This week saw a gratifying, almost universal shift to bullish sentiment on gold and silver. Of course, readers of this update heard it here first on Oct. 26, when we not only predicted the move, we explained why it would happen. Now some analysts are predicting that metals and miners will be one of the hottest sectors of the next year, so beginning this week, in addition to commentary on the precious metals markets, this newsletter will also feature regular commentary on selected mining stocks in an effort to provide timely and actionable information to help you make money in the precious metals and derivatives markets.

There's no doubt the Fed got the payroll number it was looking for on Friday. Last week's FOMC policy statement said that relatively low energy prices would drive an "expanding economy" and continued "high resource utilization." But we interpreted the fact that the Fed statement omitted language including commodity prices as a measure of inflation as indicating that rises in commodities prices were inevitable and would not stand as an obstacle to future interest rate-cutting like energy and economic data. We called it a "buy" signal.

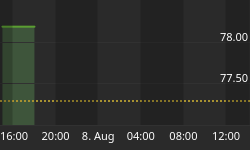

The early part of the week saw the new Fed stance play out with a more than 3% rise in gold and silver, increased odds of a rate-cut in early 2007, and the appearance of several new market analysts proclaiming a strong technical outlook for gold and silver. In addition to illustrating the strong performance of the metals in the wake of the Fed statement, the chart above shows what appears to be a decoupling with oil, a sign we've been anticipating as an indication of renewed investor interest in the metals sector. The mother of all the commodities markets, fluctuations in investment demand for oil tend to swallow the smaller gold and silver markets and this will probably happen again at some point in the future. Decoupling is an assertion of the metals' own bullish fundamentals. With many energy stocks underperforming the market on the last rally, some of the money that would be going into energy might now be heading towards the metals. Furthermore, rising gold and silver over flat oil would exactly match the FOMC forecast and hey, they've done a pretty good job so far.

Equities markets struggled this week because of uncertainty about the economic slowdown. Higher wage inflation and lower productivity boosted inflation fears and kept potential dip-buyers mostly on the sidelines. Hand-wringing over gold, though, as it retook the $600 level, was misguided given the October statement. Unless there is a parabolic move that clearly evidences a speculative bubble, the Fed will use economic data, not commodity prices to determine its future interest rate policy. With straight months of gains on the major indices, it's not shocking that stock market bulls saw the week as a chance to lock-in profits, while fund managers at the end of their fiscal years declared victory and made adjustments to their strategies for the quarter ahead. Friday's strong payroll report breathed new life into the "soft-landing" hypothesis, but couldn't stem the tide of red ink because tighter payrolls could be inflationary in the Fed's view. Rate-cut odds for early '07 dropped accordingly and the question now is what effect this will have on gold and oil.

Clearly silver was too cheap under $12 and gold under $600. Now that we've entered the strongest season for metals, historically, and the word is out that the metals are likely to be a hot sector over at least the next quarter, we're up above those psychological levels and close to near term resistance. Still, we should expect money to rotate into the metals and the miners at a fairly steady pace next week to help push them beyond. Over the coming weeks gold could be on its way to as high as $650-675 and I've already stated my expectation for silver to retest $13, probably by the end of the year. But, at this point, we simply don't have the underlying fundamental picture in place for either metal to seriously challenge the May highs.

Despite the decoupling action we saw this week, oil will continue to be an important factor. The so-called "Goldilocks economy" has come into question repeatedly over the past few months, but was reaffirmed every time either by very conveniently timed economic data or well-received remarks by Fed governors. But two numbers that don't respond particularly well to Fedspeak or data are consumer confidence and retail sales, both of which have recently declined. The last FOMC statement called for an expanding economy, but the latest backward-looking data still show a slowing economy and the overall effect of the housing slowdown is still not clear. We're quickly approaching a critical period where the economy will either rebound decisively or drop irrefutably into recession. To put it mildly, the economy needs cheap oil right now.

It's not certain exactly when the Fed anticipates economic expansion to appear in the data, but it continues to credit the economy's "moderation" to its own string of quarter point rate hikes. But the truth is that the spigot has been wide open, with total Fed credit expanding and fractional reserve and margin requirements shrinking. Banks continue to target subprime borrowers and offer creative mortgage options. Not surprisingly, the rise in gold and silver matched a simultaneous downturn in the dollar. If the data continues to worsen and they are forced to reverse their view of the economy, this could increase odds of a rate-cut and should continue to boost metals, if not mining stocks, but this can't be considered a foregone conclusion.

Next week we'll see a new crude inventory figure, which could be important, but it seems like $60 oil is an acceptable level for all parties at the moment and the price probably won't move too far from there in either direction for a while. We'll be watching mostly to see if the metals continue to act independently or return to lockstep. For more immediate analysis and updates, visit www.tradingthecharts.com.

Featured Mining Stock

Coeur D'Alene (CDE)

Until very recently, Coeur D'Alene was the world's largest primary silver producer. The company's very capable management has worked aggressively in the past year to reduce its cost per ounce to about $4, and, though it struggled to turn a profit during a period of acquisition and low silver price, advances in the price of silver have created impressive year-over-year comparisons in recent quarters. New development and acquisition promise to soon return Coeur to its status as largest primary silver producer.

Going into its quarterly report and conference call next Monday, however, the company has two strikes against it, as far as many investors are concerned. Still, if the company's past statements prove true, Wall Street may be grossly over-exaggerating their effect on its bottom line and setting the stage for an aggressive comeback.

First, in it's San Bartolome property, CDE has committed the cardinal sin of attempting to mine in a politically hostile region. Otherwise a promising operation ultimately estimated to yield 6 million ounces of easily obtainable silver each year, the San Bartolome project has the unfortunate condition of happening to be located in Bolivia, a tumultuous country where recently elected president Evo Morales has publicly promised to nationalize the country's energy and mining industries and radically alter its tax policies. In May, Morales sent soldiers to enforce his nationalization policy at oil fields owned by Exxon Mobil and others. Coupled with occasional socialist violence in the region, he's generally made himself an albatross around the neck of any company with Bolivia exposure.

Despite the fast pace of energy nationalization, details about mining reform have been scarce. Morales already stated he would not nationalize existing mining projects outright, but will rather seek to encourage foreign investment in aiding his country's mining and processing of its resources. Spokespersons for CDE are quick to note that Bolivia already owns all the natural resources at San Bartolome and that the company only leases mining rights at the property through a wholly owned Bolivian subsidiary. Still, investor sentiment can be difficult to reverse and Bolivia continues to be seen as a high-risk investment.

Uncertainty about the political climate in Bolivia continues to weigh on CDE's share price, but actual harm seems unlikely. Management has even gone to the length of extending the construction period and insuring their assets in the region for $155 million against appropriation and political violence. Morales' admission on Tuesday that his country cannot even afford to nationalize its mining operations, in addition to the company's quarterly report and conference call on Monday, will likely be a catalyst for this stock in the coming weeks.

Strike two is a lawsuit by the Sierra Club against CDE's Kensington mine in southeast Alaska. Since 2004, construction at the site has run afoul of several environmentalist groups despite progressing as permitted and reviewed by the U.S. Forest Service, EPA, U.S. Army Corps of Engineers, and Alaska Coastal Management. Several attempts to revoke the permits have failed, but under pressure from local activists, the Army Corps of Engineers has now voluntarily suspended CDE's wetlands permit pending further review, and the Ninth Circuit has issued an injunction halting construction at a tailings facility on Lower Slate Lake. CDE maintains it has acted at the highest standards of environmental, safety, and health compliance and even received a Bureau of Land Management award earlier this year. Drilling and exploration on the Kensington property have continued in non-wetlands areas and the company does not expect to suffer materially as a result of the ongoing challenge to its operations in Alaska.

Another topic that needs to be discussed at the conference call Monday is the entrance into a Rule 10b5-1 plan to publicly sell up to 500,000 shares of the company's common stock by Dennis Wheeler, the company's Chairman, President and CEO. As of the date of the filing, Mr. Wheeler has not made public his intentions regarding the plan.

These two strikes have depressed the value of CDE shares over the past year and caused the stock to underperform other stocks in the sector. But, as neither mine property is yet in a revenue-producing stage, neither setback is expected to influence the current quarter results. Further, as these issues become resolved, and the new mines' production comes on line, sudden corrections upward may occur. For Monday, analysts are expecting earnings of $.06 - .09 per share ($.08 consensus, up from $.01 last year) on revenues of $58.88 million (up from $44.1 million). We should note that the widely lauded Silver Wheaton (SLW) has a similar cost per ounce and annual EPS, but is valued well above CDE at 57 times earnings, and trades substantially higher. As this fact becomes more widely recognized, CDE could easily move above the $6 level in a favorable trading environment.

If you've enjoyed this article, signup for Market Updates, our monthly newsletter, and, for more immediate analysis and market reaction, view the charts exchanged between our seasoned traders in the www.tradingthecharts.com forum.

Continued success has inspired expansion of the "open access to non subscribers" forums, and our Market Advisory members and I have agreed to post our work in these forums periodically. Explore services from Wall Street's best, including Jim Curry, Tim Ords, Glen Neely, Richard Rhodes, Andre Gratian, Bob Carver, Eric Hadik, Chartsedge, Elliott today, Stock Barometer, Harry Boxer, Mike Paulenoff and others. Try them all, subscribe to the ones that suit your style and accelerate your trading profits! Those forums are on the top of the home page Trading the Charts.

Also, click here to see how perfectly my hourly Trend chart caught this week's high in the S&P. If you like what you see, send the links to friends!