Market Summary

U.S. equities closed at all-time highs on Friday once again, as the major indexes posted their best week since the election. Bullish sentiment spreads across most sectors and short sellers are scrambling to cover at elevated prices. For the week, the S&P 500 Index and the Blue Chip-heavy Dow Jones Industrial Average both rallied another 3.1%. The Nasdaq gained a hefty 3.2% and the MidCap 400 jumped 4.20%, while the small cap Russell 2000 led equities again finishing the week up a massive 5.6%.

Last week we said "...You can see that the Nasdaq stocks are lagging the other major equity indexes. This can be considered non confirmation of the current trend, especially considering tech stocks have been leading the market higher all year...Tech stocks usually set the overall market direction, if this is still true the market is due for pullback unless the Nasdaq recovers..." As evidenced in the updated chart below, the Nasdaq has reversed course and moved higher to confirm that the current bullish move has legs.

Recent commentary mentioned "... an unintended consequence of Trump's victory has been the surge in the U.S. dollar...when factoring in potential protectionist trade policies and the overall global deflationary environment, you could easily argue that the recent dollar move has the potential for a much bigger upside. The very sharp rise in real market-driven interest rates is the clear driver of the dollar at present...Higher interest rates and stronger dollars are both are negative for precious metals and bond prices..." You can see in the updated chart below that as the dollar remains elevated bonds and precious metals are sinking from the higher rates.

Market Outlook

Daily new record highs are giving investors encouragement, or at least calming fears about a drop occurring in the short term, the election's outcome remains front and center for many investors. Some market pundits are encouraged by possible changes President-elect Donald Trump could make, while others are uncertain or want to wait to see how his administration's policies and their impact evolve. There are also some bears that are still pessimistic following the election. Beyond the election, the direction of interest rates, the pace of economic and earnings growth, and valuations are influencing investors' expectations for the stock market. The Dow Transports just issued a Dow Theory Buy signal by breaking out to a new high this past week. The current post-election bullish rally looks like it's got more room to roam and falls in line with November historically being the start of best six consecutive months for the stock market. The updated graph below displays fourth quarter performance for the major asset classes. The biggest under performers are gold, bonds and real estate which are expected to suffer from higher interest rates.

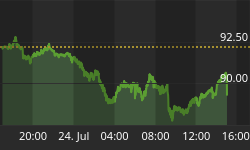

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. In the chart below, as the S&P 500 reached all-time highs the Volatility Index crashed as investors are not anticipating any surprises from next week's Fed meeting.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 12/07/2016. Optimism among individual investors about the short-term direction of the stock market is above 40% for a fourth consecutive week for the first time in approximately two years. This week's AAII Sentiment Survey also shows a decline in neutral sentiment and a modest rise in pessimism. Bullish sentiment, expectations that stock prices will rise over the next six months, declined 0.7 percentage points to 43.1%. This marks the fourth consecutive week that optimism is above 40% and the fifth consecutive week that it is above its historical average of 38.5%. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, declined 0.7 percentage points to 30.4%. The modest decrease drops neutral sentiment back below its historical average of 31.0%. Bearish sentiment, expectations that stock prices will fall over the next six months, rose 1.4 percentage points to 26.5%. Even with the increase, pessimism is below its historical average of 30.5% for a fifth consecutive week. Bullish sentiment readings in the low- to mid-40s have been a normal occurrence throughout the history of the survey. During most of the past 24 months, however, readings above 40% have been fairly rare. For example, the last time optimism held above 40% on four consecutive weeks was December 25, 2014, through January 15, 2015. In total, there have only been 14 weeks over the past 24 months with optimism at or above 40%.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 12/07/2016. Third-quarter NAAIM exposure index averaged 80.32%. Last week the NAAIM exposure index was 98.02%, and the current week's exposure is 101.60%. You can see how the NAAIM Exposure Index is at the highest level in over a year and half. Our recent analysis remains valid as we said "...The NAAIM Exposure Index will probably trend higher leading up to the December FMOC meeting...The Trump rally continues unabated as investors rotate money out of bonds and other defensive sectors into shares of companies that are expected to benefit under a Trump administration... Most probably, how investors interpret comments from the December 14th FOMC meeting will influence whether the NAAIM Exposure Index remains at elevated levels..."

Trading Strategy

In a recent issue of the Almanac Trader Jeff Hirsh talks about how next week's December's option expiration has a bullish history. In fact, the week of options expiration and the week after have the most bullish record of all Triple Witching expirations. As we have been saying recently "...investors having been selling off bonds, gold, utilities and other defensive sectors...investors are rolling into financial, industrials and energy sectors...historically, November begins the best consecutive six-months for the stock market..." There should be another opportunity to bid on stocks from your watch list during the next market pause. Tax selling is about to commence as investors dump under performers, also next week's FOMC meeting should be a nonevent, but the current upward move might stall a bit while investors try to decipher Fed comments.

Feel free to contact me with questions,