ECB president Mario Draghi is under self-imposed pressure to do something dramatic on March 10 to ward off fictitious problems that he associates with consumer price deflation.

To that end, the market expects Draghi will crawl further down the rabbit hole by cutting its benchmark rate by 10 basis points (0.1 percentage points) to -0.4%.

Will that provide the drama Draghi seeks?

In its post Here's How Draghi Can Free Up $900 Billion of Debt for QE, Bloomberg estimates Draghi could "free up" $478 billion worth of QE eligible bonds by cutting the rate to -0.4% and $903 billion with a cut to -0.6%.

About $900 billion of sovereign debt that meets maturity criteria for the European Central Bank's quantitative-easing plan yields less than its deposit rate, putting the securities out of reach of the program. A 10 basis-point cut to minus 0.4 percent at this week's meeting, the median estimate of economists, would free up about $478 billion, according to the Bloomberg Eurozone Sovereign Bond Index, with 20 and 30 basis-point cuts bringing another $268 billion and $157 billion into play respectively. The risk is the benefits may be short-lived -- yields have fallen further since the ECB, led by President Mario Draghi, cut its deposit rate in December.

Freed Up for What?

By "freed up", Bloomberg means the ECB could cut rates deeper into negative territory so that the ECB's benchmark rate is lower (more negative) than some $900 billion in bonds that already trade with a yield less than 0.30%.

Bonds trading at yields higher (less negative) than the ECB's benchmark rate would be eligible for QE.

Ludicrous Example

Got that? Some $900 billion in bonds yield between -0.3% and -0.6%.

The following weekly chart of German 2-years bonds shows yields have been negative since August 23, 2014.

Ludicrous Discussion

It's clearly ludicrous for bonds to have negative yields, but here we are. And Draghi is expected to increase the degree of ludicrousness on March 10.

Would that "free up" anything?

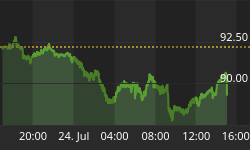

I expect not. Bond rates are ahead of the ECB, thanks to its telegraphing every move in advance. Here's a beautiful example, also with Germany 2-year bonds. This time, a daily chart highlights recent action.

.

.

That big green candle is from the ECB's last meeting on December 3. At that time, the market threw a hissy fit but Draghi quickly stepped in to promise more action, and the market responded in advance.

Given that ECB asset purchases are run about $60 billion a month, it would take 15 months for the ECB to burn through $900 billion in stimulus.

15 months from now, who knows how deep the rabbit hole will be?

How to Free Up €14 Trillion

A quick check of ECB's Euro Denominated Securities Report shows the ECB might be able to "free up" €14 trillion ($15.4 trillion) with the right policy move now.

Since that's where we are ultimately headed, Draghi may as well make that announcement on March 10 and do it all at once.

By the way, I am not sure if such a move a would cause the least bit of consumer price inflation. Instead, it might crash the system.

However, the benefit of such a move is obvious. We could finally get the bazooka proponents to shut up.