The good news is:

• The market is oversold going into next week which has had a positive seasonal bias.

Short term

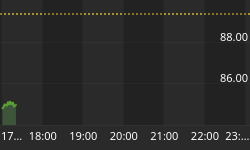

Occasionally price levels evolve that offer support, that is, prices are unable to drop significantly below the support level. The Russell 2000 (R2K) and the NASDAQ composite (OTC) have been two of the weakest of the broad based indices since the May top and both are near levels that have offered support in the past.

The first chart shows the R2K which closed Friday less than 1% above a support level that goes back to late last year.

The next chart shows the OTC with a support line drawn from the October low. The OTC closed Friday about 1% above the level that provided support last October and again last month.

The market is at a critical point it is important that these support levels hold.

Intermediate term

The secondaries (small caps) lead both up and down. The next two charts cover the period from late March through last Friday with dashed vertical lines drawn on the 1st trading day of each month.

The 1st chart shows the R2K in red and an indicator showing the percentage of the component issues of the R2K that are above their 50 day exponential moving average (EMA) in green.

The next chart is similar to the one above except the index is the S&P 500 (SPX) and the indicator shows the percentage of the component issues of the SPX that are above their 50 day EMA.

Since the June low, measured both by price and the percentage of issues above their 50 day EMA's the SPX has been stronger than the R2K.

This is a negative.

Seasonality

Next week includes the five trading days prior to the 3rd Friday (Options expiration) in August during the 2nd year of the Presidential Cycle.

The tables below show daily returns for the OTC from 1966 - 2002 and S&P 500 (SPX) from 1954 - 2002 during the 2nd year of the Presidential Cycle. There are summaries for both the 2nd year of the Presidential Cycle and all years combined beginning with 1963 for the OTC and 1953 for the SPX. I have shortened the SPX reporting period because prior to 1953 the market traded 6 days a week possibly skewing the data because Friday was not the last trading day of the week.

During the 2nd year of the Presidential Cycle, in the coming week, both the OTC & SPX have been up 70% of the time with a modest gain. Over all years both indexes have been modestly positive.

Report for the week before Options expiration Friday during Aug

The number following the year is the position in the presidential cycle.

Daily returns from Monday through Friday.

| OTC Presidential Year 2 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1966-2 | -0.10% | -0.30% | -1.28% | -0.67% | -1.14% | -3.49% |

| 1970-2 | -0.85% | 0.62% | 0.76% | 1.08% | 0.41% | 2.02% |

| 1974-2 | -0.47% | -2.00% | -2.00% | -0.55% | -1.53% | -6.54% |

| 1978-2 | 0.08% | -0.12% | 0.62% | 1.03% | 0.42% | 2.04% |

| 1982-2 | 0.34% | 1.63% | 2.00% | -1.83% | 1.24% | 3.38% |

| 1986-2 | 1.11% | 0.91% | 0.97% | 0.69% | 0.17% | 3.85% |

| Avg | 0.04% | 0.21% | 0.47% | 0.09% | 0.14% | 0.95% |

| 1990-2 | 0.07% | 0.50% | 0.27% | -2.00% | -2.00% | -3.16% |

| 1994-2 | 0.17% | 0.36% | 0.97% | -0.07% | 0.04% | 1.47% |

| 1998-2 | 1.55% | 2.00% | -0.67% | -0.56% | -1.90% | 0.43% |

| 2002-2 | 0.06% | -2.00% | 2.00% | 0.80% | 1.19% | 2.05% |

| Avg | 0.46% | 0.21% | 0.64% | -0.46% | -0.67% | 0.20% |

| OTC summary for Presidential Year 2 1966 - 2002 | ||||||

| Avg | 0.20% | 0.16% | 0.36% | -0.21% | -0.31% | 0.20% |

| Win% | 70% | 60% | 70% | 40% | 60% | 70% |

| OTC summary for all years 1963 - 2005 | ||||||

| Avg | 0.22% | -0.03% | 0.16% | 0.00% | -0.11% | 0.23% |

| Win% | 65% | 50% | 63% | 52% | 53% | 53% |

| SPX Presidential Year 2 | ||||||

| Year | Mon | Tue | Wed | Thur | Fri | Totals |

| 1954-2 | 1.07% | 0.23% | -0.10% | 0.23% | 0.16% | 1.59% |

| 1958-2 | 0.27% | -0.93% | 0.17% | 0.21% | -0.86% | -1.14% |

| 1962-2 | 0.14% | 1.08% | 0.70% | -0.03% | 0.63% | 2.52% |

| 1966-2 | -0.52% | -1.34% | -0.55% | -1.26% | -0.67% | -4.34% |

| 1970-2 | 0.20% | 1.15% | 1.00% | 0.88% | 2.00% | 5.24% |

| 1974-2 | -1.37% | -1.58% | -2.00% | -0.56% | -0.83% | -6.34% |

| 1978-2 | 0.01% | -0.12% | 0.77% | 0.41% | -0.33% | 0.74% |

| 1982-2 | 0.23% | 2.00% | -0.47% | 0.58% | 2.00% | 4.34% |

| 1986-2 | 1.60% | 1.11% | 0.96% | 0.24% | 0.37% | 4.27% |

| Avg | 0.13% | 0.51% | 0.05% | 0.31% | 0.64% | 1.65% |

| 1990-2 | 0.06% | 1.09% | 0.20% | -2.00% | -1.37% | -2.02% |

| 1994-2 | -0.16% | 0.82% | 0.03% | -0.43% | 0.11% | 0.38% |

| 1998-2 | 1.98% | 1.61% | -0.28% | -0.59% | -0.95% | 1.76% |

| 2002-2 | -0.53% | -2.00% | 2.00% | 1.16% | -0.16% | 0.46% |

| Avg | 0.34% | 0.38% | 0.49% | -0.47% | -0.59% | 0.15% |

| SPX summary for Presidential Year 2 | ||||||

| Avg | 0.23% | 0.24% | 0.19% | -0.09% | 0.01% | 0.57% |

| Win% | 69% | 62% | 62% | 54% | 46% | 69% |

| SPX summary for all years 1953 - 2005 | ||||||

| Avg | 0.17% | -0.04% | -0.04% | 0.02% | -0.01% | 0.09% |

| Win% | 66% | 51% | 56% | 47% | 60% | 53% |

Conclusion

The market was down 4 out of 5 days last week leaving it short term oversold and next week has a strong positive seasonal bias.

I expect the major indices to be higher on Friday August 18 than they were on Friday August 11.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.