Cyclicals Have Lost Their Confident Look

We can learn a lot from the chart below, which shows the performance of economically-sensitive stocks relative to the S&P 500. After the S&P 500 bottomed on February 11, cyclicals (XLY) took the lead off the low as economic confidence started to improve. Notice the steep slope of the ratio off the recent low (see green text). The confident look has morphed into a more concerning look as the S&P 500 has continued to rise over the last month (orange text), which tells us to keep an open mind about a pullback in the stock market.

A similar picture emerges when we examine the high beta stocks (SPHB) to S&P 500 ratio below.

What Can We Learn From The Longer-Term View?

This week's stock market video examines the question:

What can we learn from asset class behavior?

The video covers low beta stocks (SPLV), consumer staples (XLP), Treasuries (TLT), high-yield bonds (JNK), NASDAQ (QQQ), Dow (DIA), NYSE Composite Stock Index (VTI), VIX (VXX), crude oil (USO), emerging markets (EEM), transportation (IYT), energy (XLE), and materials (IYM).

Back To The Shorter-Term Charts

The economically-sensitive materials sector (XLB) has significantly lagged the S&P 500 over the past two weeks.

Given the consumer is often referred to as the life blood of the U.S. economy, the tepid relative performance of the retail (XRT) ETF since March 8 is a bit concerning.

If problems return to the oil patch, problems may return in the credit markets. Oil peaked relative to the S&P 500 over 2 weeks ago.

Transportation stocks have made little to no progress relative to the broader stock market since early March.

Brazil (EWZ) has been one of the best performing ETFs since late January 2016. As shown in the EWZ/SPY chart below, the ratio has stalled in recent weeks.

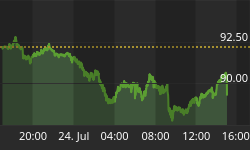

If credit leads stocks, then the chart below tells us confidence in the current stock market rally may be waning.