The market finished with its third consecutive weekly loss and the worst start to any new year. Sinking commodity prices and slowing global economic growth are the main contributors to the weakness. For the week, the S&P 500 Index and the Blue Chip-heavy Dow Jones Industrial Averages were both down by 2.2%. The Nasdaq finished the week down 3% while the small cap Russell 2000 Index led the major indices down 3.6%. The chart below shows the major indexes in a full-blown correction with Gold Miners and Russell 2000 in bear market territory.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the general stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. The chart below confirms stocks are in a serious downtrend and headed back to the September low.

As noted in the weekly chart below, MTUM has closed below the 50-week MA for the first time since the stock market correction at the end of last summer. If the MTUM does not snap back over the next week or so that would signify serious structural damage to the market. As highlighted, the chart has already confirmed bearish momentum for the first time since the last market correction.

Most of the current discussion about market pricing is focused on how investors' perceptions are causing oil prices to fluctuate. As seen in the chart below, as the dollar has strengthened commodity prices have been in freefall. Weakening demand for oil and all manner of commodities is fueling the perception of an imminent recession.

Market Outlook

Crude oil prices fell below $30 a barrel, hitting levels not seen since 2004 is causing investors to panic. Falling energy prices should be considered a good thing as it lowers the cost of doing business for a wide assortment of industries, ranging from manufacturing to transportation. But in this case investors are worried that historically cheap crude and crashing commodity prices is an ominous sign that global demand is far weaker than economists think. Indeed, the last two times that crude oil prices even came to $30 a barrel was in 2008, amid the global financial crisis and Great Recession; and in 2000, when the bursting of the internet bubble pushed the U.S. economy into a recession. As discussed above, the large cap indexes have officially fell into a correction and the small caps are actually in a bear market. This has triggered a new set of worries that the bull market that began in March 2009 could be petering out, which has led to even more selling. Since 2009, this bull market has withstood five market corrections and bounced back each time. Most recently, stocks lost 12.4% during the late August market slide which took place for the exact same reasons the market is jittery today, a combination of global slowdown fears and cheap oil. But the Dow bounced back more than 11% through the end of last year, rewarding investors who hung in there. The chart below confirms investors are trading "risk off" as the only positive asset classes since the beginning of December are bonds and gold.

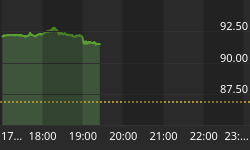

Put/Call Ratio is the ratio of trading volume of put options to call options. The Put/Call Ratio has long been viewed as an indicator of investor sentiment in the markets. Times where the number of traded call options outpaces the number of traded put options would signal a bullish sentiment, and vice versa. Technical traders have used the Put/Call Ratio for years as an indicator of the market. Most importantly, changes or swings in the ratio are seen as instances of great importance as this is commonly viewed as a change in the tide of overall market sentiment. The current ratio indicates traders remain extraordinarily bearish during the sell off as they pile into option put contracts to protect against a bear market crash.

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends VIX higher. As highlighted in the weekly chart below, the 'Fear Gauge' climbed back up to the high levels established during the last correction at the end of last summer. As long as the VIX stabilizes below the current level we can expect a near term counter-trend relief bounce. When the market is in full-blown panic mode, the VIX approaches a reading of 40. That's roughly double the historic level. This happened in 2008, during the global financial crisis, and in the late 1990s, leading up to the 2000 tech crash that triggered a global bear market. So far this year, the VIX has been nowhere near panic levels.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 01/13/2016. The most recent AAII survey showed 17.90% are Bullish and 45.50% Bearish, while 39.60% of investors polled have a Neutral outlook for the market for the next six months. The current AAII Survey bearish percentage is elevated higher than during correction at the end of last summer, while the bullish reading is lower than the low from last summer. The current AAII survey signals a short-term counter trend bounce based on retail investors' extremely bearish sentiment.

The Nation Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 01/13/2016. Fourth-quarter NAAIM exposure index averaged 44.61%. Last week the NAAIM exposure index was 50.26%, and the current week's exposure is 34.50%. Similar the market correction at the end of last summer, professional money managers continues to reduce equity exposure during the current market selloff. Don't be surprised if the NAAIM exposure index falls to the lows from the beginning of October.

Trading Strategy

Last week's commentary is still valid where we said "...Trader mentality has switched from years of buying dips to 'Selling Rallies' based on the action the last few months. In the graph below the only winning S&P 500 sector over the past month is Utilities. Similar to Treasury bonds, investors are putting funds into Utility company stocks as a safe-haven during the current market turmoil..." The flight to safety in the markets is in vogue as the 'Risk-Off' trading is on.

Feel free to contact me with questions,