Corporate tie-ups are all the rage right now. Global M&A activity reached an all-time high in 2017, with more than 50,000 deals worth more than $3 trillion dollars consummated, and a 2018 M&A Trends report by Deloitte predicted an acceleration in mergers and acquisitions in this year, both in deal volume and size.

So far, those projections are spot on, with global M&A exceeding a trillion dollars during the first three months of the year.

While the usual suspects including North America, Europe and Asia-Pacific continue hogging the limelight with their mega deals, one unlikely region has emerged as a hotbed of tie-ups—the Middle East.

Cross-Border M&A

The aggregate value of mergers and acquisitions in the Middle East climbed to $25.4 billion during the first half of the year compared with $15.7 billion a year ago. That’s good for a 62-percent increase, and more than three times the global growth clip.

The strong growth is mainly driven by cross-border mergers, with 65 percent of all M&A activity happening between companies in different countries.

The UAE has been seeing the lion’s share of the action, with 34 deals closed totaling $6.6 billion. Emirates NBD’s acquisition of Turkey-based $3.2-billion Denizbank in April stole the show.

Inbound deals targeting the Middle East increased at a torrid pace of 174 percent to $8.1 billion, powered by the acquisition of Abu Dhabi National Oil Company’s oil field concession by French oil giant Total and Austria’s OMG for a total of $2.6 billion. Related: Tesla Stock Stumbles On Model 3 Cancellations

Outbound deals increased at a slower but still respectable 20-percent clip to $7.6 billion. The energy and power sectors drew the most inbound merger activity with deals totaling $7.4 billion.

M&A Playbook Changing

Some of the key reasons companies are often willing to pay huge premiums to acquire other companies include:

• Gain a bigger market share

• Diversify product and service offerings

• Gain control of operational expertise including intellectual rights, patents and R&D

• Lower operational costs and financial risks

Unfortunately, the reality has hardly been utopian.

Most asset remixes in the past have failed to deliver the projected synergies and therefore failed to create sufficient shareholder value to justify their price tags. The merger graveyard is littered with the formerly Who’s Who of the corporate arena—Americas Online/Time Warner, Sprint/Nextel Communications, Google/Motorola, Microsoft/Nokia among others.

And there’s empirical evidence to back up those claims: A 2012 KPMG study found that staggering 83 percent of mergers failed to boost shareholder returns, while another by A.T. Kearney concluded that overall, M&A led to negative total returns on shareholder capital. Meanwhile, this report by Bain Capital says the chief reason why mergers fall below expectations can be pinned on the tendency by the involved parties to set highly aggressive targets in a bid to receive the backing of shareholders and financiers.

Related: Iraq Unplugged: No Internet, No Protests, No Money

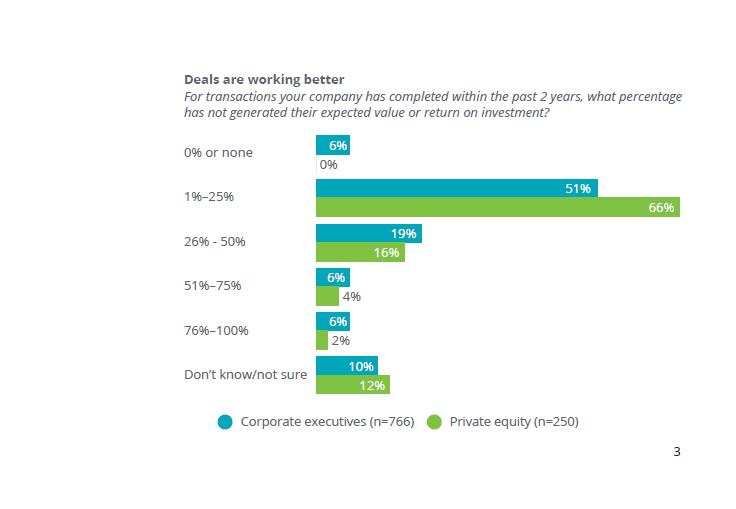

More recent studies, however, suggest that companies are increasingly becoming adept at realizing value from mergers.

Just 12 percent of company leaders now report that mergers are failing to deliver the expected return on investment--a sharp drop from nearly 40 percent reported two years ago.

(Click to enlarge)

Source: Deloitte

This is definitely a positive trend, since no investor wants their company making huge write-offs that are likely to leave them in a profit hole for years. Let’s just hope that corporate leaders and deal brokers keep their magic touch.

By Charles Benavidez for Safehaven.com

More Top Reads From Safehaven.com: