The market's rally in the past few days has been brought to us courtesy of the super bearish sentiment that showed up in the AAII investor sentiment poll of last week, which showed a whopping 57% of investors had turned bearish compared to only 28% bullish. That much disparity in favor of the bears was sure to produce a rally as we talked about earlier and the banks were among the beneficiaries of the rally as expected. (As we write this the percentage of bears has backed off a bit but is still quite high at 43%. Meanwhile the bulls gained some and are closer to 36%. Thus, short-term market psychology is still favorable from a contrarian standpoint.

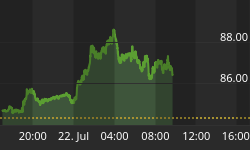

Let's start our market overview with the bank industry since this is one of the more sensitive and important areas in the market, along with the financials. The Bank Index (BKX) was up 2% on Friday to close the latest week at 111.39. The BKX is currently reaching for its pivotal resistance near the 114 level which was last achieved at the early May high, led by J.P. Morgan (JPM) and Comerica (CMA). We've been discussing this scenario of a bank stock rally before the market's next corrective move and so far BKX has performed as expected. We previously discussed the sudden breakdowns of certain key bank stocks and now another low has been made since our last report, namely Capital One (COF) which broke down to a new low last week and made a lower one on Thursday. This forms the internal low for COF and the recent breakdowns of certain key bank stocks are evidence of the bottoming 4-year cycle. It also shows the work of the insiders in the way of focusing all the cycle-related selling pressure in a handful of stocks in order to take the pressure off the bigger market (i.e., "internal rotation").

The Dow Industrial index started Friday's session strongly and held up throughout the day, unlike Wednesday's and Thursday's trading sessions. The Dow rallied 120 points on Friday to end the week at 11,219. The S&P 500 index (SPX) was up 1.22% on Friday to close the week at 1278.55. The rally effort made on Friday put the SPX above its dominant interim 90-day trend line. Is this enough to qualify as a legitimate upside breakout? Not quite, for there is a more pivotal resistance at 1290 which, if broken on the upside, will confirm the price low for the SPX made in June and pave the way for a test of the May high.

The tech sector has had a rough go of it in the past few weeks and has clearly born the brunt of the "hard down" phase of the 4-year cycle. This has been par for the course ever since 2000 and the large caps have held up better. The selling in the techs, including the semiconductors, has been heavy since the April peak and a bottom is forming already even before the 4-year cycle bottoms around September 1. Can the tech sector bottom before the yearly cycles? Yes, for this happened at the last yearly cycle bottom in 2004 (when the 10-year cycle bottomed in October) and the NASDAQ that year put in its final low for the year in August. We may be witnessing something similar in the current tech market as a number of positive divergences show up in many charts, including the semiconductors, biotechs, and even nanotechs. Incidentally, once the 4-year cycle is behind us the aforementioned sectors should be among the star performers in the months ahead. We've already isolated some potential turnaround stocks in this sector and will be discussing them in the coming days.

We've made an ongoing observation since last year that whenever a major market bottom is forming there always seems to be a handful of critical "name" stocks (mostly tech stocks) that get hammered in quick fashion. We call this "internal rotation" for it allows the broad market to escape serious punishment at the expense of a few key stocks. Last year's victims included Amazon (AMZN) and Google (GOOG). This time around it was Yahoo (YHOO) and again AMZN, both of which took big hits in recent days.

The chart pattern showing up in a number of tech stocks across many different industries right now is that of a downside "channel buster" where the price gets knocked below the lower boundary of a downward sloping trading range, usually on very high trading volume. This forms, in most instances, the final low or at least the internal low of the intermediate-term cycle for the stocks in question. With so many tech stocks showing the channel buster recently I can't help but believe the techs are putting in their final low for the 4-year cycle and will likely test and confirm these lows before the cycle bottoms later in August. Some will probably make a lower low in terms of price, but again, I believe the internal low is already in for the broad tech stock market just as it was in before the 10-year cycle bottomed in late 2004.

The 6-month daily chart showing the NASDAQ 100 Index (NDX) displays a rather prominent positive divergence between the price line (which has made lower lows) and the MACD indicator (which has made a higher low) in the past two months. This is normally a bullish pattern and suggests a turnaround process is near. It doesn't guarantee that the absolute low has been made in terms of price, for there can still be another low made before the 4-year cycle bottoms. But what this positive divergence is showing us is that the worst of the damage has already been inflicted on the NASDAQ and we should see a gradual recovery process before long, and as mentioned above I think we'll see a short-term rally attempt up to the nearby resistance at the 1550-1575 area where the 60-day moving average intersects.

The S&P Midcap 400 Index (MID) is among the most important to monitor for clues as to short-term market direction. MID, which closed up 1.61% on Friday at 741, looks like it wants to test its immediate resistance at the 765 level. This is where the important 90-day moving average intersects in the daily chart. Closing above the 90-day MA will confirm the June low in MID. Above 765, MID will encounter a layer of resistance and may have to wait until the 4-year cycle bottoms later next month before its next extended rally gets going.

The Russell 2000 Small Cap Index (RUT) also looks like it will test overhead resistance at the 720-730 area soon between where the 60-day and 90-day moving average intersect in the daily chart. Russell closed at the 700 level on Friday.

To show you the value of positive divergences, several weeks ago you'll recall we looked at the potential turnaround pattern in the daily chart of the AMEX Healthcare Products Index (RXH). As the RXY was showing higher lows in a number of its internal indicators compared to the price line it was evident that internal momentum was building upward for the healthcare product industry. The upside breakout for RXH finally occurred earlier this week along with the strong forward surge in the Pharmaceutical stocks. RXH broke above its 1380 level resistance and closed the week just below its May high at 1436.50. In doing so RXH has become "overbought" internally and will soon correct these imbalances.

The Biotechnology Index (BTK) is another index showing breakout potential ahead of the 4-year cycle bottom in the near term and is currently testing its overhead 90-day moving average resistance at the 660 level, closing at 656 on Friday. Like RXH, the BTK index is showing a positive divergence signal in some of its internal indicators and a resolution to its 3-month trading range is near. Later in this report we take a look at a potential turnaround trade in this sector and will discuss some more next week.

After showing a negative divergence to the Dow Industrials, the Dow Transportation index (DJTA) had a relief rally on Friday and closed higher by 2.54%. DJTA is currently oversold internally and could end up testing its major near term resistance between the 4600-4700 area where the 30/60/90-day moving averages are all grouped together. We'll have to watch to see how DJTA reacts to this resistance for it will show us whether the recent relative weakness the DJTA has been displaying has been merely seasonal in nature or the start of something bigger. It could be a "bear trap" ahead of the 4-year cycle low, however, and I have a hard time believing the DJTA is signaling a recession is at hand since a recession following a 4-year cycle bottom is extremely rare.

Is the Fed finished raising interest rates? Many analysts think so and that's the story the financial press has been giving out as one of the reasons behind this week's rally. One observation that can be made is that the 10-Year Treasury Yield Index (TNX) has backed off noticeably from its late June high after making that bearish upside "channel buster" we talked about last month. Since peaking in June TNX has fallen below the 5.0 level and is now below its 90-day moving average. A snap-back rally usually follows the first close under the 90-day MA, but the important thing to watch is whether the June high holds up on subsequent rallies. If so it would form a good indication that rates have peaked for the latest cycle and a slight reduction in rates following the 4-year cycle bottom would actually fit nicely with the recovery bull market scenario beginning within a few weeks and extending into 2007.

As far as kicking off a new sustained rally leg, the action of the past week, while promising, is still inconclusive and will soon encounter a fresh layer of overhead resistance. How the indices react in the face of this resistance will be revealing. One thing we must see is an improvement of the new highs/new lows differential on the NYSE. The past couple of days were a start but we're not there yet as there yet as there should ideally be several days in a row of less than 40 new lows on the NYSE to show that internal selling pressure has completely dried up in the broad market. We also need to see improvement on the Fed securities lending front.

Finally, there's the matter of the 4-year cycle which hasn't formally bottomed yet. The question everyone seems to be asking is, "Is it possible this cycle has bottomed 'early' already?" The answer is no, for the 4-year cycle is fixed in its duration as to when it peaks and troughs. However, it's not without precedent that the leading market indices can confirm price lows and even begin to rally ahead of the 4-year cycle low. The last such occurrence was in 1994. Also worth mentioning (as someone recently brought to my attention) is that back in '94 the Dow Transportation Average (DJTA) made a lower low in contradistinction to the Dow Industrial's higher low -- just like today! That turned out to be a "head fake" for the bears, for 1995 was one of the most bullish years in recent memory. The lesson here is that the Dow Theory, while a very helpful tool, isn't infallible.

While a broad market bottom ahead of the 4-year low wasn't my original expectation, it's possible we're witnessing a repeat performance of the 1994 experience. It's still a little too early to tell, however, and we could still yet see a final test of the June lows in some indices before this cycle has bottomed, although the double bottom low from June and July in the Dow Industrial index looks pretty strong and may prove to be a solid one. The important thing is to remain flexible in our thinking and vigilant in our chart scouting so we'll be able to capture worthwhile trading opportunities whenever they present themselves.

The XAU gold/silver stock index closed higher for the week and ended up at 141.62, slightly above its 60-day and slightly below its 90-day moving average. XAU, like many other major indices, looks like it could test its nearest pivotal resistance at the 150 area soon.

Beginning next week is when things start to get interesting for the gold stock industry. The month of August begins seasonal strength for the golds (which we'll discuss more in depth in Monday's report). And as we previously discussed there will be quite a few quarterly earnings announcements coming out next week which could have both favorable and unfavorable impacts on individual stock prices. (But with record high gold prices in the second quarter and overall strong corporate cash flows I can't imagine many, if any, negative earnings surprises).

Those are the positives. Now for the negatives. The two main negative considerations weighing against the precious metal stocks right now (white and yellow metals) include the 4-year cycle which is scheduled to bottom in a few weeks as well as some negative internal momentum signals the intermediate-term momentum indicators. What this could mean is that gold and silver stocks remain in their trading ranges until the cycle bottoms and the pressure is lifted. There are some charts in the gold and silver stocks, however, that are showing relative strength and forward momentum and the stocks having the best charts will be the ones most likely to move higher in August based on seasonal strength in the face of cyclical downward pressure. We've been discussing some of these lately but among them are Kinross (KGC), Agnico-Eagle (AEM), Inmet (IMN:TSX) and basically any gold stock that is above its rising 90-day moving average. Another one that's just below it, Royal Gold (RGLD), also has rally potential in coming weeks due to having built up a very high short interest which could come into play once the 90-day moving average resistance is broken to the upside.