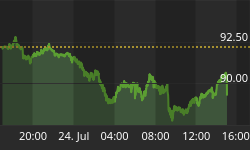

A longtime reader (and friend) today forwarded me a chart from a well-known technical analyst showing the recent correlation between TIPS (via the TIP ETF) and gold; the analyst also argued that the rising gold price may be boosting TIPS. I've replicated the chart he showed, more or less (source: Bloomberg).

Ordinarily, I would cite the analyst directly, but in this case since I'm essentially calling him out I thought it might be rude to do so! His mistake is a pretty common one, after all. And, in fact, I am going to use it to illustrate an important point about TIPS.

The chart shows a great correlation between TIPS and gold, especially since the beginning of the year. But here's the problem with drawing the conclusion that rising inflation fears are boosting TIPS - TIPS are not exposed to inflation.

Bear with me, because this is a key point about TIPS that is widely misunderstood. Recall that nominal interest rates represent two things: first, an amount that represents the return, in real terms, that the lender needs to realize in order to defer consumption and instead lend to the borrower. This is called the real interest rate. The second component of the nominal interest rate represents the compensation the lender demands for the fact that he will be paid back in dollars that (in normal times) will be able to buy less. This is the inflation compensation.[1] Irving Fisher said that nominal interest rates are approximately equal to the sum of these two components, or

n ≈ r + i

where n is the nominal interest rate, r is the real interest rate, and i is the inflation compensation.[2]

In a world without TIPS, you can only trade nominal bonds, which means you can only access the whole package and nominal interest rates may change when real rates change, expected inflation changes, or both change. (And when interest rates are negative, this leads to weird theoretical implications - see my recent and fun post on the topic.) Thus changes in real interest rates and changes in expected inflation affect nominal bonds, and roughly equally at that.

But once you introduce TIPS, then you can now separate out the pieces. By buying TIPS, you can isolate the real interest rate; and by trading a long/short package of TIPS and nominal bonds (or by trading an inflation swap) you can isolate the inflation expectations. This is a huge advance in interest rate management, because an investor is no longer constrained to own a fixed-income portfolio where his exposure to changes in real rates happens to be equal to his exposure to changes in inflation expectations. Siegel and Waring made this argument in a famous paper called TIPS, the Dual Duration, and the Pension Plan in 2004,[3] although it should be noted that inflation derivatives books were already being managed using this insight by then.

Which leads me in a roundabout way to the point I originally wanted to make: if you own TIPS, then you have no exposure to changes in inflation expectations except inasmuch as there is a (very unstable) correlation between real rates and expected inflation. If inflation expectations change, TIPS will not move unless real rates change.[4]

So, if gold prices are rising and TIPS prices are rising, it isn't because inflation expectations are rising. In fact, if inflation expectations are rising it is more likely that real yields would also be rising, since those two variables tend to be positively correlated. In fact, real yields have been falling, which is why TIP is rising. The first chart in this article, then, shows a correlation between rising inflation expectations (in gold) and declining real interest rates, which is certainly interesting but not what the author thought he was arguing. It's interesting because it's unusual and represents a recovery of TIPS from very, very cheap levels compared to nominal bonds, as I pointed out in January in a piece entitled (argumentatively) "No Strategic Reason to Own Nominal Bonds Now."

Actually (and the gold bugs will kill me), gold has really outstripped where we would expect it to go, given where inflation expectations have gone. The chart below (source: Bloomberg) shows the front gold contract again, but this time instead of TIP I have shown it against 10-year breakevens.

>

>

No, I don't hate gold, or apple pie, or America. Actually, I think the point of the chart is different. I think gold is closer to "right" here, and breakevens still have quite far to go - eventually. The next 50bps will be harder, though!

[1] I abstract here from the third component that some believe exists systematically, and that is a premium for the uncertainty of inflation. I have never really understood why the lender needed to be compensated for this but the borrower did not; uncertainty of the real value of the repayment is bad for both borrower and lender. I believe this is an error, and interestingly it's always been very hard for researchers to prove this value is always present and positive.

[2] It's technically (1+n)=(1+r)(1+i), but for normal levels of these variables the difference is minute. It matters for risk management, however, of large portfolios.

[3] I expanded this in a much less-famous paper called TIPS, the Triple Duration, and the OPEB Liability: Hedging Medical Care Inflation in OPEB Plans in 2011.

[4] What the heck, one more footnote. I had a conversation once with the Assistant Treasury Secretary for Financial Markets, who was a bit TIPS booster. I told him that TIPS would never truly have the success they deserve unless the Treasury starts calling 'regular' bonds "Treasury Inflation-Exposed Securities," which after all gets to the heart of the matter. He was not particularly amused.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"