Since withdrawing its troops from Southern Lebanon six years ago, Israel has carefully watched Iranian backed Hizbollah guerillas plant landmines and booby traps along their common border, and then stockpile about 12,000 katushya rockets, with ranges up to 100 km (60 miles), aimed at Israel's northern frontier. Until July 12th, the prevailing view in Jerusalem was that Hizbollah would hold its fire, unless a wider war in the Middle East broke out over Iran's clandestine nuclear program.

However, the Middle East tinderbox was set on fire on July 12th, when Hizbollah guerillas sneaked across the border and killed eight Israeli soldiers and kidnapped two others, which Israel's prime-minister Ehud Olmert called an "act of war", and promised a "very painful and far-reaching" response. Hizbollah is the only Lebanese faction to retain its weapons after the 1975-90 civil-war, and is also a political party, with 14 members in the Beirut parliament and two cabinet ministers.

Hizbollah crossed another "red line" on July 16th with a rocket attack on Haifa, Israel's third largest city, 35 km (20 miles) south of the Lebanese border. If Hizbollah launches longer-range Iranian missiles on Tel Aviv, the commercial center, the Israeli response would be very severe.

Hizbollah crossed another "red line" on July 16th with a rocket attack on Haifa, Israel's third largest city, 35 km (20 miles) south of the Lebanese border. If Hizbollah launches longer-range Iranian missiles on Tel Aviv, the commercial center, the Israeli response would be very severe.

The next few days are most critical and a lot depends on whether Tehran decides to take a chance and authorizes Hezbollah to launch long-range missiles with more powerful warheads at Israeli cities.

Neither side has yet played its full hand. Israel did not knock out Beirut's electrical grid, as it had done in the past. Hezbollah has not yet aimed at the oil refineries and other combustible targets in the Haifa Bay area, or unleashed its longest-range rockets reportedly capable of reaching Tel Aviv. It is difficult to assess what the Iranian leadership will decide next in its war to "wipe Israel off the map."

But if Iran and Syria join the battle, world oil prices could soar, and meltdown the global stock markets.

The G-8 leaders meeting in St Petersburg, blamed Hizbollah for the flare-up of violence, and agreed that Israel had the right of self-defense. That gives Israel the green light to maintain its air, land, and sea blockade of Lebanon, to prevent further shipments of ammunition to Hizbollah. An extended blockade might also convince the Sunnis, Druze, and Christians that Hezbollah is not the protector of Lebanon from Israel, as it claims, but a terrorist proxy, operating at the behest of Iran and Syria that will bring disaster upon Lebanon's economy and infrastructure.

However, Saniora's Sunni Muslim-led government is not willing to use force against the Shiite Muslim Hezbollah guerrillas, which could trigger another bloody civil war in Lebanon. The 70,000-strong Lebanese army would break up along sectarian lines, as it did during the 1975-90 civil-war. Such an option is therefore, highly unlikely.

Fears of a Wider War in the Middle East

Very few traders took Iranian President Mahmoud Ahmadinejad seriously on July 9th, when he called for a jihad against Israel. "The basic problem in the Islamic world is the existence of the Zionist regime, and the Islamic world and the region must mobilize to remove this problem. The biggest threat today for the region is the existence of the fake Zionist regime, and it will not be long before intense Muslim fury will lead to a huge explosion," he said.

Three days later, on July 12th, Hizbollah heeded the call with a cross border raid into Israel that coincided with a deadline for Iran to respond to a UN package of carrots and sticks relating to its nuclear program. Ahmadinejad rejected the deadline in no un-certain terms on July 13th. "In the face of the venomous campaign of malicious people, we'll not step back one iota. The Iranian people are standing tall on their way to access their full rights and complete use of the nuclear fuel cycle."

The flare-up of violence distracted the Group of Eight summit of major world powers, which had planned to focus on a joint policy on Iran's nuclear program, and eventual UN Security Council sanctions, if it doesn't suspend uranium enrichment. Instead, the G-8 leaders spent much of the weekend struggling to reach a semblance of consensus on how to stop the new violence.

The flare-up of violence briefly sent US light crude oil soaring to record highs of $78.40 per barrel on July 14th, and crude oil for April 2007 delivery hit $80 per barrel. Iran's Ayatollah figures the US or Israel might someday launch a preemptive strike again his nuclear facilities. So Hezbollah's attacks might just be a sneak preview of the damage that Tehran can inflict on Israel and the global stock markets, if the UN embargos Iranian oil exports or blocks its imports of gasoline.

Fanning the flames of a wider war in the Middle East, on July 13th, Iran's Ahmadinejad warned Israel against attacking Syria, during a telephone call with President Bashar al-Assad in Damascus. "If Israel commits another act of idiocy and attacks Syria, this will be the same as an aggression against the entire Islamic world and it will receive a stinging response," he warned.

On July 16th, Hezbollah leader Sheikh Hassan Nasrallah warned that the Iranian proxy could strike almost anywhere in Israel. "We are just at the beginning. We promise them surprises in any confrontation. Hezbollah is not fighting a battle for Lebanon. We are now fighting a battle for the Islamic nation. The peoples of the Arab and Islamic world have a historic opportunity to score a defeat against the Zionist enemy. We are providing the example," Nasrallah added.

But Saudi Arabia rejected Hizbollah's call for jihad on July 14th, "there has to be a differentiation between legitimate resistance to Israel and uncalculated adventures. The kingdom sees that it is time for those elements to alone shoulder the full responsibility for this irresponsible behavior and that the burden of ending the crisis falls on them alone." With the Saudis publicly distancing themselves from Hezbollah, and Egypt and Jordan sharing similar private sentiments, the current crisis leaves Israel alone, to square off against the Hizbollah, Syrian, and Iranian axis.

The "Oil Weapon" and the Laws of Supply and Demand

Tehran has already unleashed the "Oil Weapon" this year with daily verbal jawboning threats, and without cutting back a single barrel of oil exports. On June 4th, the Ayatollah Khameinei threatened to disrupt the flow of 17 million barrels per day thru the Gulf of Hormuz, lifting crude oil above the psychological $70 per barrel area. "If the US makes a wrong move regarding Iran, definitely the energy flow in this region will be seriously endangered," Khamenei warned.

Iran's chief nuclear negotiator Ali Larjani said the US is intent on toppling Tehran's government whatever happens in talks over its nuclear plans, Britain's Guardian newspaper reported on June 23rd. "If the Americans continue on the same path, the price of oil will skyrocket and it will strengthen our resolve. They want to set fire to the region. The American strategy is to use force to secure their interests."

There is also growing demand for crude oil in China and India that keeps oil prices bubbling. China's crude oil imports for the first five months of 2006 were up 17.9% at 12.4 million tons, importing more than 40% of its crude needs. India's oil imports rose to 9 million tons or 12% higher from a year ago, and its industrial production was up 10% in May from a year earlier, bolstering its oil demand.

Also squeezing the price of crude oil higher was a report from London, that supplies of North Sea Brent that set the price for a quarter of the world's oil supply will fall to a record low of 741,000 barrels per day in August, down from 933,000 bpd in July due to maintenance on Forties fields. In Nigeria, suspected explosions at oil pipelines on July 13th heightened uncertainty over production, even as almost a quarter of oil output in that country remains shut due to attacks by militants.

In the United States, the world's largest oil consumer of 21 million bpd, the price of crude oil briefly rose to an all-time high of $78.40 per barrel in electronic trading on July 14th. The uptrend in crude oil has confounded market bears, because prices are climbing alongside a 25% increase in US commercial oil stocks from two years, to an eight year high of 347 million barrels in June. In the past two weeks however, US crude oil stocks fell 3% or 11 million barrels to 336 million barrels.

US oil companies are hoarding oil supplies, in case Iran withholds crude-oil exports or targets oil tankers in the Persian Gulf. Iraq is falling into a civil war and its daily oil output of 2.4 million bpd is unstable. And now China has just completed oil storage tanks in Zhejiang, Shandong and Liaoning, with capacity to hold up to 88 million barrels, and is planning a third phase of yet another 200 million barrels of storage, to be completed by 2008.

The nightmare scenario of $100 per barrel is a possibility, but mitigating the odds are total government and industry stocks of crude oil and refined products held by member states of the OECD, that amount to about 4 billion barrels. If markets do not settle down from a possible cut-off in Iranian supply, there are reserves available to cover the Iranian shortfall for several years. And without its $54 billion of annual oil sales, Iran's economy could collapse and topple the Ayatollah's regime.

Mid-East Oil Shock Rattles Dow Jones Industrials

One year ago, with crude oil trading at $62 /barrel, former Fed chief "Easy" Al Greenspan was marveling at the strength of the US economy and the stock market, in defiance of record high oil prices. "The increase in oil prices since the end of 2003 probably shaved roughly 0.50% off of real GDP growth last year, and they look to restrain growth this year by approximately 0.75%. Aside from these headwinds, the US economy seems to be coping pretty well with the run-up in crude oil prices."

But eleven months later, on June 7th, Greenspan offered a grim view of the world's vulnerability to crude oil prices above $70 per barrel. "The energy abundance on which this nation was built is over. While the world economy had largely shrugged off sharp oil price gains so far, the immunity of US consumers may be running out. The US especially, has been able to absorb the huge implicit tax of rising oil prices so far. However, recent data indicate we may finally be experiencing some impact."

Greenspan said the buffer between oil supply and demand was razor thin and that oil price spikes remained a risk. "Even small acts of sabotage or local insurrection have a significant impact on oil prices." He added that a big oil price rise could spur "a significant contraction in the economy," but said he could not predict what size increase it would take to do such damage.

In retrospect, the surge in oil prices above $70 per barrel was the trigger point that derailed the 3-year Dow Jones Industrials rally. For the eternal optimists on Wall Street, the bargain hunters who dive into the market to buy badly stocks after any big sell-off, the latest oil price shock is no fluke and much higher energy prices could lie on the horizon, if the Ayatollah shuts down the Strait of Hormuz.

Before that happens however, schizophrenic US hedge fund traders, whose firepower rocks markets at a moment's notice, will focus on Fed chief Ben Bernanke's testimony before Congress on July 19th. Bernanke has zig-zagged a few times in the past three months, between calls for a pause, then calls for rate hikes, to confront inflation pressures. After the latest downturn in the US stock markets, the odds in the fed funds futures market are 50-50 for a rate pause in August.

European Central Banks Shaken by Middle-East Oil Shock

Just when Europe's largest economy was gaining upward momentum after 3-years of flirting with recessions, the Middle-East oil shock threatens to derail Germany's long awaited recovery. German factory orders jumped 17.3% from a year earlier in May, the biggest increase since 2000. The Munich-based Ifo institute raised its 2006 growth forecast for the German economy to 1.8% and the business confidence index unexpectedly surged to a 15-year high.

Germany's $2.6 trillion economy and the DAX-30 blue-chips have depended on foreign sales over the past four years for growth, as job cuts at home and a surge in oil prices eroded households' purchasing power. About one third of Germany's overall economy is linked to exports, which were booming in April and May at an average of 73 billion Euros, but are at risk from any global economic downturn.

The first oil shock in early April to as high as 61 Euros /barrel, flattened the high-flying German DAX-30 index, which was racking up a 42% gain from a year earlier, fueled by merger and takeover mania in Europe. But the first spike in oil prices to 61 Euros per barrel also began to show up in the German producer price index, which jumped 0.6% in April, to an annualized 6.2%, its highest rate in 24-years.

The Middle-East oil spike to 61 Euros per barrel on July 14th, also derailed a German DAX's recovery at the 5700-level, and overshadowed bullish news that Germany exported a near-record 72.6 billion Euros in May. Germany is the world's fourth largest oil importer of 2.4 million bpd of oil, with the largest source of crude oil imports from Russia, Norway, and the United Kingdom.

The sharp rise in world oil prices presents a big dilemma for the European Central Bank, which is inflating the Euro M3 money supply at an annualized 8.9% clip, to cushion the European stock markets from the rising costs of energy. The ECB's strategy is beginning to backfire, with European headline inflation rates creeping higher, due to the rising cost of oil and its secondary knock-on effects.

On June 15th, the Bank of Spain's chief Jaime Caruana broke ranks with ECB chief Jean Trichet, and called for a tighter ECB monetary policy to combat the rising cost of energy and other commodities. "The world economy has so far absorbed rising commodity prices well, but the upwards trend is a major risk to the world economy," declared Bank of Spain chief Jaime Caruana on June 15th. "This trend constitutes a risk of the first order to which monetary policy must remain vigilant."

On July 12th, Jean "Tricky" Trichet agreed that high oil and commodity prices demanded closer attention, and should not be ignored when measuring true inflation levels in the Euro zone. "The phenomenon we are observing is very important and we have to understand it. We are in some kind of supply shock, but also very much a demand shock with the emergence of new economic giants, (China, India)," he said.

Trichet then criticized the narrow focus on measures such as "core" consumer price inflation, which exclude rising energy costs but factor in the falling cost of manufactured goods. That would represent a 180 degree change in "Tricky" Trichet's view of inflation. But Trichet is still dragging his heels, and the ECB's three-quarter point rate hikes to 2.75% so far since December, have not kept pace with a 1.5% surge in the Euro zone producer inflation to 6.0 percent.

So on the surface, the ECB is raising nominal interest rates, but behind the "smoke and mirrors" the ECB's repo rate, adjusted for producer price inflation, is actually lower this year, at a negative 3.25 percent. An August rate hike to 3.00% would still leave the ECB far behind the inflation curve, especially during a Middle-East oil shock period. But then again, the ECB is also aiming to cushion European stock markets.

Bank of England Monetizing Oil prices

The Bank of England, has been conspicuously absent from the G-10's monetary tightening campaign this year, Instead, the BOE is quietly inflating the British M4 money supply at an annualized rate of 11.7%, twice the growth rate from three years ago, to insulate the British stock market from the shock of escalating oil prices. England finds itself today with crude oil prices at 42 pounds per barrel, up 133% from three years ago, yet the BOE has no intention of raising rates anytime soon.

The BOE is defending the UK housing market, as British mortgage debt exceeds a trillion pounds for the first time in May, underlining the economy's vulnerability to any downturn in the housing market. Outstanding mortgage debt hit 1.06 trillion pounds in May as net lending surged by 9.3 billion pounds, the biggest monthly gain for 2-½ years. British consumers could find it increasingly difficult to stay on top of their debts if rates rise, so the BOE is printing more pounds to keep rates low.

Bank of Japan Tightening despite Oil Shocks

The Bank of Japan's five-year, ultra-easy money policy was widely cited as a primary contributor to the bullish trend in global commodities, including copper, crude oil, silver, and zinc, over the past four years. The BOJ's ultra-easy money policy boomeranged with higher energy and metals costs, pushing Japan's producer price index up 3.3% in May from the same period a year earlier, its fastest in 25 years.

According to the Bank of Int'l Settlements, in the seven quarters to the end of 2005, "yen carry" trades surged by $161 billion, with three quarters of this lending channeled to international financial centers such as the United Kingdom, Singapore, and the Cayman Islands, a favorite haven for hedge funds. Traders could borrow funds in Japan at zero percent to finance positions in commodities, while the Japanese ministry of finance was intervening or jawboning the yen lower.

Rising Japanese producer prices are a concern to the BOJ because they slow corporate profit growth, and add pressure on factories to pass along higher input prices to consumers. Tokyo says that "core" consumer prices are rising at a slower 0.6% rate in May, and that suggests that middleman profit margins are getting squeezed. Indeed, Japan's corporate profit growth slowed to 4.1% in the first quarter, less than half the 11% in the fourth quarter.

Partly in response to soaring gold and commodity prices, the Bank of Japan announced the end of its radical "quantitative easing" policy on March 9th, and has drained 22.7 trillion yen out of the banking system since March 9th. Japan's monetary base, which includes yen in circulation plus bank deposits, fell to 91.4 trillion yen last month. The BOJ also hiked its key overnight rate by 0.25% from zero percent on July 14th, but added, "an accommodative monetary environment ensuing from very low interest rates will probably be maintained for some time.

But while the baby-step rate hike to 0.25% is a noteworthy event, it's just part of a game of "smoke and mirrors". After the dust finally settles, Japan's overnight loan rate is pegged at 3% below its producer price inflation rate. While the BOJ is tightening liquidity in a big way in the $4.5 trillion economy, a 0.25% overnight loan is still abnormally low, and is not likely to put a meaningful roadblock in front of "yen carry" traders betting on the long side of the "Commodity Super Cycle".

The BOJ is still under enormous pressure from the finance ministry to keep its overnight interest rates close to zero percent. Tokyo has 774 trillion yen ($6.7 trillion) of outstanding debt, and doesn't want to pay a higher cost of servicing the debt. Finance Minister Sadakazu Tanigaki said on July 11th, "It is desirable to have zero interest rates to support the economy when there are no worries about inflation. The BOJ needs to watch markets and the underlying economic conditions," he said.

With Japan's Nikkei-225 stock index is starting to wilt under slowing profit growth and soaring oil prices to a record 9,000 yen per barrel on July 14th, it's a good bet that the BOJ would remained sidelines for the next few months. Japan contains almost no oil reserves of its own (59 million barrels of proven oil reserves), but it is the world's third largest oil consumer, after the US and China. Japan consumes an estimated 5.35 million barrels per day. Yet by leaving the overnight loan rate pegged at 0.25%, the BOJ hopes the cushion the Nikkei-225 from high oil prices.

Gold Shines as a Hedge against Inflation

Gold emerged as a big winner from the chaos in the Middle East, and the inflationary consequences of spiraling crude oil prices. Last week, the yellow metal defied a firmer US dollar and a plunge in global stock markets, and instead tracked crude oil. Traders feared the conflict in the Middle East could spread to include Iran and Syria and roil a region that supplies almost a third of the world's crude oil.

Most interestingly, the tight correlation between gold prices and the direction of global stock markets was broken in the past five days, as gold rose 8% towards $675 per ounce, while Morgan Stanley's World Index fell 3.3% to a three-week low. The MSCI World index measures blue chip stocks of 23 developed economies that account for 86% of the world economic output.

Since September 2005, gold and global stock markets were moving in lockstep. After-all, the direction of global stock markets can give real-time clues about the health of the global economy, the demand for commodities, and global inflation pressures. With gold recovering two-thirds of its losses from May 11th, the big-3 central banks face a quagmire of falling stock markets and rising gold prices, or the nightmare scenario called "Stagflation."

Also boosting gold was a report that China's foreign exchange reserves, the world's largest, rose by $56.2 billion in the first quarter and $66 billion in the second quarter 2006 to a record $941.1 billion. In all of 2005, they swelled by $209 billion. China's FX reserves have ballooned as the central bank prints yuan in exchange for foreign currency flowing into the country, in order to hold down the yuan exchange rate.

But the flood of FX reserves is making it hard for the Chinese central bank to keep the money supply under control. Beijing issues treasury bills to drain the excess cash, but must pay interest on the debt. Meanwhile, Yu Yongding, who advises the People's Bank of China, wants to use the foreign-currency reserves, to buy gold and crude oil as a hedge against inflation and the eventual devaluation of the US dollar against the yuan. The PBOC has only 1% of its reserves in gold.

Tel-Aviv Stock Exchange under Attack

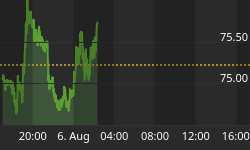

Not surprisingly, the Tel-Aviv-25 stock index took it on the chin last week, after Israel suddenly found itself in a new war with Iran's Hizbollah in Lebanon. The TA-25 tumbled 10% in three days, amid worries that prolonged fighting would force the Treasury to run a bigger budget deficit, driving up long term Israeli bond yields. Israel's economy grew by an impressive 6.6% in the first quarter, but could get hurt by soaring crude oil prices and rate hikes in Japan and Europe.

At its worst level on July 17th at the 720-level, the TA-25 was off 20% from its all-time high of 900 set in early May. After a reversal bottom pattern set on July 17th to the 770-level, the TA-25 was back in perfect alignment with Morgan Stanley's emerging market index. The reversal bottom for the TA-25 was based on speculation that the battle with Hizbollah would not spread to Syria or Iran.

Israelis are resilient and accustomed to fighting wars with their Arab neighbors every few years, in addition to the daily battles with Hamas and Islamic Jihad. Yet the Israeli economy grew 4.3% in 2004 and 5.2% in 2005, and is expected to grow 5% in 2006. Until May 11th, the TA-25 had tripled in value from three years ago, far outpacing stock markets in developed countries. Israel attracted a record $9.7 billion of foreign investment last year, and is on course to raise $1.6 in venture capital for its high-tech industries in 2006.

Twelve business groups control 60% of the aggregate market value of all Israeli public companies (when Teva Pharmaceutical Industries is excluded), with shares valued at $44 billion. The groups achieved their control through descending layers of ownership. These types of organizations were eliminated in the US in the 1930's, through a series of restrictions on ownership, as well as double taxation of dividends paid by a company to its parent organization.

As for the future of the TA-25, Israeli traders are already looking beyond the skirmish in Lebanon and focusing on fundamentals, such as interest rates, oil prices, earnings, and the direction of other emerging stock markets. Israel's military said it destroyed 30% of Hizbollahs's weaponry so far, and expects to knock out the remainder by next week, leading to the departure of Sheik Nasrallah from Lebanon.

Beirut Stock Exchange Locked Limit down

Lebanon's stock market did not open on July 17th, after tumbling 14% last week, after the Israeli blockade closed down the Lebanese economy and all its foreign trade. Lebanese Finance Minister Jihad Azour explained the market would be closed for security reasons, though trading would continue in the Lebanese pound. On the currency front, big investors are converting to the US dollar from the Lebanese pound, but so far, there has been no major flight of capital.

Azour said the central bank has around $13 billion in gross foreign currency reserves, more than enough resources to defend the pound. However, if the Israeli blockade is prolonged for several months, the central bank might run out of cash, raising doubts about its ability to service Lebanon's huge foreign debt burden. That in turn, could sink the pound, trigger higher inflation and higher interest rates, and crush the Beirut stock market when it dares to re-open for trading.

Meanwhile, the Lebanese economy will suffer from the attacks on infrastructure. Booming tourism has played an important part in Lebanon's economic recovery, with the bulk of its tourists from the Persian Gulf region. But the severity of the current disruption will depend on how long the Israeli attacks continue and how long it takes for damage to be repaired, all of which is currently uncertain. Israel has threatened to destroy Lebanon's electricity grid, if Iran's Hizbollah fires upon Tel-Aviv.

Istanbul swept lower by Regional contagion

The main Turkish share index, the Istanbul-100 fell as much as 4.8% on July 17th, while the lira and Turkish bonds weakened with losses in other foreign markets. Violence between Turkey's southern neighbors in Israel and Lebanon has escalated, increasing investors' fears that the situation could erupt into regional violence. Tourism to Turkey was already 16.7% lower in May from a year earlier.

The Turkish stock market was hammered in the global emerging stock market meltdown between May 11th to June 13th. The lira tumbled by 25%, forcing the central bank to hike its overnight lending rate in rapid succession by 425 basis points to 22.25%. The weaker lira is expected to lift Turkey's 10.1% inflation rate in the months ahead, and put a strangle hold on the Turkish stock market.

Turkey's current account deficit rose 73.8% year-on-year to $4 billion in May, and for the first five months of the year, the deficit stood at $16.5 billion, compared with a deficit of $11.2 billion in the same period a year earlier. Turkey revised its official estimate of the deficit to 7% of gross national product from an original 5.8 percent. Turkish GNP is projected at $381 billion in 2006.

Turkish oil demand is around 685,000 barrels per day, and 90% of Turkey's oil supplies are imported, mainly from Saudi Arabia, Iran, Iraq, Syria and Russia. Turkey's port of Ceyhan is a major outlet for Iraqi oil exports, with optimal pipeline capacity from Iraq of 1.6 million bpd. But higher oil prices can widen Turkey's trade deficit which mushroomed 36% to $21.6 billion in first five months of 2006, from the same period a year ago.

With the flare-up of violence in the Middle-East and surge in crude oil prices to $78 /barrel, there are doubts about Turkey's ability to attract enough money from abroad to cover its external deficit. In an attempt to stop the capital flight, Turkey will scrap a 15% withholding tax on non-residents investing in financial instruments, said Finance Minister Kemal Unakitan on June 22nd. The withholding tax for Turkish residents investing in shares and bonds will fall to 10% from 15 percent.

To Subscribe to the Global Money Trends newsletter, Please click on the hyperlink below to place an order now. http://www.sirchartsalot.com/newsletters.php

This article may be re-printed with links to www.sirchartsalot.com.

Here's what you receive for a subscription to the Global Money Trends newsletter

1- Insightful analysis and predictions for a dozen of the most influential stock markets around the world including, the global benchmark S&P 500 index and Dow Jones Industrials, the Toronto Stock Exchange, Brazil's Bovespa, Japan's Nikkei-225, South Korea's Kospi, mainland China's H-share index in Hong Kong, Australian Stock Exchange, Russia's Trading System Index, India's Sensex index, the German DAX-30, and the UK's FTSE-100 index.

2- Actionable trading ideas for their US-listed Exchange Traded Funds, (ETF's) such as the Morgan Stanley International funds, and other closed-end country funds.

3- Analysis and bold predictions for key commodities such as crude oil, copper, gold, the CRB index, and related mining and oil company indexes. Foreign currencies such as, the Australian dollar, British pound, Euro, Japanese yen, Canadian dollar, New Zealand dollar, and South African rand. Libor interest rates and 10-year bond yields in Australia, Canada, Europe, Great Britain, Japan, and the United States, and their underlying monetary policies.