Few assets in the business world are as polarizing as cryptocurrencies are right now, and it doesn’t help when a tech monolith like Apple moves to ban all apps that facilitate crypto mining, and then Wells Fargo follows suit with a ban on credit card crypto purchases.

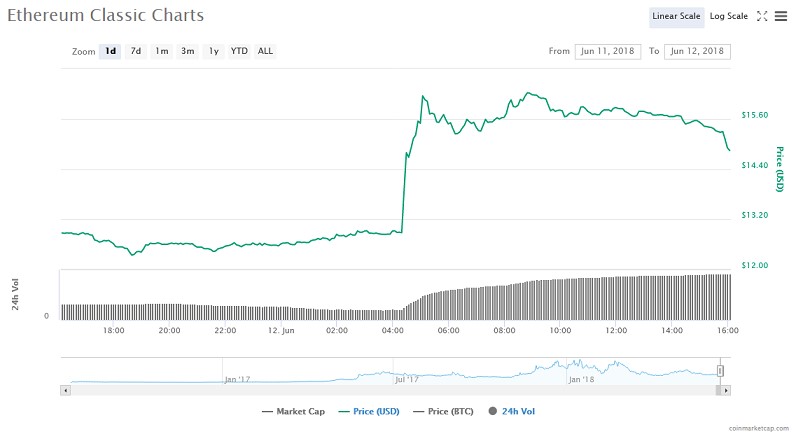

And it all comes just as the crypto community was warming up to the idea of an expanding cryptocurrency space after the announcement by giant crypto exchange Coinbase has added Ethereum Classic (ETC) to its platform.

(Click to enlarge)

Source: CoinMarketCap

The news led to a nice 25-percent spike in ETC prices, and came hot on the heels of a recent announcement by Coinbase and Circle regarding their intention to seek SEC approval.

The move by Coinbase, the fourth-largest crypto exchange, probably means that the company is now open to adding more assets to its narrow portfolio in the future.

But then suddenly, Apple and Wells Fargo have thrown a spanner in the works. The iPhone maker has just slapped a ban on cryptocurrency mining through its popular app store. Apple has updated its app developer guidelines to ban on-device cryptocurrency mining in App Store apps.

Meanwhile, Wells Fargo has announced that customers will no longer be able to purchase cryptocurrencies using its credit cards.

Wells Fargo joins a raft of other large banks including Bank of America, Citibank and J.P. Morgan which have also pulled off similar moves.

Protecting the User Experience

Apple and Wells Fargo appear to have reset the clock back to the days of the anti-crypto campaign by Facebook, Google and Twitter.

The three digital advertising companies [ in]famously banned cryptocurrency ads for ICOs and token sales on their platforms ostensibly to keep prying eyes by regulators at bay. Related: Cryptos Attempt To Claw Back Weekend Losses

Apple's crackdown on cryptocurrency mining comes a couple of months after the company pulled the popular Calendar 2 app from App Store in March after the app started mining Monero on the background on users' devices.

The company said that it removed the app from App Store because: “Apps should not rapidly drain battery, generate excessive heat, or put unnecessary strain on device resources.''

In its latest guidelines, Apple says the only crypto mining activity allowed on its devices is the off-device kind, i.e. cloud mining. It also says that virtual currency wallet apps are OK, as long as they are offered by developers enrolled as organizations.

It therefore appears as if Apple's main concern is not to deter crypto activity per se, but rather to avoid degrading the user experience. In other words, Apple is simply trying to avoid its precious devices looking bad in the eyes of users.

That’s just as well considering that Macs and iPhones lack powerful enough CPUs and GPUs to mine top-shelf cryptos like Bitcoin and Ethereum. To do that you would need a giant mobile mining rig that's powered by 40 Samsung smartphones (albeit old ones):

Protecting Consumers

In the case of Wells Fargo, the company said it deemed it necessary to take its latest step in order to be consistent with the industrywide practice and also due to the high volatility of crypto—even though that volatility is nothing like it used to be.

Wells Fargo is making sense, here.

Related: The Double-Edged Sword Of Crypto Regulation

Far too many people have been using credit cards to make Bitcoin purchases speculative and highly risky plays.

A 2017 LendEDU survey found that nearly 20 percent of users were using their credit cards to purchase Bitcoin, with a good chunk planning to pay off their balances after selling their Bitcoin investments. Although LendEDU failed to indicate whether the survey was scientifically randomized or not, the sample size is large enough to lend credibility to the findings.

Such speculative plays are worrisome because they could easily fuel a cycle of credit card defaults, with crypto exchanges like Coinbase being the only sure winners.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com: