Gold has enjoyed a strong new uptrend in recent months following last summer's extreme gold-futures shorting attack. But speculators returned with a vengeance this past week, aggressively dumping gold futures again following a hawkish surprise by the Fed. The resulting gold plunge shattered its support, and thrust sentiment back into hyper-bearish territory. But gold-futures shorting soon reverses to big buying.

In recent years the gold-futures trading by American speculators has utterly dominated the gold price. With investors still missing in action thanks to the Fed's astounding stock-market levitation, speculators' reign is unchallenged. Gold is not only at the mercy of their mercurial sentiment, the leveraged nature of futures speculation grants their collective trades an outsized impact on gold's price. They rule the roost today.

With global stock markets levitating due to extreme central-bank money printing and jawboning, normal investment demand for gold has relentlessly withered away. With endless easy money buoying stocks ever higher, gold's traditional role as a critical portfolio diversifier that moves counter to stocks just isn't valued today. This has led to radical gold underinvestment, creating a demand vacuum for speculators to fill.

And thanks to futures' inherent extreme leverage, speculators' firepower to move gold prices is nothing short of immense. When an investor buys 100 ounces of physical gold, the equivalent to a single gold-futures contract, they have to pay $115k at $1150 gold. If they choose to gain gold exposure via the leading GLD gold ETF instead, they can run margin of up to 50%. That lowers their buy-in cost to $57.5k.

But futures speculators can effectively buy or sell gold in 100-ounce increments with far-higher leverage than stock traders. This week, the minimum maintenance margin on a gold-futures contract was just $3750. That's all it takes for speculators to control 100 ounces of gold worth $115k at $1150! This is incredible leverage of 30.7x, vastly greater than the 41-year-old legal limit in the stock markets of just 2.0x.

So each dollar of futures speculators' capital bet on gold is up to 30x more powerful in moving the gold price than a dollar of investors' capital. In normal times this excessive influence is offset by far more investment capital deployed in gold than speculation capital. But with central banks deluding traders into believing stock markets can magically rally forever, investors have abandoned gold to chase stocks.

Since early 2013 when the Fed's wildly-unprecedented open-ended third quantitative-easing campaign ramped up to full speed, American futures speculators' collective bets have effectively controlled the gold price. The only other major driver of gold during that surreal Fed-distorted span was the extreme liquidations in GLD's gold-bullion holdings on epic differential selling as stock investors abandoned gold.

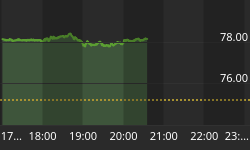

All of 2015, including this past week's Fed-spawned gold plunge, has proven a microcosm of recent years' utter gold dominance by American futures speculators. This first chart shows their ironclad gold-price influence through the weekly Commitments of Traders reports that reveal their collective bets on the gold price. Long-side bets on gold rising are shown in green, while short-side ones on it falling are red.

When American speculators buy gold futures, gold rallies. When they sell, gold sells off. This is rather unfortunately the whole story of gold this year, with investors not around to offset the hyper-leveraged gold-futures trading. It doesn't matter if speculators buy gold futures by adding new long contracts or covering existing short ones, nor does it matter if they sell by closing existing longs or adding new shorts.

Gold certainly got off to a promising start this year with a sharp rally in January that catapulted it above $1300. That was directly driven by speculators buying new long contracts to ride gold's rally while also covering shorts to get out of the way. Speculators' total long-side gold-futures bets just soared back then, while their short-side bets collapsed. But soon after gold peaked, speculators reversed their trades.

Gold plunged in February and early March because futures speculators were liquidating longs while ramping shorts. The positive correlation between the blue gold-price line and the green spec-total-longs line is very high, while the inverse correlation between gold and the red spec-total-shorts line is even higher. When speculators are aggressively buying or selling gold futures, they utterly dominate the gold price.

As soon as speculators stopped dumping gold futures in March, gold stabilized and ground sideways along with specs' collective bets. Gold didn't fall out of that multi-month consolidation trading range until early July as speculators again started heavily shorting gold. That culminated in a record extreme gold-futures shorting attack, when a manipulative massive single short-sell order targeted gold on a Sunday night.

But the great thing about speculators' gold-futures shorting is it's inherently self-limiting and guarantees big near-future buying. There are only so many traders willing to make such incredibly-risky downside bets on gold late in a major selloff. And once gold's downside momentum slows, stops, and looks to be ready to reverse, leveraged speculators have to be quick to exit by buying gold futures to close their short ones.

At 30.7x leverage, a mere 3.3% gold rally would wipe out 100% of the capital risked by speculators. And if gold climbed fast enough to make exiting difficult, they would face immediate margin calls that would force them to pony up more money or suffer forced liquidations. So even a modest gold rally unleashes self-feeding short covering. The more gold rallies the more speculators have to cover, amplifying gold's gains.

And that's exactly what happened following the all-time record highs of speculator gold-futures shorts back in early August. As speculators bought long gold-futures contracts to offset and close their shorts, the gold price surged dramatically. That massive short-covering spree ran until the latest CoT week that ended last Tuesday October 27th. That's the latest CoT data available when this essay was published.

Over 12 weeks ending that day, American speculators bought 102.7k contracts to cover shorts. This is an astounding amount of gold, equating to 319.4 metric tons. That works out to about 106.5t per month over that latest short-covering span. According to the newest fundamental supply-and-demand data from the World Gold Council, global investment demand averaged just 75.7t per month in the first half of 2015.

With futures speculators' short covering effectively catapulting gold investment demand 141% higher, it's no wonder gold surged 9.6% in just under 10 weeks even with investors largely not participating. This buying led gold to carve its recent strong new uptrend, with lows and highs marching up within the trend channel shown above. But then something very unexpected knocked the winds out of gold's sails.

On Wednesday October 28th, the latest monetary-policy decision from the Fed's Federal Open Market Committee was due out that afternoon. Everyone expected the uber-dovish Yellen Fed to stay on its robotic script of easy money forever, implying no imminent rate hikes to end the Fed's zero-interest-rate policy implemented 6.9 years earlier in December 2008. That terrible latest jobs report almost demanded dovishness.

Back on October 2nd, the official US report on September jobs was a colossal miss at 142k jobs actually created versus the +200k expected. Even worse, past-month revisions sliced away another 59k jobs. That left the actual jobs number way down near +83k, a total disaster. After the Fed spent years arguing it was dependent on data, traders knew there was no way the FOMC was going to hike rates right after that.

Thus market expectations for the first rate hike happening this year were very low heading into that key FOMC meeting, the second-to-last in 2015. A strong majority of traders were also convinced the Fed wouldn't hike at its next mid-December meeting either. Janet Yellen and her merry band of interest-rate manipulators weren't happy about their lack of credibility in saying otherwise, so they chose to shake things up.

The FOMC shocked the markets last Wednesday by changing a single sentence in its statement to read, "In determining whether it will be appropriate to raise the target range at its next meeting, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation." The italics are mine, futures speculators pounced on those 4 new words like lions on fresh meat!

They immediately started aggressively selling gold futures on their strongly-held belief that higher rates are very bearish for gold. Ahead of that FOMC meeting that morning, gold had been trading at $1182 which wasn't far from its best levels of October. But after the Yellen Fed defied belief to wrench traders' expectations back to a December rate hike being very possible, gold plunged to close 0.9% lower at $1156.

That futures selling momentum built on itself in the subsequent days, with gold falling another 1.0%, 0.3%, 0.7%, 1.4%, and 0.9% on the next 5 trading days. As of the middle of this week, gold has lost an incredible 5.1% in 6 trading days including that FOMC day. Futures speculators have once again gone on the attack to savage gold with aggressive gold-futures selling. This wreaked some real technical damage.

As the chart above shows, speculators' serious selling pummeled gold down through its new uptrend's lower support line. This big technical breakdown further exacerbated resurgent bearish sentiment. And with gold back down near $1100 after it had been closing in on $1200 just a couple weeks earlier, everyone is convinced today that gold is doomed to spiral lower indefinitely. But that's almost certainly not in the cards.

Speculators' total bets in gold futures are published once a week in those CoT reports. Though that data is current to Tuesdays, it isn't published until late Friday afternoons. So the reason a collapse in speculators' long gold-futures positions and surge in their short ones isn't evident is because the latest CoT report available when this essay was published was current to Tuesday October 27th. The day before the FOMC!

Given gold's rapid plunge, and futures speculators' utter dominance of its price in recent years, there is no doubt this Friday's CoT is going to show a sharp climb in spec shorts and likely a big drop in spec longs over the CoT week straddling that hawkish FOMC statement. I can't wait to see the mix of long liquidations and short covering, as their implications for gold's near-term price action vary considerably.

If most of this latest bout of spec selling was fueled by closing longs, gold's outlook isn't as bullish. No speculator is compelled to make new upside bets on gold, those trades are totally voluntary. And given the extreme leverage inherent in gold futures, speculators must have high levels of conviction on an imminent gold rally to add longs. But it's a whole different ballgame if short selling just hammered gold.

In order to short sell gold they don't own, speculators first have to borrow it in the form of gold futures. They immediately sell those contracts, and hope the gold price falls enough for them to buy back at a lower price so they can earn a profit before repaying their debts with cheaper gold. Because of that borrowing element, short covering is compulsory. Speculators are legally obligated to buy gold futures to close shorts.

So gold-futures shorts are guaranteed near-future buying, which is why I was so super-bullish on gold near its lows back in early August when everyone else was convinced its fall was just starting. The more speculators ramped their shorts in this past week on the hawkish FOMC, the more gold-futures buying will be necessary soon to offset and close those positions. High spec shorts are a very-bullish omen.

This next chart expands this same dataset to encompass the Fed's entire wildly-distorted era since early 2013. It reveals a well-defined horizontal trend of speculators' total gold-futures shorts. These leveraged downside bets have proven more influential on the gold price in recent years than the upside ones. So the higher in this trend channel spec shorts have gone, the greater the near-term potential for a major gold rally.

Spec gold-futures shorts have generally meandered between 75k-contract support on the low side to 150k-contract resistance on the high side. On the Tuesday right before that Wednesday FOMC meeting, the latest CoT report showed specs' total shorts at 99.7k contracts. That's definitely on the low side in the context of recent years. And this low level of spec shorts paved the way for that massive post-Fed selling.

If speculators had already been heavily short coming into the FOMC, they wouldn't have had the firepower to add significant new short positions. But since spec shorts were fairly low ahead of that, there was unfortunately lots of room to rebuild positions. It was only 12 CoT weeks ago in early August when total spec downside bets on gold hit an all-time record of 202.3k contracts. That was 103% above last week's levels.

So how big could this past week's shorting actually have been? Since early 2013, the CoT weeks that have seen speculators' downside gold-futures bets climb had average gains around 9.5k contracts. A big shorting week is 20k+ contracts, which have only been seen in 11 out of 147 CoT weeks in that span. I suspect we'll definitely see a 20k+ jump in short contracts this week given the size of this gold selloff.

That would catapult spec shorts back up near 120k contracts, which is well above their trend's midpoint of 112.5k. And gold is definitely bullish in the near term, usually soon embarking on a big surge driven by short covering, when these leveraged downside bets are in the top half of recent years' trading range. So odds are speculators' latest savage gold-futures shorting frenzy created plenty of short-covering rally fuel.

So what could possibly light a fire under bearish gold-futures speculators to cover their shorts again? A couple things. First, the reason investors abandoned gold in recent years was that Fed-conjured stock-market levitation. And after the stock markets rocketed higher in October in what looks just like a classic bear-market rally, they are ripe for another major selloff. As stocks retreat, gold will catch a bid like usual.

Second, futures speculators are so blinded by herd groupthink that they haven't yet realized that Fed-rate-hike cycles are actually bullish for gold! This sounds heretical, since the notion that higher yields kill zero-yielding gold appears logical. But history proves just the opposite, that gold investment demand and therefore prices surge when the Fed is hiking rates because it is so damaging to stock and bond prices.

The Fed's last rate-hike cycle ran between June 2004 and June 2006. During that span, the Fed hiked its benchmark federal-funds rate no fewer than 17 separate times for a total of 425 basis points. That more than quintupled the FFR. Yet what did gold do over that exact timeframe? It soared 49.6% higher! And that certainly wasn't an anomaly, big gold gains are actually the norm for past Fed-rate-hike cycles.

I recently finished a comprehensive study of gold's price behavior during every Fed-rate-hike cycle since 1971. It turns out there have been 11 of them, and in 6 of those gold rallied to an average gain of +61.0% during those exact rate-hike-cycle spans! Gold thrived in the very times that today's speculators mistakenly believe it should've been crushed. Whenever gold entered a new rate-hike cycle low, it dramatically rallied.

During the other 5 Fed-rate-hike cycles since 1971 where gold fell, its average loss was just 13.9%. And every single time gold entered those rate hikes near major secular highs. That's certainly not the case today, with gold down and out and despised. Sooner or later American futures speculators will learn that Fed rate hikes are vastly more dangerous for stocks and bonds then gold, attracting investors to the latter.

So the savage gold attack by futures speculators over this past week isn't sustainable for long. Extreme futures shorting soon burns itself out, and the more contracts shorted the greater the potential for a major rally erupting imminently on short covering. Gold's going to catch a bid as these lofty stock markets roll over again. And history proves Fed rate hikes are bullish for gold investment demand when gold starts near lows.

If this inevitable short covering comes soon enough, it will catapult gold back into its young new uptrend to keep it intact. Traders can play this coming short-covering surge in gold through the metal itself, the leading GLD SPDR Gold Shares gold ETF, or the beaten-down stocks of the elite gold miners. I certainly prefer the latter, since they have great potential to leverage the coming gains in gold many times over.

At Zeal we've long specialized in this contrarian realm, buying low when few others were willing to. And it proved very successful. Since 2001, all 700 stock trades recommended in our acclaimed weekly and monthly newsletters have averaged annualized realized gains of +21.3%! And with gold stocks down at fundamentally-absurd price levels and universally loathed today, their mean-reversion bull should be enormous.

So join us and start cultivating an essential contrarian perspective on these dangerous central-bank-distorted markets. Our subscription newsletters that pay for these popular web essays draw on our decades of exceptional market experience, knowledge, and wisdom to explain what's going on in the markets, why, and how to trade them with specific stocks. Subscribe today and enjoy our 20%-off sale!

The bottom line is American gold-futures speculators just savaged gold again on their historically-wrong and irrational belief that Fed rate hikes will decimate gold. Last week's surprisingly-hawkish FOMC statement unleashed furious gold-futures selling, battering gold back below its new uptrend's support line. But gold selloffs driven by futures shorting soon reverse, as those positions must soon be covered.

The higher the proportion of futures short selling compared to long liquidations that drove this latest sharp gold selloff, the more bullish gold looks in the near term. It won't take much gold buying, probably on the lofty overbought stock markets rolling over again, to ignite accelerating short covering. Any gold selloff driven by leveraged gold-futures shorting is short-lived, since that's all guaranteed near-future buying.