Japan and Europe have been operating with negative interest rates for going on a year now, and this is what they have to show for it:

For readers who aren't completely clear about the GDP charts, they're measuring the annual rate of change, so 0.4% means an economy is growing at a rate of less than ½ of 1%. This is about as close to zero as it's possible to get without enduring actual shrinkage. Clearly the new-age policy mix of negative interest rates and massive central bank bond buying isn't working.

Mainstream economists want to up the ante by lowering rates even further. But there are reasons to believe that not only won't such a policy work but that it won't be tried. For one thing, negative rates are already killing the banks. In Japan, for instance:

Negative rates seen reducing Japan big banks' profits by $2.96 billion: Nikkei

(Reuters) – Japan's financial watchdog estimates that negative interest rates under the Bank of Japan's monetary easing policy will reduce profits for the country's three big banks by at least 300 billion yen ($2.96 billion) for the year through March 2017, the Nikkei business daily reported on Saturday.

The Financial Services Agency (FSA) expressed concern to the BOJ regarding the situation as it sees reduced profits weakening the banks' ability to extend loans, the Nikkei said.

According to FSA estimates, Mitsubishi UFJ Financial Group Inc's profit will fall by 155 billion yen. Sumitomo Mitsui Financial Group Inc's profit will be reduced by as much as 76 billion yen and that of Mizuho Financial Group Inc will be cut by 61 billion yen.

If the BOJ was to take interest rates deeper into negative terrain, the agency reckoned that the banks would suffer substantial further drops in profit as their interest rate income would suffer.

In Germany, Deutsche Bank is so badly run that teasing out the effects of any one problem isn't easy. But negative interest rates do seem to be in the mix. From a recent Zacks Research report:

Deutsche Bank's Profitability at Risk from Macro Concerns

Profitability growth of Deutsche Bank, one of the largest financial institutions in Europe and the world, as measured by total assets (€1.80 trillion as of Jun 30, 2016), remains threatened by a stressed operating environment with negative interest rates, slow growth of the European economy and global headwinds. Management continues to see a challenging revenue environment in 2016, specially post Brexit vote.

Last month the German banking giant reported net income of €20 million ($22.6 million) for the second quarter of 2016, significantly down on a year-over-year basis. Income before income taxes came in at €408 million ($460.7 million), down 66.8% year over year. Results were adversely impacted by reduced revenues and higher provisions, partially offset by lower expenses which resulted from reduced litigation as well as compensation costs.

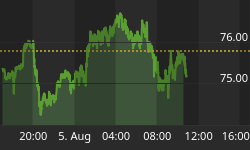

DEUTSCHE BK AG Price

As the article on Japanese banks noted, more negative interest rates will suck even more life from the banks. Since 1) they're already on life support in a lot of cases and 2) even in their currently diminished state they remain immensely powerful politically, it's highly unlikely that we'll see -3% yields on government bonds in this cycle.

But if not that, what? Banks are shrinking around the world – as are pension funds and insurance companies and everyone else who depends on positive fixed income returns. National economies aren't growing, while national debt burdens continue to soar. Staying the course in this case means drifting over the falls.

So the next round of experiments will probably feature bigger deficits and more aggressive public hand-outs. Which – since these have already been tried and failed – doesn't give much hope for the future.