Pretend, for a minute, that your country responds to the bursting of a credit bubble by borrowing unprecedented amounts of money and using it to prop up banks and construction companies. This doesn't work, so you create record amounts of new money and push interest rates into negative territory in an attempt to devalue your currency. But this -- amazingly -- doesn't work either. Your currency soars and the inflation you'd hoped to generate never materializes.

Now what? Is there even anything left to try, or is it simply time to stand back and let the current system melt down? Those are the questions facing Japan, and the answers are not obvious. Here, for instance, is its inflation rate two years into the largest major-country money creation binge since Wiemar Germany:

Deflation is to be expected and even desired in a well-run country where debt is minimal, money is sound and rising productivity makes things continuously cheaper. But in an over-indebted financial system, deflation is death because it magnifies the debt burden and raises the odds of an existentially threatening financial crisis. To continue to borrow money under such circumstances is to court disaster. And yet Japan is still at it:

What we're witnessing, in short, is a catastrophic loss in the currency war. Contrary to every mainstream economic theory, debt monetization and full-throttle currency creation have resulted in a rising yen and falling prices. Here's an excerpt from a recent -- and really gloomy -- Financial Times analysis of Japan's situation:

It's time for investors to admit it: Abenomics has failed

The past few weeks have not been happy ones for many central bankers -- and none more so than Haruhiko Kuroda, the hapless governor of the Bank of Japan.That is because the threat of moving rates deeper into negative territory and buying up even more assets has done nothing to weaken the yen down as he desires. Brexit, which briefly sent the yen beyond the ¥100 mark against the dollar on Friday, is a fresh headwind.

The Bank of Japan is likely to move rates from negative 0.1 per cent to minus 0.3 per cent come the end of July, increase its holdings of ETFs from ¥3.3tn to ¥6.3tn as well as its purchases of Japanese Reits from ¥90bn to ¥200bn, economists at JPMorgan in Tokyo predict.

With the yen ever stronger, Abenomics and the desired impact of central bank policies are going into reverse. The irony is that these policies, which were meant not to change traditional Japan but to revive it, are likely to end up wounding it -- perhaps irreparably.

Abenomics was never about real reform. Instead, it was merely meant to weaken the currency, undercutting competitors like Korea and China and allowing Japan Inc to more easily export its cars and other manufactured goods to the rest of the world.

Since corporate profits for the last three years were only ever about currency translation gains, these are now going in reverse and dragging down industrial shares with them.

Surveys suggesting companies plan to invest have failed to materialise: in April core machinery orders, the best proxy for capex, dropped 8.2 per cent from the previous year, while exports fell in May with the trade surplus down 32 per cent compared with the previous month.

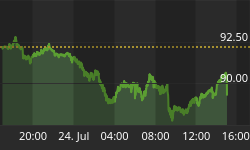

The March tankan survey showed corporate Japan expected the yen/dollar rate at ¥117 going forward -- today it sits at ¥101.5 to the dollar. Masaaki Kanno, chief Japan economist for JPMorgan, expects the currency to surge to ¥90 next year.

Meanwhile, negative rates are especially murderous for bank shares. "Why should a central bank policy that hurts bank shares be good for a credit-driven economy?"asks Christopher Wood, strategist for the CLSA unit of Citic Securities.

In a way, the fact that Mitsubishi UFJ is preparing to give up its primary dealership in the government bond market is immaterial -- at least from a narrow economic or financial perspective. The Bank of Japan's purchases of JGBs far exceed net new issuance. Trading volumes have collapsed.

But as a symbolic political gesture it is huge, suggesting that the mutual support and trust of the old convoy system have totally broken down. Moreover, it is no accident that the protest comes from Nobuyuki Hirano.

There are other signs that the private sector has become less compliant as well. Both the heads of the GPIF and Japan Postal Savings say this is no time to buy risky assets at home since they reflect only the BoJ's buying (and perhaps foreign fund front-running of that buying). Given the flat yield curve, insurers can hardly hold JGBs, and anyway fear losses on their holdings should rates eventually move up.

In addition, there is likely worse to come for many major investors. They have been pushed abroad by the central bank. But with the yen rising in a world which has been mostly risk-off, they will have big losses on assets held in foreign currencies, especially since only a small part of their exposures have been hedged, according to data from JPMorgan.

Rather than reboot Abenomics, it is time to replace it. Investors should not bet on Japan any longer.

So what happens -- and doesn't happen -- now? Several things:

The bad stuff gets worse. Post-Brexit Europe will be a source of anxiety and therefore capital flight for years. See What is Frexit: Will France leave the EU next?

That means more money looking for a place to hide, some of which will choose yen-denominated bonds. So Japan's already-negative interest rates will fall even further, which is catastrophic news for the Japanese banks and pension funds now suffocating under the current yield curve.

Regime change -- but not yet. In upcoming elections the ruling party looks likely to hold its legislative majority. Longer term, though, Japan will find itself in pretty much the same boat as every other major democracy, with inept incumbents having handed lethal ammo to opposition parties more than willing to pull the trigger. New leaders won't be able to fix the problem (which is by now unfixable) but the uncertainty surrounding a contested election will raise the odds of a crisis of involving currencies, debt, banks or any number of other things.

Plunging US rates. Eventually, hundreds of trillions of yen will have to find a new home with more hospitable returns. And 30-year Treasuries yielding 2% will look pretty tasty in a relative if not absolute sense. Rising foreign demand will push down Treasury yields, killing off numerous US banks, pension funds and insurance companies but giving the remaining solvent Americans a chance to refinance their mortgages at 1%.

Governments become the biggest stock market players. This is already happening, as Japan, China and (probably) the US buy equities and ETFs to blunt natural corrections in share prices. But with nothing else left to try, expect these programs to be ramped up virtually everywhere. This will prop up stock prices until it doesn't, and then look out below.

Soaring gold. Everything that happens these days points to higher precious metals prices. I'm thinking of writing a piece of boilerplate to that effect for placement at the end of every future article.