Do you remember the amazing days of the tech-stock mania of late 1999 and early 2000? Boy I sure do!

I have been interested in the stock markets almost my entire life. When I was a young kid around 12 or 13 years old my wonderful father helped me make my first purchase of common stock. Ever since then I have had a strong passion for the markets, which I find perpetually intriguing and exciting.

Since it would probably take me a hundred lifetimes to even start to truly fully understand the markets, I have also always been an eager student of market history. Market history really fascinates me not only because it is interesting and colorful reading, but because we have a magnificent opportunity right now today to learn from the countless mistakes made by past generations.

If we can learn and understand how investors and speculators just like us won and lost vast amounts of capital throughout history, then we can diligently strive to emulate their successes and zealously avoid remaking their deadly mistakes. Personally I find it far more profitable and much less painful to learn from the mistakes of other folks in history rather than getting blasted myself in today's versions of the same old historical market minefields!

Before 1999, I had read and read and read about historical market bubbles with great wonder but had never experienced one firsthand myself until the recent mania that capped last millennium. They are truly rare once-in-a-lifetime experiences, generally only cropping up once per Kondratieff Wave, roughly 60 years, in any given nation.

In the mid-1990s I regretted not paying closer attention to the Japanese bubble, as I haven't traded in the Japanese stock markets, but only a few years later I was blessed to experience an American bubble of our very own. I have no doubts that this phenomenal experience will be one of the highlights of my lifetime as an investor and speculator.

Just like all the dusty old tomes on historical bubbles that I had read had prophesied, the NASDAQ bubble swirled around a speculative mania. There is always speculation, a great thing that helps spread risk around to those most willing and able to accept it, but in a speculative mania the intoxicating allure of speculation seduces an entire culture. In a mania practically everyone tries to be a speculator!

You certainly share the same fresh memories of this fantastic "New Era" as I do! Remember folks thinking that 75%+ annual gains were normal? Remember when every conversation with everyone ultimately led to the markets and the killings to be made in tech stocks? Remember when ANYNAME.COM was enough to lead to a feeding frenzy in any unknown and unproven company with no profits? What a wild and crazy moment in history!

While investors are concerned about fundamentals, speculators truly could not care less. Speculators will buy anything if they think its price is going higher and they usually remain totally unconcerned about actual quality and underlying value. When this mindset infects an entire culture, a rare event that only happens once every three generations or so, prices are bid up so far into the stratosphere beyond fundamental foundations that it is breathtaking.

As I was blessed to have my book knowledge on historical bubbles augmented with the awesome real-world experiences of the NASDAQ bubble, my overall understanding of this bubble phenomenon greatly deepened. Today's NASDAQ scene intriguingly reminds me much of the NASDAQ 2000 bubble days. We certainly don't have a full-blown popular mania-driven tech bubble again today and won't for 60 years or so if history proves to be a valid guide, but it sure looks like a miniature NASDAQ Echo Bubble is brewing.

An echo bubble? Like a sonic echo returning much weaker after bouncing off of a canyon wall, an echo bubble is a miniature-scale replay of a real bubble returning after the real thing fails. An echo bubble is like a relatively small speculative mania in the same sectors most affected by the preceding historical bubble mania. As I think you will agree after you see the evidence in this essay, there is really no better way to describe current NASDAQ behavior than a curious echo bubble.

In today's odd NASDAQ Echo Bubble, the technical price action fueled by aggressive speculation is excellent and exciting, but the rally's fundamental valuation core is rotten just like the NASDAQ 2000 bubble. Speculative manias and mini speculative manias are certainly powerful and must be respected, but sentiment can only carry a market so far. Eventually red-hot pure emotion, basically unbridled greed, cools, and if the necessary supporting fundamentals aren't there after the sentiment dust settles the mania suddenly vaporizes and the markets plunge.

It's kind of funny that virtually everyone has been forced to accept that the so-called "New Era" of 2000 was really just a garden-variety bubble, a speculative mania focused on tech stocks. Back in 2000 when I was writing essays on this very topic I used to be constantly flamed and ridiculed for calling the NASDAQ scene a bubble, but now it is just accepted truth. Our first chart illustrates why this bubble thesis is unassailable.

This graph simply compares the NASDAQ 2000 bubble and years since with the notorious Dow 30 bubble of 1929 and its resulting Great Bear bust. We ran the original iteration of this chart way back in August 2000 in "To Crash or Not to Crash" when I brazenly forecast that "…the probabilities continue to increase that April was a classical index crash and a demoralizing NASDAQ bear market lies dead ahead…"

Incidentally, if you'd like to study a larger and far-more detailed version of this graph, we finally updated our big-huge version which is freely available at www.zealllc.com/2002/1929.htm . While it was once only the realm of outcast financial heretics to dare label the NASDAQ a bubble and bust, it is now an unquestioned fact carved in stone in market history.

The fantastic technical symmetry inherent in this DJIA 1929 and NASDAQ 2000 comparison is magnificent! In both cases huge stock-market gains spawned booms, which led to popular speculative manias culminating in bubbles. Every investor and speculator on Earth today is so incredibly blessed to have been granted the privilege of witnessing one of these near-mythical beasts firsthand!

In both of these cases, for no readily apparent reason at the time, the speculators suddenly woke up one morning and realized that the indices were far beyond what fundamentals could support and they started selling. The bubbles burst in initial crashes. While the crashes seemed painful at the time, they were really only a small taste of things to come in the subsequent brutal bust periods.

During busts, the sole mission of the unleashed Great Bears is to ruthlessly obliterate the remaining vestiges of the preceding speculative mania without mercy. Ultimately the bubble index is ground into powder and slammed down into the underworld of undervaluation and a whole generation of wanna-be speculators is totally demoralized. Busts are wickedly ugly and nasty times in the markets!

The whole key to this entire Boom Bubble Burst Bust phenomenon is valuations. During booms valuations grow rich and during bubbles they explode into the realm of the truly absurd. During busts valuations implode and head back down through fair value towards undervalued levels. The seeds for the next boom are only sown after the Great Bear extracts enough speculator blood to leave the markets battered, popularly loathed, and undervalued.

Amazingly, even though valuation is one of the most important concepts for all investors to understand, only a relatively small fraction, the contrarians, really pay attention. If you are new to the world of valuation yourself, you may wish to skim a few of my past essays that go into much greater depth on this crucial subject.

These essays include "Long Valuation Waves", "Valuation Wave Reversion", "Dividend Valuation Waves", and "Valuation Wave Reversion 2". We also have over a century's worth of valuation charts published at www.zealllc.com/charts/valuation.htm . If you don't understand valuation, then you can't understand bubbles, and if you can't understand bubbles they will crush you like a fly just as they have so many countless other naïve investors throughout history!

The chart above illustrates the intimate ties between historical speculative manias and valuations. For both the NASDAQ and Dow 30 above, general-market S&P P/E ratios and dividend yields are shown. We use general-market valuation metrics because speculative manias are a broad phenomenon dramatically affecting the entire market as a whole, not just the narrow sector like technology in which most of the speculative fervor happens to be concentrated.

As 1929 rolled in the US markets were booming and traded at a very expensive P/E ratio of 25x earnings, well above the historical 14x fair-value average. At the bubble top later that year, the general-market P/E soared to 33x earnings, eclipsing the official bubble-territory mark of 28x. Then, as you can see above, in each subsequent year valuations dropped during the bust as the Great Bear did its thing. The US markets ultimately bottomed in 1932 under 6x earnings, horrendously undervalued.

This classical 1929 boom bubble burst bust, certainly the most famous in history until 2000, dramatically illustrates the valuation nature of the whole bubble process. As a bubble festers, speculators drive up stock prices far too high relative to the power of their underlying companies to actually earn profits in their businesses and pay dividends to their owners. Speculators collectively spawn a giant disconnect between stock prices and underlying fundamental reality, and such bubblicious environments can never last for long before fundamental gravity catches up.

Now compare this 1929 experience with the NASDAQ 2000 bubble. General-market valuations were extremely high following a stock boom. In early 2000 the boom exploded into one of the greatest popular stock manias in history as stocks shot ballistic. General-market P/Es soared above 44x earnings, a new high-water mark in history, and NASDAQ-specific P/Es hit the moon trading at well over 100x earnings!

The NASDAQ 2000 bubble was ultimately unsustainable of course. Speculators eventually had to face the cold, hard reality that stock prices were so far ahead of corporate earnings fundamentals that it was insane, and the NASDAQ bubble burst and crashed.

If you carefully examine the general-market valuation numbers (red) and NASDAQ-specific (yellow) in the chart above, you will note this valuation phenomenon. As the Great Bear bust ground down stock prices back towards underlying fundamental realities, valuations have fallen just as in all the other major bubbles in history. The NASDAQ itself has gone from well over 100x earnings, where it would take an entire century just for NASDAQ companies to merely earn back the steep prices investors paid for them, back down to 34x earnings at the beginning of 2003.

So far so good right? Valuations grew far too outrageous in 2000 due to popular naked speculation, prices crashed, valuations fell, and all is well now. Right? Unfortunately this hypothesis, incidentally the very one the bulls are leaning on today, is fatally flawed. Prices have indeed plunged, but valuations have not yet fallen anywhere near far enough and are still extremely overvalued! No Great Bear in history has ever fully retreated after a major bubble until stocks are actually undervalued, and this one almost certainly won't either.

Enter the NASDAQ Echo Bubble.

Booms, bubbles, bursts, and busts are caused by a fundamental disconnect between stock prices and valuations spawned by rare once-in-three-generation speculative manias. A post-bubble bust cannot and will not end until valuations are once again undervalued by historical standards.

While today the bulls believe that we have witnessed The Ultimate Bottom of the NASDAQ Great Bear back in October, they are dangerously ignoring all of the bubble wisdom and experience of history. Valuations remain staggeringly high, even during the recent October and March market lows. If you read about any major historical bubble in history, you will soon learn that the mere idea of a Great Bear bust ending before valuations are undervalued again and speculative excess is completely wiped out is laughable and foolish.

Our second graph this week shows our NASDAQ Echo Bubble in this crucial valuation context. The recent rally has indeed been powerful, but since it erupted from extremely high valuations, both in general-market and NASDAQ-specific P/E terms, it looks like an echo bubble. A true secular bull market like the one that launched in 1982 can only be born in undervalued markets. The NASDAQ Echo Bubble, however, was born in radically overvalued markets and it won't survive.

The NASDAQ is up an impressive 38% from its March lows and an incredible 58% from its October lows, so its recent pure-technical-price action is awesome. But unfortunately as this valuation data reveals, there is simply no fundamental foundation to this powerful bear-market rally. Like the 35%, 25%, 41%, 45%, and 34% major bear-market rallies since 2000 before it, this 38% specimen today is built on a weak foundation of speculative sand and will fail.

I am convinced, in light of today's extremely high valuations, that this recent NASDAQ action we have seen will be judged by history to be a NASDAQ Echo Bubble, a wickedly devious Great Bear trap designed to gut the still greedy perma-bulls like fish one last time before the bust continues. The Great Bear is sucking in the bulls in anticipation of gleefully flaying them alive!

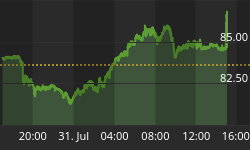

This short-term chart of the last year or so of NASDAQ action is certainly technically impressive. If you simply look at prices alone the short-term uptrend is unmistakable and it is easy to see why folks are so excited about this rally. In addition, the NASDAQ's 50dma has forged far above its 200dma, a generally bullish technical omen. Yet, while technical analysis is an extremely important tool, it is impossible to analyze a post-bubble environment successfully without being aware of current valuations. Yes, fundamentals matter!

There are three separate sets of valuation numbers shown above, all of which we calculate at Zeal from the ground up each month-end using data from the individual companies in the indices. The top blue number is the NASDAQ 100 P/E ratio, a simple average of the individual P/Es of all the companies in the NASDAQ 100 actually earning money. The total market capitalization of the NASDAQ 100 generally runs 60% or more of the total market cap of the NASDAQ Composite, so it is a great proxy for a NASDAQ P/E.

The yellow number is the market-capitalization-weighted-average (MCWA) P/E ratio of the NASDAQ 100, a much better measure. This MCWA weighting ensures that tiny companies with ludicrous P/Es don't excessively skew this valuation metric too far from representative reality. Large companies like Microsoft and Intel are given large weights proportional to their hefty market caps, while small companies trading at hundreds of times earnings are only given small weights. MCWA P/Es are explained in more depth at www.zealllc.com/faq/page3.htm .

The third red set of numbers, and in my opinion the most important, is the MCWA P/E and MCWA dividend yield of the S&P 500, or the general US stock market. While the argument can be advanced that NASDAQ companies may deserve higher than historical average P/E ratios while they are growing fast, there has never been a post-bubble Great Bear bust in history where general-market valuations haven't fallen well under fair-value, or 14x earnings.

One way or another, before this Great Bear ends, the S&P 500 will trade under 14x earnings and yield over 6% in dividends and will be undervalued by historical standards. Mark my words on this! Either stock prices will plunge dramatically in the next couple of years to get valuations back in line, or stock prices will trade sideways for a decade or more until earnings catch up. There will be no new Great Bull until stocks are really undervalued, period.

All these monthly valuation metrics really unmask the recent NASDAQ rally's true character of being an echo bubble. Yes, the pure technical price action is great, but by any valuation measure the NASDAQ rally erupted out of very high valuations in both October and March and as it marches higher valuations are growing ever more extreme and unsustainable by the month!

Just as the DJIA 1929 and NASDAQ 2000 bubbles were marked by a speculative-mania-driven disconnect between stock prices and underlying fundamental corporate earnings power, so is this festering NASDAQ Echo Bubble we are witnessing today. While short-term speculators ready to sell at a moment's notice can certainly ride foundationless rallies like this one, any long-term investors buying into this echo bubble today are committing financial suicide. This will collapse just like the real bubble before it did in 2000!

All throughout market history, real sustainable bull markets only gallop when they are launched from historically low valuations. Betting on high-valuation stocks before the grisly aftermath of a supercycle bubble bust fully runs its course is a recipe for disaster. Speculative manias, or mini ones like our echo bubble today, can run for awhile, but eventually fundamental gravity catches up and utterly crushes the mania.

If you are also interested in valuations, and in monitoring the great historical valuation waves that really drive long-term stock-market action, we painstakingly calculate the elite Big Three US index valuations each month and publish the numbers in our acclaimed Zeal Intelligence monthly newsletter.

My goal for this ritual is to ensure that neither we nor our subscribers make the disastrous mistake of deploying long-term stock-market investments before the weight of history suggests this Great Bear will really end at horrific undervaluations. All long-term investors should always know where general market valuations stand!

The bottom line on the recent NASDAQ rally, while no doubt impressive, is that the technical price action is not at all supported by fundamental improvements in valuation levels. The long-term viability of a post-bubble rally erupting above expensive P/E levels greater than 21x earnings is effectively zero. Like the five major NASDAQ bear rallies before today's 38% one, which together averaged 36%, this NASDAQ Echo Bubble will also fail.

Real bull markets are born from the desolate ashes of undervaluation, not from the fiery embers of a mini speculative mania! While gunslinging speculators can enjoy this waning party, long-term tech investors with crucial capital risked in still chronically overvalued tech stocks should follow the tech corporate insiders' lead and aggressively sell now and get out of Dodge.

The NASDAQ Echo Bubble day of reckoning is coming, and it won't be pretty! The brilliant men who wrote those dusty old history books on bubbles will be proven right yet again.