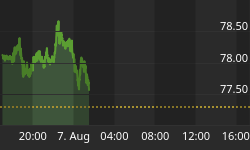

This past week, more than a few investors took a pass on gas - so to speak - selling their oil and gas investments. This is illustrated in the daily chart below which depicts trade in the S & P Energy Sector Index [XLE]. It should be clear for all to see that for the past six trading sessions in particular, the energy complex has been 'sucking wind' rather than blowing the same:

Chart compliments: www.stockcharts.com

With the energy stocks being so "hot" for much of the year to date, pullbacks are not only inevitable but they often provide the opportunity to add quality names that have inadvertently been sold off in any broad based consolidation in the context of a secular bull market like the energy complex is currently experiencing.

The above thought - perhaps presents a dilemma to some - in terms of what name[s] one should consider adding. Rather than getting into a long and drawn out discussion about particular names within the energy complex, I would like to offer a helpful hint as to how each investor might consider viewing the entire energy complex from a macro perspective. Following this 'sector approach,' one might better understand where the holes are in their existing portfolio and take the appropriate steps to fill the gaps accordingly.

What follows is the body of a piece from my Macro Economic News Letter, available through my web site. It outlines the energy complex from a macro perspective and embodies the most important investment advice I have ever received in my life from a very good friend who has traded professionally and very successfully for a living for many years. His over riding investment 'axiom' is this: If you've got a clear and accurate view of the BIG PICTURE - it almost becomes a chore to lose money over the long run. He spends most of his time trying to understand the big picture - often telling me there is literally 'mountains' of research available on an endless list of companies in the public domain. The trick - in his words - is understanding how the pieces best fit together.

In my experience, investment banks and broker-dealers view of the energy complex tend to be skewed by whomever they are courting [for their fees] for their capital raising requirements and often times, many of the pieces in the energy complex are overlooked or ignored. The energy companies in the oil and gas sector in particular, tend to receive little analyst coverage, as compared to tech names that burn lots of cash and require frequent re-financings. This is often due to the fact that energy companies, by nature, tend to generate lots of cash from their own businesses and are not as beckoning to Wall Street financiers as their investment bankers might wish. I believe that Peak Oil is not only real but is actually upon us now. As such, a decent understanding of all the pieces in play in this sector is in my mind, invaluable.

Hydro Carbon Related

Many investors tend to look at energy as simply oil and gas - and perhaps a big crap shoot. I view the energy sector more in terms of the following:

Integrated[s] - These tend to be the majors. They explore, ship, refine and often retail petroleum based products. By nature, they don't have all their eggs in one basket. Risks in holding are somewhat diminished through lessening of sector specific risks. Think in terms of low to moderate risk in holding over the medium to long term [3 - 15 yrs].

Light crude - Easily refined or West Texas Intermediate [WTI] grades. These are the higher grades of oil that are most often referred to in the "peak oil" debate and therefore with questionable or diminishing reserves. Existing refining infrastructure is highly geared to handle this type of oil. While reserve life is suspect [elevated capital risk] in many cases, look for enhanced earnings and higher yields, near term [2 - 5 yrs], going forward.

Heavy crude - As the name suggests, thicker, heavier oil typical of Tar Sands. There is less existing refining capacity for this type of oil and while reserves are plentiful - additional output requires massive capital expenditures and years of lead time. Reserve lives are longest and most dependable here; therefore expect lower yields but shelf lives that would be more consistent with retirement time frames [5 - 15 yrs].

Gas or LNG - as opposed to crude oil. Natural gas reserves are generally regarded to be more plentiful than traditional crude oil in much of Canada - a relatively well developed infrastructure exists including the pipelines required to bring the product to market in N.A. Exploitation of Natural Gas supplies in the Middle East are relatively 'new phenomena' with prospects of explosive growth - albeit with plenty of accompanying geo-political risk. An accompanying boom in ship building is underway [look to Korean shipyards to supply the ships] to facilitate transport of this resource to market with upwards of 300 LNG ships currently on the order books at roughly 300 million per. Good prospects, anticipate moderate yield, over the 5 - 15 year time frame.

Pipelines - Recommended sticking to contiguous N.A. in this sector. Geo-political risks [bombing, sabotage, mischief] in this sector are paramount. After mitigating these concerns, expect a dependable moderate yield with a 5 - 20 year time frame.

Shipping - This sector could be played a number of ways. I would identify the builders of ships/rigs, and the operators of ships/rigs. The operators can be further sub divided into the "spot" market and the long term charter trades. Ship builders tend to be boom/bust by nature [investment should be moderate to high yielding as a result] and investors should anticipate and be compensated with much higher yields for exposure in the spot market than in the long term charter trade. Time frame considerations in this sector range from perhaps 6 months [variable, spot with elevated risk] all the way out to 10+ yrs [when secured by long term charter with credit worthy counterparty] or more with moderate risk.

Drillers - These are the guys who poke holes in the ground. Potential geo-political considerations depending on where business is concentrated. Historically a volatile sector within a cyclical group - as long as elevated to rising energy prices persist, the outlook for this sector remains buoyant going forward. Anticipate moderate risk and yield over 2 - 5 year time frame.

Oil Field Services - This segment covers everything from pipeline maintenance to re-supply, logistics, oil field reservoir analysis and spare parts for oil rigs. Anticipate risk and returns in this sector to be commensurate with broad industry norms. Think in terms of 2 - 10 year time horizon with moderate risk.

Coal - With recent steep rises in price of crude oil, more expensive 'clean coal technologies' are becoming more viable as time goes on. Look for increased adoption rates in the areas of electricity generation in North America as the realities of Peak Oil set in and attempts are made to lessen dependence on imported energy sources. Risk profile on this type of energy source tends to be quite low since North America is naturally well endowed with many years of ample supply of this resource. With a lower risk profile expect a corresponding lower yield but relative stability in return over the long haul [5 - 50 yrs].

Biomass - This involves burning the residue from the forestry industry [bark, pulp, etc] to create steam and then electricity. This means of power generation is relatively new and more or less confined geographically to areas where forestry is practiced. The bonus to power generation of this sort is that its inputs are more or less 'renewable.' On the downside, this means has not yet been widely adopted and might be viewed as a developing technology. Making large bets on developing technologies is not recommended for the faint of heart - although the premise makes a great deal of economic sense. Not enough history or data points in this area to suggest time/yield appraisal. If I had to take a stab, I'd guess 5 - 10 year time horizon with a moderate risk rating.

Nukes

A good overview of what is driving demand in this segment of the energy complex might be gleaned by reading this N.Y. Times piece from Jan. 05. The gist of the article is that demand going forward, mostly from China, is likely to be explosive for nuclear energy. An explosive outlook in any industry is usually a good thing, unless of course you happen to be referencing Iran or North Korea and their supposed [alleged] nuclear/military ambitions.

How To Play The Nuke Sector?

Utilities - The folks who generate electricity using nuclear power. Utilities also employ coal, natural gas and oil as well as hydro to generate power. In a nutshell, what happens in a nuclear power station is that nuclear fuel is used to superheat water which in turn creates steam which drives a turbine to create electricity. Utilities generally have captive audiences [monopolies] in the jurisdictions that they operate. The costs and red tape associated with entry into the business are very large - and they are typically financed through the issuance of bonds [debt]. As such, as an investment, utility returns often tend to be tied as much to bond yields as energy prices. Do note, however, that nuclear power carries with it the stigma of the safe disposal of 'spent' nuclear fuel - a large and valid - but not insurmountable environmental concern. Anticipate risk and return to be low to moderate over the long term [2 - 10+ years].

Miners - The folks who extract uranium [nuclear fuel] from the ground. Anticipate moderate risk with moderate to high returns over the medium term [3 - 5+ yrs].

Exploration - The folks who go out and explore for new uranium deposits [reserves]. Anticipate very high risk with extremely high returns as compensation over a relatively short term [6 months - 2 yrs].

Hazardous Waste Disposal - The folks involved in the safe disposal of 'spent' nuclear fuel. This activity is highly regulated. Expect low to moderate risk with moderate return over the medium term [3 - 5 yrs].

Hydro Electric

This part of the energy complex is the oldest and likely the most understood and most reported. This involves the utilization of running water [river or dam] power to spin turbines to create electricity. This type of power generation necessarily requires rivers and typically the construction of a dam. Dam construction typically falls into the category of 'mega project' and as such require massive amounts of capital investment to complete, hence bond issuance and a tie-in - typically to a spread over government bond yields as much as the costs of competing forms of energy. While dams are expensive to build, they have very long shelf lives and as a result carry low risk profiles, accompanying low to moderate return expectations over the very long term [3 - 50 yrs].

Geothermal

Entails using the earth's internal heat to create steam - primarily for heating Purposes in areas that are seismically active - like Iceland. Limited wide scale application.

Alternative

This segment includes Wind Power and Solar. Wind power is one of the most promising and cost-effective renewable energy technologies available today. It involves utilizing wind power to spin a turbine [wind mill] to create electricity. Worldwide there are more than 13,000 megawatts (MW) of wind power installed. As a point of reference, it takes roughly 2,600 megawatts of capacity to power 750,000 homes in the U.S. Anticipate low to moderate risk with low to moderate return over the medium to very long term [3 - 50 yrs].

When most people think of solar power, they envision 'photovoltaic' or 'photoelectric' cells customarily seen on calculators or situated in arrays outside. This type of electricity generation had its genesis in the space industry and was originally conceived to provide minimal amounts of power required in the ongoing operation of satellites. As such, this means of power generation remains very expensive, even to this day, and is typically used in conjunction with or as an adjunct to other means of power generation. Limited wide scale application due to high costs.

How Do You Like Your Medicine?

As an investor, there are a couple of fundamentally different ways to own equity in the energy complex. The first is through common shares [which in many cases pay nominal dividends] which most investors are more than aware of. Another less publicized and perhaps not as well understood way is through Royalty Income Trusts - which typically pay much larger cash distributions [which usually include a small return of capital], typically monthly or quarterly:

The most controversial of income trusts are the royalty trusts which invest in mining or oil and gas properties. The reason is that mines and oil and gas wells have limited life spans. They eventually run out of oil or gas or coal or whatever.

Because of this, these trusts must periodically have a new public offering of shares to finance the purchase of additional properties, or they must wind up at some point, liquidating remaining assets and distributing the proceeds to the unit holders.

They are also subject to the vagaries of the commodity markets. Oil goes up. Profits go up. Distributions go up. And vice versa. Right now, the oil and gas trusts are riding high with excellent yields and rising unit prices - the best of both worlds. But if oil prices head south again, the distributions will shrink and the share prices will drop.

With all that I've said here today, I've run out of room, I'll have to leave my diatribe about the Refco fiasco for next week!