One of the things we do each night is evaluate the quality of each day's price move. We want to know whether a trend is genuine, with broad-based participation, implying a longer shelf life, or whether it is the result of panic buying or selling, which suggests high risk of termination, and reversal. When directional volume, issues, and points are near, or over 90 percent, that is an indication of fear being the motivating factor for the price move, not a solid sustainable trend. Selling panics are an indication of selling exhaustion, often leading to strong reversal rallies. But the reverse is true, which is important when we are in what appears to be a strong price rally, since Bear markets can wipe out months and years of gains from Bull markets in short order, in a matter of weeks. So, we want to know if a multi-month rally has occurred from solid, broad-based buying, or whether it was intervention short-covering induced.

Most autumns we see a significant decline. This attracts shorts. Bears take aggressive short positions where they buy puts, or agree to sell shares in the future at today's prices but do not yet own those shares. They are gambling prices will decline. Interventionists feed off of shorts. The rally since July has been almost entirely short-covering. We get one big move, about once a week, on buying panic, then no follow-up, with slightly down to sideways price action until the next week. What has been missing has been supply. Sellers have noticed these out of the blue short-covering rallies, so have disappeared. The interventionists have succeeded in muting supply pressure. This type of rally can continue for quite some time, and drive prices quite high, as we have seen. But it is a death trap. It is artificial. It will end as soon as some trigger event sends fear into markets, the kind that catches shorts on the sidelines, buyers exhausted, and interventionists helpless to play their game. We believe a Democrat victory in the coming election could be such an event.

Get this: All of the progress of this three month summer/autumn rally, all of it, occurred in only 9 days of trading, and all but one of the nine was a short-covering rally. In other words, without intervention induced short-covering, the Dow Industrials would be exactly where they stood in mid July, at the start of this rally. Other than those 9 trading days out of 63 since July 14th, the other 54 days of trading produced only 4 percent of the upside progress, and zero since July 19th. Zero. In 8 of the 9 trading days where upside progress was made, evidence of short-covering was present. That evidence included a larger rise in Demand Power than the decline in Supply Pressure, suggestive that shorts joined the buying. That evidence also included either upside volume, advancing issues, or upside points coming in at or very near a buying panic 90 percent. In each instance, a sharp up move started early in the day, followed by buying panic as shorts felt compelled to cover, pushing the rally higher throughout the day. There was only next-day follow-through to the upside one time, on August 16th, after a short-covering rally on the 15th, but it too showed evidence of short-covering. No days other than August 15th showed strong upside follow-through. Solid rallies see follow-through. This rally has been manufactured.

The short-covering rallies:

| Date | Rally | Upside Volume | Advancing Issues | Upside Points |

| July 19th, 2006 | + 212.19 | 93% | 86% | 94% |

| July 24th, | + 182.67 | 90 | 82 | 98 |

| July 28th | + 119.27 | 81 | 81 | 88 |

| August 15th | + 132.39 | 89 | 84 | 98 |

| August 16th | + 96.86 | 81 | 76 | 89 |

| September 12th | + 101.25 | 77 | 76 | 90 |

| September 26th * | + 93.58 | 72 | 64 | 82 |

| October 4th | + 123.27 | 83 | 79 | 97 |

| October 12th | + 95.57 | 83 | 79 | 92 |

| Total Progress Points +1,157.05 | ||||

| Gain from 7/14 to 10/12/06 = 1,208.35. | ||||

| * This rally was probably not significantly short-covering, although the rise in Demand Power was greater than Selling Pressure's decline, so may have had some minor short-covering help. | ||||

The point of examining whether the quality of this rally is broad-based or is from shortcovering, is critical as to the risk that it will end badly. Clearly the rally from July has not been broadbased, is not sustainable on its own, is not a classic "Bull" market, but has occurred from a lack of supply and a ton of buying and price pushing from those most pessimistic about the market, not from optimists. There was no net progress in 52 of the past 60 trading days. Think about that. All this market requires to tank is a reason to sell. The buying isn't there. Overall, the decline in Supply Pressure since July 19th was 25 points, more than the rise in Demand Power, which was 21 points. This is not what we should see in a solid bona fide rally. Sustainable rallies require a stronger rise in Buying Power with a corresponding decline in Selling Pressure. We have the opposite condition here, a weak rise with the decrease in Supply exceeding the increase in Demand. Can prices rise further from here? Sure. Figure another intervention short-covering rally or two before the election, and maybe another 200 points? But, it will stop when an event sends fear into Wall Street, and end badly.

Genuine rallies occur typically with 2 to 1 upside volume, advancing issues, and upside points, with the Demand Power rise about equal to the Supply Pressure decline each day, and we see follow through several days in a row. We don't see once a week hundred point gains, and then sideways action for four or five days. If buyers are excited about the future, we should see strong steady buying on a daily basis, with periodic profit-taking selling. That is not what has happened since July.

The motive? The November elections. Wall Street loves Republican control. The means? Hidden M-3, and the lawful actions of the Working Group and their surrogates as established by President Reagan in 1988.

One of our challenges is to account for intervention in our technical market analysis. We have designed key trend-finder indicators to take into account intervention short-covering rallies in forecasting short-term, multi-week trends.

One of the best tools we have is the S&P 500/Dow Industrials Purchasing Power Indicator. It is a measure of Demand and Supply momentum. It is market data based, with no judgment or emotion influencing its daily calculation. The next chart shows how this indicator called a "buy" on July 19th, 2006, and has not vacillated since, remaining on that "buy" signal throughout this three month rally. It picked up the short-covering, it picked up the lack of supply pressure, and pointed up. We update this measure every evening and report it in our daily market briefings. Since the "buy" signal was generated, the Dow Industrials have risen 947 points, or 8.6 percent.

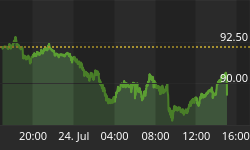

We also have a Purchasing Power Indicator for the NASDAQ 100. Its chart is shown below. The NASDAQ 100 Purchasing Power Indicator generated a "buy" on July 24th, 2006. The NDX then rallied 122.68 points, or 8.3 percent. On September 6th through the 12th, we had a minor pause. On September 12th, 2006 the NDX Purchasing Power Indicator generated another "buy" signal, which has led to a 113 point, or 7.0 percent rally.

So, although we are seeing a lengthy short-covering induced rally here, our key trend-finder indicators are picking up on it, which is all that matters for short-term traders. The problem is, if you are a long-term investor, this is not the sort of rally that is likely to last more than a few months. Further, our other technical analysis work suggests we are putting in a major top here. Every single time, since 1913, the Fed raised the discount rate above 6.00 percent, we have seen a substantial decline start within a year thereafter, several as much as 30 percent. That discount rate event occurred again in May 2006. We would rather this rally from July was genuine and not artificial.

For a Free 30 day Trial Subscription, go to www.technicalindicatorindex.com and click on the button at the upper right of the Home Page. Check Out Our September Subscription Specials.

"And there was a man in the synagogue possessed by the

spirit of an unclean demon, and he cried out with a loud voice,

"Ha! What do we have to do with You, Jesus of Nazareth?

Have you come to destroy us? I know who You are -- the Holy One of God!"

And Jesus rebuked him, saying, "Be quiet and come out of him!"

And when the demon had thrown him down in their midst,

he came out of him without doing him any harm."

Luke 4:33-35

If you are a trader, we offer market timing signals. If you are a conservative long-term investor, we have just come out with our Conservative Balanced Investment Portfolio, which we will update with transactions on a regular basis.