, Which means core EX HOUSING was actually slightly down m/m

-

core services rose to 2.6% (mostly on housing); core goods fell to -0.5% from -0.4% y/y. Same story overall.

-

Apparel accelerated to -1.64% from -1.85% y/y. Story for years in apparel was deflation; in 2011-12 prices rose>>

-

>>and looked like return to pre-90s rate of rise. Then it flattened off, and has been declining again.

-

Apparel could well be a dollar story now - it's almost all made overseas, almost no domestic competition so dollar matters.

-

our proxy for core commodities is apparel + cars + med care commodities. all 3 decelerated. Cars went from +0.5% to 0.0% y/y.

-

sorry, Apparel actually ACCELERATED to -1.6% from -1.9%, but still negative.

-

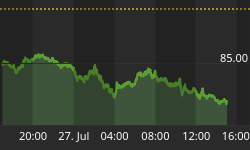

airfares not really a story. -5.6% y/y vs -5.2% y/y. The NSA number dropped but it always drops in late summer. [Ed note: see chart below]

-

airfares was -8.5%, but it was -8.1% last july, -2.9% in 2013, -2.6% in 2012...no story there. didn't affect core meaningfully.

-

Primary rents 3.56% from 3.53%. OEW 3.00% from 2.95%. Both will continue to rise.

-

Lodging away from home also rebounded to 2.9% y/y after a one-off plunge to 0.8% y/y last month. Household energy of course down.

-

Transportation accelerated (-6.6% y/y vs -6.9%) on small motor fuel recovery. btw, airline fares are only 0.7% of CPI, so 0.9% of core.

-

Med Care: goods were dn (drugs 3.2% vs 3.4%,equipment -0.9% vs 0.0%) but prof services up (2.1% vs 1.8%),hospital svcs dn (3.2% vs 3.5%)

-

Health insurance only +0.9% y/y vs 0.7%, but more expenditures out-of-pocket under the ACA so higher infl for those categories hurts.

-

Median (due out later) might only be +0.1% this month. I have it cuffed at 0.15% but I don't seasonally-adjust the housing sub-components.

-

Last yr Median was +0.17% m/m, so best guess is it roughly holds steady at 2.3%.

-

I don't see how the Fed embarks on a meaningful tightening in Sep, with global economy weaker than it has been in a couple yrs.

-

Median inflation and growth plenty strong enough to "normalize" rates but that's not a new story.

-

I've been saying they should tighten for a few years but not sure why they would NOW if they didn't in 2011.

-

But Fed doesn't use common sense or monetarist models.It's all DSGE;who knows what those models are saying?Depends how they calibrated.

-

FWIW our OER models diverge here. Our nominal model says pressures on core start to ebb in a few mo; our real model predicts more rise.

-

I like the real model as it makes mose sense...but it's not tested in a real upswing.

-

US #Inflation mkt pricing: 2015 0.8%;2016 0.7%;then 1.6%, 1.7%, 1.8%, 1.9%, 2.0%, 2.1%, 2.2%, 2.3%, & 2025:2.2%.

-

...so inflation market doesn't see inflation at the Fed's target (about 2.2% on CPI vs 2.0% on PCE) until 2023.

-

The market is not CORRECT about that, but another reason the Fed can defer tightening if they want to. And they have always wanted to.

First, let's start with the airfares chart. One of the early headlines was that airfares plunged by the most since some long-ago year, which held down core. Well, here is the chart of airfares, non-seasonally adjusted. You tell me whether this is unusual to have airfares fall in July.

Because this is part of a normal seasonal pattern, the year-on-year figure was only slightly lower, as I note above. And airfares are a tiny part of CPI, less than 1% of the core. This is not a story.

More important will be the median CPI. This is a much better measure of the central tendency of prices than headline or core, both of which (as averages) can be skewed by a few categories having outsized moves. Median inflation has been ticking higher (see chart below) but will probably go sideways this month.

Finally, the most important chart. There are lots of ways to model housing. If you model rents as lagged versions of the FHFA Home Price Index, or Existing Home Sales median prices, then you get one model and that model suggests that rents should begin to moderate over the next 6-12 months. Not that they will decelerate markedly, but that they will stop accelerating and therefore stop being the driving force pushing core CPI higher. But if you use those models, you have to recognize that you are calibrating over a period of very slow inflation, so that you are effectively ignoring the knock-on effect of higher inflation on rents. That is, if core inflation is around 2% and rents are 3%, then if core inflation rises to 5% you wouldn't expect rents to be at 3%. So, you need to use a model that recognizes the interrelationship between these variables. And that sort of model implies that rents will continue to climb. Both models of Owners' Equivalent Rent are shown in the chart below. I prefer the "real" model to the "nom" model, but we don't know the right answer yet.

Even if OER moderates it doesn't mean that CPI will stop rising; it just means that the story will stop being all about rents. Core goods still have a long ways to go to normalize, and that might be the next story. But for now, I am still focused on rents.

As I said, I really don't see how the Fed can think about hiking rates in September based on the data we have seen recently. Yes, inflation is on the border of being an issue, but that has been true for a long time. In 2011, there was plenty of growth and while high rates would not have been warranted, it is hard to argue that normal rates were not called for. And yet, we got QE and more QE. This will end up being the biggest central bank error in decades, regardless of what the Fed does in September. I doubt they will hike, and if they do then it won't be a long series of hikes. This is still a very dovish central bank, and they will get skittish very quickly if markets balk at more expensive money - which, of course, they are wont to do.

Note: If you would like to be on the notification list for my new book, What's Wrong with Money?: The Biggest Bubble of All - and How to Invest with it in Mind to receive an email when the book is published, simply send an email to WWWM@enduringinvestments.com and I will put you on the list!

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"