The proportion of U.S. companies that choose to go public has been plummeting for more than two decades now, and a looming deregulation push could prompt a turnaround.

But that assumes that all IPO problems are created by red tape.

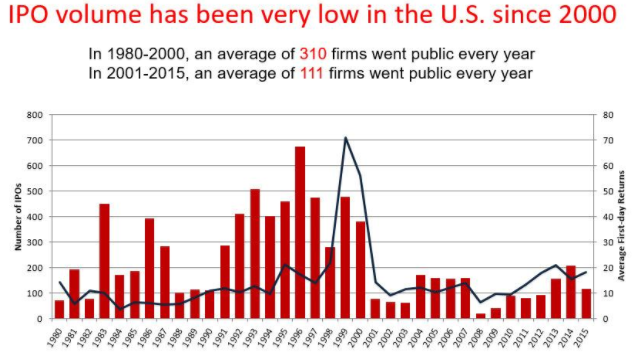

IPO volume in 2017 clocked in at a mere 181 companies. While that is a 77-percent increase compared to the previous year, it’s a far cry from the mid-1990s when 3-4 times that figure was the norm.

The number of public companies in the country has seen a dramatic decline from 7,300 during the height of the dot-com boom to just 3,671 today, mainly due to listed firms’ shrinking ranks and established firms exiting the stock market.

The IPO drought could have negative long-term implications on the economy because it undermines the notion of shareholder democracy. It means that ordinary investors are increasingly unable to own shares of companies in the fastest-growing sectors.

Two of the world's leading underwater unicorns, Uber and AirBnB, have a combined valuation of more than $100 billion--all in the hands of the founders, private equity firms and VCs.

(Click to enlarge)

Source: Kauffman

Many observers blame this unfortunate trend on red tape--increasing regulatory and disclosure costs.

Others cite the Sarbanes-Oxley Act of 2002(SOX), enacted to protect investors from possible fraudulent activities by corporations, as a possible culprit.

Assuming they are right, the IPO market could receive a much-needed shot in the arm if a recent report by the WSJ comes to fruition.

According to the report, the SEC plans to make it easier for more companies to list on the bourses by allowing them to hold private talks with investors in a bid to test appetite for their stocks before holding actual IPOs.

There's little doubt that less red tape could act as a big incentive for young startups to go public.

Related: U.S. And China To Face Off Over Aramco IPO

The regulatory landscape as it stands right now is too stodgy. Long-drawn procedures and numerous public disclosures can delay going public by years.

In a report by the White House Council of Economic Advisors, President Trump credited efforts by his administration at deregulation as a major reason why the U.S. economy exceeded growth expectations in 2017.

But putting all the blame for the sorry state of the IPO industry on SOX and red tape is missing the mark.

There are other frequently ignored factors at play here. The U.S. economy is now about knowledge and intangible investment, according to Quartz. It’s not about ‘industry’ as much, or about raising massive capital for factories and machinery. Now, twice as much money is poured into research and development as opposed to capital investments.

Public listing encompasses two main features--disclosure and accounting standards. A small startup with a highly valuable app is likely to be strong in intangible assets but won’t have much to show in terms of traditional assets. It also won’t want to share information that might benefit competitors. As such, it will struggle to pass the two key tests and qualify for the stock markets.

The other reason is simply due to the fact that private companies now have plenty of avenues through which to raise cheap capital with relative ease without all the substantial disclosure burdens.

There's plenty of money sloshing around in private equity, venture capital and, recently, ICOs (Initial Coin Offerings).

It's less risky and probably much easier to convince a VC of the value of your idea than pitching to thousands of potential investors.

The overarching takeaway is that there's much to like about the current private capital model. Removing various regulatory hurdles might help increase IPO activity, but private capital is likely to continue ruling the roost.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com: