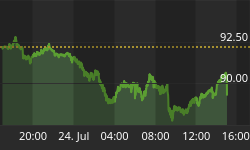

The last two weeks of July felt a lot like August typically does. Thin, lethargic trading; somewhat gappy but directionless. Ten-year Treasury note futures held a 1-point range except for a few minutes last Thursday. The S&P oscillated (and it really looks like a simple oscillation) between 2160 and 2175 for the most part (chart source Bloomberg):

In thinking about what August holds, I'll say this. What the stock market (and bond market) has had going for it is momentum. What these markets have had going against them is value. When value and momentum meet, the result is indeterminate. It often depends on whether carry is penalizing the longs, or penalizing the shorts. For the last few years, with very low financing rates across a wide variety of assets, carry has fairly favored the longs. In 2016, that advantage is lessening as short rates come up and long rates have declined. The chart below shows the spread between 10-year Treasury rates and 3-month LIBOR (a reasonable proxy for short-term funding rates) which gives you some idea of how the carry accruing to a financed long position has deteriorated.

So now, dwelling on the last few weeks' directionless trading, I think it's fair to say that the markets' value conditions haven't much changed, but momentum generally has surely ebbed. In a situation where carry covers fewer trading sins, the markets surely are on more tenuous ground now than they have been for a bit. This doesn't mean that we will see the bottom fall out in August, of course.

But add this to the consideration: markets completely ignored the Fed announcement yesterday, despite the fact that most observers thought the inserted language that "near-term risks to the economic outlook have diminished" made this a surprisingly hawkish statement. (For what it's worth, I can't imagine that any reasonable assessment of the change in risks from before the Brexit vote to after the Brexit vote could conclude anything else). Now, I certainly don't think that this Fed, with its very dovish leadership, is going to tighten imminently even though prices and wages (see chart below of the Atlanta Fed Wage Tracker and the Cleveland Fed's Median CPI, source Bloomberg) are so obviously trending higher that even the forecasting-impaired Federal Reserve can surely see it. But that's not the point. The point is that the Fed cannot afford to be ignored.

Accordingly, something else that I expect to see in August is more-hawkish Fed speakers. Kansas City Fed President Esther George dissented in favor of a rate hike at this meeting. So in August, I think we will hear more Esther and less Mester (Cleveland Fed President Loretta Mester famously mused about helicopter money a couple of weeks ago). The FOMC doesn't want to crash the stock and bond markets. But it wants to be noticed.

The problem is that in thin August markets - there's no escaping that, I am afraid - it might not take much, with ebbing momentum in these markets, to cause some decent retracements.

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"