The imbalance in the London paper metals markets, where unbacked paper contract claims for metal are traded as a substitute for physical metal thus containing precious metals prices, first drew our attention to palladium in 2014 and more recently in March 2015 as the global physical palladium market supply deficit became more pronounced.

There had previously been a crisis in London's platinum and palladium market in 1997 that had driven the short-term palladium lease rate to 300% p.a. The London paper metals market was saved in 1997 by Russia providing from its estimated 20M to 25M palladium stockpiles at that time and over the next 17 years to fill the gap between mined and recycled palladium supply and the total global annual demand for palladium. In the years 2005 to 2009 the supply from Russian stockpiles had declined to approximately 1M oz per year but this was still an important component of global palladium market supply.

Annual Russian mine production of palladium is approximately 2.6M oz per year or 41% of the 6.3M oz of global mine supply. The annual addition by Russia of 1M oz of stockpile sales set Russia's total annual supply to the world market at 3.6M oz n 2009 helping meet total global annual raw palladium demand of 8.7M oz. and that amount of supply thereafter began to decline toward Russia's annual mine output of palladium indicating that supply from Russia's historic stockpiles was running out.

Russia's Exit as Enabler of the London Palladium Market

It now appears that Russia has materially reduced its supply of palladium to the global palladium market and there are signs of growing physical shortage in the market. The scale of the reduction in supply by Russia appears to have been unnoticed in the palladium market until now.

We can find evidence of the large decline in Russia's palladium supply to the world market by looking to global export statistics. In the table at the following link (http://www.worldstopexports.com/palladium-exports-by-country/), we can see that Russia exported only $675.6M of raw palladium in 2015 or 0.98M oz of palladium at the 2015 average price of $691/oz and that the UK exported 1.88M oz of raw palladium during the same year.

Using the same source, in 2015 Russia exported .98M oz of total palladium (raw plus manufactured) and the UK exported 2.75M oz of total palladium. In other words, Russia's supply to the world market of palladium declined to 1M oz in 2015 from 3.6M oz in 2009.

It appears from these statistics that UK stockpiles were being drawn-down to replace the reduction in supply from Russia to the world palladium market in 2015 and likely in years prior. This raises the question as to how large are the UK stockpiles of palladium available for sale?

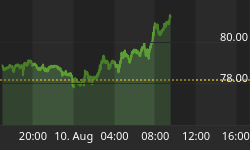

We may be getting a hint from recent London palladium lease rates. The following chart shows London's palladium forward rate ( palladium forward rate = LIBOR interest rate - palladium lease rate) has recently started to spike negative indicating increasing palladium lease rates and physical palladium tightness. While these rates are not yet 300% p.a., they bear watching.

Data source: Commerzbank

As all of the precious metals in London suffer from the same lack of physical metal to deliver into the paper spot contract claims, when disruption comes it will likely not be limited to any one metal market.