You’re more vulnerable to fraud than your grandmother is, and you can thank the internet—at least according to a new Federal Trade Commission (FTC) report suggesting that millennials were more likely than any other age group to fall victim to fraudsters in 2017.

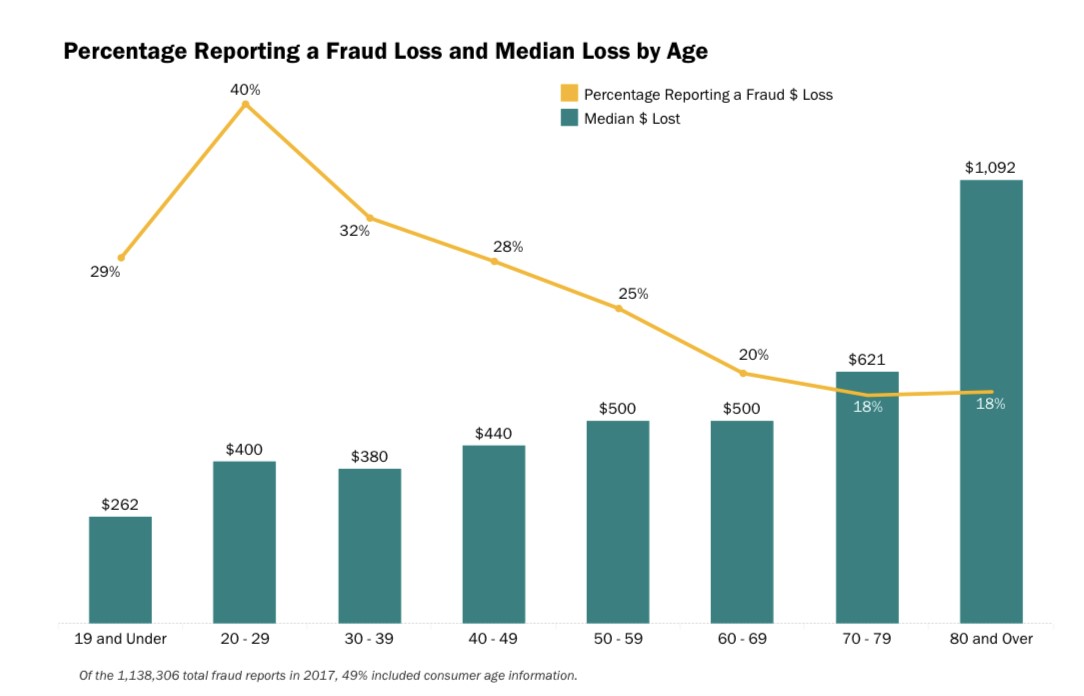

Americans aged 20 to 29 made up 40 percent of reported losses of money from fraud in 2017, compared to only 18 percent of two elderly groups combined—70-79 and 80 and over, according to the FTC report.

(Click to enlarge)

Why are millennials perfect targets? That’s simple: the Internet, the perpetual need for instant gratification, and a habit of sharing personal information online on a whim. They also aren’t as familiar with scams in general.

Older generations are much more cautious about sharing, says the FTC.

All of these factors put twentysomethings at a much higher risk level than other age groups.

The Better Business Bureau agrees, and its latest “scam risk report” identifies fake-check fraud as one of the more popular ways to get money out of millennials ages 25 to 34.

In one scenario, an apparent local business was hiring millennials to review their customer service online, paying participants small fees for small jobs, at first. Once they got hooked, they changed the parameters, asking reviewers to evaluate money-transfer businesses by cashing checks for hundreds, or even thousands of dollars, and then wiring the money back to the company.

This is where millennials get tripped up. They’re not that used to checks. There is a time lapse between when the bank can discover that a deposited check is fraudulent, and it’s a longer lapse than it takes to make a wire transfer. It’s an easy way for a fraudster to make thousands of dollars from large groups of unwitting twentysomethings. The companies collect the wires, and then cut and run.

It’s not a question of education, either. More than half of millennials who fell victim to fraud had a college degree.

It’s a question of life experience, and the digital black hole in which we live today. In fact, the all-consuming presence of the internet is the biggest reason that millennials are the juiciest prospects for fraudsters. If it’s online, it must be legit, right? No.

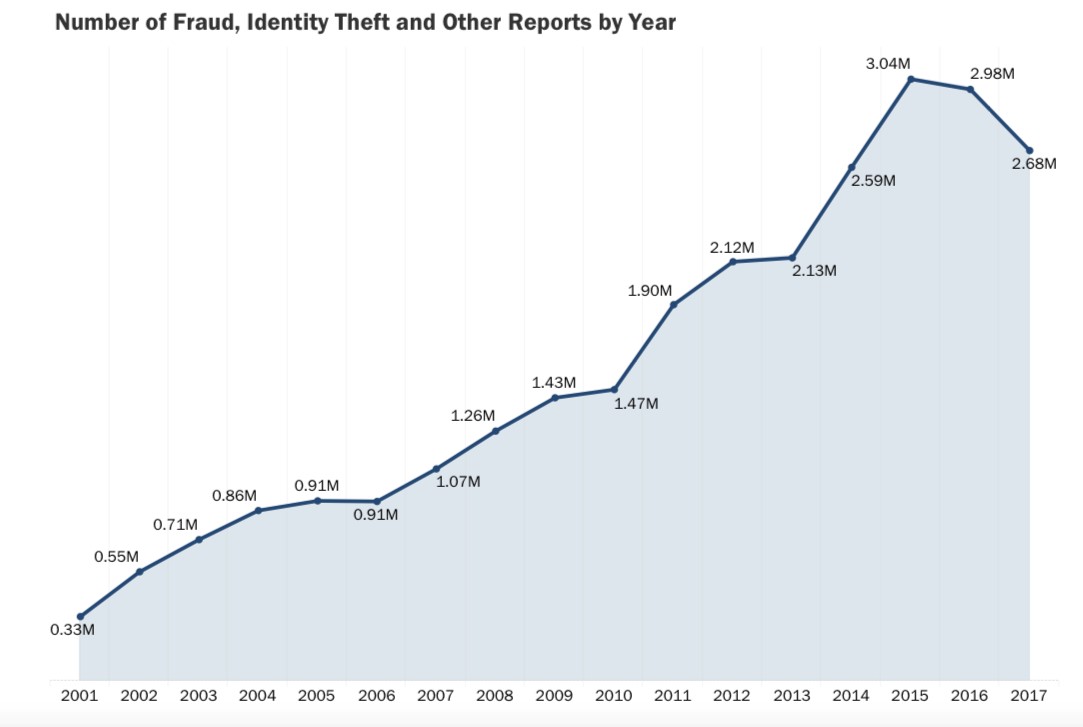

But when it comes to phone scams, older generations were more likely to fall victim to fraud, according to the FTC, which examined complaints submitted from roughly 2.68 million consumers last year, down from 2.98 million the previous year. Of those, 1.1 million were fraud; 371,000 were identity theft; and 1.2 million were categorized as “other”.

The group age that complained most frequently was between 60 and 69, representing 19 percent of the reports received in 2017. Related: U.S. Crypto Exchange Faces Insider Trading Charges

So, while millennials are more often falling victim to fraud, when they do fall, it’s not as hard as older generations. The FTC found that older age groups suffer greater total losses as victims.

The median loss for those aged 70 to 79 was $621, while the 80-and-up age group lost an average of $1,092. For millennials, losses averaged $400, for ages 20 to 29.

Annually, seniors are losing $3 billion a year to fraud, according to Consumer Reports.

Overall, the amount of money lost to fraud in 2017 is 7 percent greater than the year before, clocking in at $905 million.

While there were more than 71,000 incidents of fraud reported last year by millennials alone, 21 percent of those resulted in loss of money--a total of $61 million.

Under the identity theft category, credit card fraud represented the top scam by frequency, with complaints up 20 percent from the previous year. Coming in second was employment or tax-related fraud.

Travel- and vacation-related scams recorded an average loss of $1,710 per victim. Mortgage foreclosure relief and debt management scams netted an average of $1,200 per victim, and business and job opportunities brought in $1,063 per target, according to the FTC.

But the biggest bucks were raked in by imposter scams, where fraudsters pose as government officials, relatives or people in need. This category raked in $328 million for scammers last year—more than any other type of fraud.

(Click to enlarge)

Regardless of age group, the number of fraudsters is growing, and becoming more savvy.

By Jan Bauer for Safehaven.com

More Top Reads From Safehaven.com: