Market Summary

The Dow Jones Industrial Average finished the week with a gain of 0.8% while the S&P 500 recorded its best weekly performance in more than two months finishing up 1.2%. The Midcap S&P 400 rose 1.48% for the week while the small cap Russell 2000 led the way up 2.44%. The Nasdaq Composite index ended the week higher 1.20%. All the major asset classes remain in the black year-to-date.

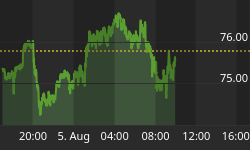

Last week we said "...Nasdaq 100 index diverging away higher from the Dow and S&P indexes. Tech stocks have led the market the past month. If this pattern continues it signals the current pullback may have ended and prices can be expected to reverse higher. Especially if investors like what they hear from next week's FOMC meeting that will almost certainly move the overall market higher..." In the updated graph below you can see investors' positive response from the Feds decision not to raise rates pushed equity indexes higher.

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. The Volatility Index fell 20 percent last week, its biggest drop since July 1. You can see in the updated chart below the VIX has sunk back down to its lowest support level. Unless there is some type of unexpected global economic event, it is reasonable to expect the Volatility Index to remain subdued for the next month or so.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 09/21/2016. The percentage of individual investors expressing pessimism about the short-term direction of the stock market is at its highest level since February. This week's AAII Sentiment Survey also shows a slight increase in neutral sentiment and a further decline in optimism. Bullish sentiment, expectations that stock prices will rise over the next six months, fell 3.1 percentage points to 24.8%. The drop keeps optimism at its lowest level since June 22, 2016 (22.0%). Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, edged up 0.7 percentage points to 36.9%. The increase puts neutral sentiment above its historical average of 31.0% for the 34th consecutive week. Bearish sentiment, expectations that stock prices will fall over the next six months, rose 2.4 percentage points to 38.3%. Pessimism was last higher on February 10, 2016 (48.7%). During the past two weeks, pessimism has jumped by a cumulative 9.8 percentage points, while optimism has fallen by a cumulative 5.0 percentage points. Concerns continue to exist about a potentially larger drop in stock prices than occurred earlier in the month.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers 7have made to client accounts over the past two weeks. The current survey result is for the week ending 09/21/2016. Second-quarter NAAIM exposure index averaged 60.52%. Last week the NAAIM exposure index was 68.55%, and the current week's exposure is 79.21%. Equity exposure fell from historically lofty levels, as investors appeared to be concerned about September underperformance and cautiousness ahead of this week's FOMC announcement. The NAAIM index jumped after the Fed left rates unchanged and money managers start repositioning for the end of third-quarter window dressing.

Trading Strategy

As seen in the updated chart below, Technology and Utilities are the only major S&P ETF sectors in the black over the past month. As reported by Jeff Hirsh in the Stock Trader's Almanac, since 2008, DJIA, S&P 500, NASDAQ and Russell 2000 have not fared all that well during the last five trading days of the third quarter, the end of September. 2010 was the last year where the major indices produced solid, across-the-board gains. S&P 500 has been the worst since 2008, down 7 of the last 8 years during the last five days of Q3.

Feel free to contact me with questions,