Market Summary

The market ended flat last week. For the week, the S&P 500 Index and the Blue Chip-heavy Dow Jones Industrial Average were basically flat closing up .7% and .9% respectively. The Nasdaq rose .4% and the MidCap 400 moved up .2%, while the small cap Russell 2000 gained .03%. As seen in the chart below, since the presidential election the major stock indexes have been soaring. The only major asset classes to fall during this time are precious metals and bonds which are being adversely impacted by the probability of higher interest rates from the Fed.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the overall stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. The updated chart below maps the aggressive bullish surge. Last week we said "... now we are starting to see the first technical signs indicating a possible pullback since the so-called Trump rally started. Overbought markets like the current situation can continue indefinitely, but now stock prices are converging into a tight range near resistance levels. Also, momentum levels are starting to turn down..." You can’t time a market top and stocks can keep churning higher despite being extremely overbought.

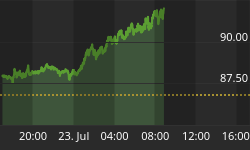

In the chart below the dollar climbed to the highest level in six weeks, after Federal Reserve Chairwoman Janet Yellen signaled that the central bank would likely raise interest rates at its coming meeting. Yellen said raising interest rates in March would "likely be appropriate," confirming what has been a rapidly growing cadre of support from Fed officials around a rate hike in mid-March. Treasuries and gold booked a sharp weekly drop, as a chorus of Federal Reserve officials decisively shifted market expectations for a March rate hike.

Market Outlook

Jeff Hirsch in the Almanac Trader talked about how the history of S&P 500 gains in January and February offers further support for continued strength. In 87 years going back to 1930, S&P 500 has been positive in January and February 33 times. Strength continued into March in 22 of those years and the full year was up 29 times. The record further improves when examining the data since 1950. This is the earliest year we consider to represent the beginning of the modern era. Since 1950, S&P 500 has advanced 19 out of 26 times in March following gains in January and February and was positive for the full year 25 out of 26. Average March gains in all 26 years were 1.4% while the full-year averaged 19.5%. The potential impact that President Trump could have on the domestic and global economy continues to cause uncertainty and/or concern among some investors, while encouraging others. Some individual investors view the market's upward momentum as positive. Others worry that the sharp upward run will lead to a forthcoming drop in stock prices. You can see in the quarterly chart how gold has staged a dramatic recovery after the year-end crash. Nasdaq stocks are the top performer after being the market leader since early last year. As we suggested recently, look for the leaders to perform well to provide evidence of market strength.

The CBOE Volatility Index (VIX) is known as the market’s "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. In the weekly chart below the Volatility Index continues its plunge to the lowest level in years as the major equity indexes continue achieving all-time highs. The market is becoming dangerously complacent regarding the possibility for any type of price pullback which is usually when a crash happens.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 03/01/2017. Pessimism among individual investors about the short-term direction of stock prices is at its highest level in more than four months. At the same time, optimism is near, though slightly below, its long-term average. The survey period runs from Thursday through Wednesday. Most of the votes were recorded before the Dow Jones industrial average rose above 21,000. Bullish sentiment, expectations that stock prices will rise over the next six months, declined 0.6 percentage points to 37.9%. The modest decrease follows what had been a six-week high. The historical average is 38.5%. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, fell 2.8 percentage points to 26.5%. Neutral sentiment was last lower on December 21, 2016 (26.2%). The historical average is 31.0%. Bearish sentiment, expectations that stock prices will fall over the next six months, rose 3.3 percentage points to 35.6%. Pessimism was last higher on October 19, 2016. The increase keeps bearish sentiment above its historical average of 30.5% for the sixth time in seven weeks. All three of the sentiment indicators remain well within their typical historical ranges.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers’ responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 03/01/2017. Fourth-quarter NAAIM exposure index averaged 84.15%. Last week the NAAIM exposure index was 100.83%, and the current week’s exposure is 102.07%. Last week’s analysis is still valid where we said "...The NAAIM Exposure Index rises to extremely elevated levels as the equity indexes keep continue making all-time highs. Sellers have virtually disappeared as earnings season winds down and it is reasonable to expect NAAIM exposure to remain high..." Investors continue moving funds out of other investment assets and rotating the proceeds into stocks.

Trading Strategy

Last week’s analysis mentioned "...At such frothy levels a smart move is to consider taking some profits from the recent run up or at least hedging long bullish positions. In the near term we don’t fight the trend which is our friend. Every pullback or pause should be considered an opportunity to load up on shares from your target stock list. In the graph below, defensive stocks are the leading sectors with the Energy group being the only loser..." The stock market is continuing to climb a wall of worry. Money had been sitting on the sideline for a long time and with the market in the midst of what is historically its best six months of the year, it didn’t take much to ignite a rally. Trump is getting a lot of credit for being a catalyst, but you could argue that whoever won the election, stocks were primed to take off. As seen in the S&P sector chart below what is notable is that stocks in the defensive group (on the right side of the graph) have been leading the market lately. This is indicative of the sector rotation where investors are putting funds to work in stocks they expect to benefit from a probable higher interest rate environment.

Feel free to contact me with questions,