With the Federal Reserve on data watch for the past year, today's benign CPI (-0.5% headline and 0.1% core) should start appeasing the Fed's more hawkish members. Emphasis now shifts to the extent of the growth slowdown and next month's release of the core PCE price index.

The dollar's resilience in the face of the slowest core CPI reading in 13 months (when rounded to 2 decimals) and the first monthly net selling in US treasuries by foreigners in 3 years can be partly explained by the non-dollar side of the Forex equation and partly explained by the need to await further evidence for more conclusive inflation data. Fading market speculation of a Bank of Japan rate hike before year-end coupled with mixed growth reports and low CPI figures from the Eurozone (lowest core CPI in 6 years) have also helped the dollar add on to Tuesday's gains.

The other major factor weighing on the euro is persistent verbal intervention by European politicians signaling to the European Central bank that it's time to halt the rate hikes and watch the strengthening of the euro. Today, French president Chirac said about the ECB: "...one can question the way it works or the choices it makes as they carry extremely serious consequences for our fellow citizens." Adding that: "Criticisms made [of the ECB]..Can be seen all around Europe, notably in all euro countries". Chirac's comments follow those by French PM Dominique de Villepin yesterday calling for more collaboration among Eurozone monetary authorities on managing the currency. Villepin called on Eurozone governments to create a "monetary shield" to protect local industries from nations accused of keeping their currencies artificially low. Understandably, Villepin's comments were made during his visit to Airbus headquarters in Toulouse to show support for the ailing company. Airbus' parent European Aeronautic Defence and Space Company (EADS) reported earnings have dropped 17% drop in revenues in the first nine months of the year.

The euro was also hit by comments from Bert Ruerup, chairman of Germany's council of economic advisers, indicating the ECB should halt its tightening as there are "no inflationary risks and also no second-round effects" to justify a hike. The ECB is widely expected to lift rates to 3.5% from 3.25% at its December 7 meeting.

Despite the European Central Bank's mandate of operational independence on monetary policy, Eurozone politicians have repeatedly proven to have a significant short-term impact on the euro when expressing their discontent with rapid strengthening in the euro. Considering that France's parliamentary elections are next April, traders could expect more comments from politicians to sway the electorate in their favor, especially in light of the deteriorating performance of companies such as Airbus and the stagnant GDP growth in Q3.

A more dollar-friendly version of the FX diversification story suggests that central banks will acquire more non-US dollar assets in their new accumulation, rather than carry out outright selling of their existing dollar reserves, which would be detrimental to the currency value of these holdings. This means that the future action of these central banks would entail purchasing assets denominated in yen, sterling and even gold. This notion is especially after a Chinese central bank official was quoted today as saying the bank has been buying yen for its $1 trillion in FX reserves, rather than selling their existing dollar reserves.

While most of the attention of FX reserves revolves around China, very little has been said on Japan--the largest holder of US treasuries. Today's September TICS report showed Japan continued to quietly reduce its own holdings (see chart below), prolonging the downtrend of the past 2 years (see chart). Meanwhile, treasury holdings by offshore Caribbean centers hit their lowest level since February 2004. We mentioned in our morning note that the new methodology of the TICS data will likely lead to increased volatility as it encompasses the acquisitions of short-term securities. But we do think that the TICS data will fall off FX traders' radar screen for the next few 2-3 months as emphasis shifts to the each and every evidence of inflation data, which is the core of the Fed's policy path.

Now that the market has seen proof of slowing inflationary pressures in the CPI report, it will await similar evidence from the all important core PCE price index -- preferred by the Fed for measuring inflation. The October report is due in two week's time, and is expected to retreat towards the 2.1% level from 2.4%. Any figure below 2.1% should be dollar positive.

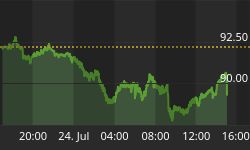

The chart below shows the short-term recovery in GBPJPY 4-hour chart, in light of today's strong UK retail sales figures and fading speculation of a December rate hike by the Bank of Japan. Hovering around the 223.20s, GBPJPY is seen attaining the preliminary target of 223.60 target, which is the 38% retracement of the 225.34- 222.52 decline. Key resistance stands at the 223.93 -- 50% retracement of said move and trend line resistance extending from the Nov 9 high.