The US dollar gets a respite following a sharp sell-off late last week as traders neutralize excessive selling in a relatively data scarce trading session. Tuesday's speech by Fed Chairman Bernanke on the US economic outlook may provide further stability to the US currency as the Fed Chairman is unlikely to depart from his obligatory hawkishness and risk triggering a renewed attack on the currency.

The dollar's stabilization is reflected in gold prices as the metal retreats from its 3 ½ month high $641.62 per ounce to $637.00 per ounce. We reiterate that last week's thin trading activity did play a major role in amplifying the dollar sell-off, but should not overshadow the fundamentals and market flows acting against the US currency.

Now that the dollar sell-off has finally drawn the attention of those beyond currency traders and analysts, it's worth summing the major factors triggering the latest sell-off in the currency. Escalating optimism in the Eurozone underlined by Thursday's unexpectedly strong German IFO business survey hitting a 15-year high in November, coupled with inflation vigilance by the European Central Bank officials, have strengthened the case for ECB rate hikes extending to 3.75% by end of Q1 from their current 3.25%. Speedy unwinding of yen carry trade positions against the higher yielding currencies of the USD and AUD have also been key drivers to the USDJPY declines, especially after Comments from People's Bank of China officials warning about the risk to Asian currency reserves from further dollar slide, suggesting the much talked about shift in USD reserves is either already underway or is a matter of time.

One of the key drivers to the sustained run-up in EURUSD and GBPUSD is the unprecedented contrast in monetary policy outlooks between the European Central Bank and the Bank of England , and the Federal Reserve. Never since the birth of the euro in 1999 have we seen an environment where the ECB and the BoE in the midst of an interest rate tightening cycle, while the Federal Reserve was approaching an interest rate easing cycle. It is this unprecedented contrast in monetary policies that is behind the accelerating flows emerging against the US dollar, even if the UK and Eurozone rates are currently below their US counterpart. This unfolding yield landscape is also leading to a sharp narrowing in the 10-year spreads between the US and the Eurozone.

This point is further validated by the lack of continuity in the USDJPY rallies. With Japanese short-term interest rates at 0.25%, 500-bps below their US counterpart, the yield differential remains one of the obstacles to an uninterrupted decline in USDJPY. Also, the Bank of Japan's cautious stance towards its planned tightening pales in contrast to the unequivocal hawkishness of the ECB and the BoE in the face of increasing levels of money supply growth, inflation growth as well as business and consumer demand.

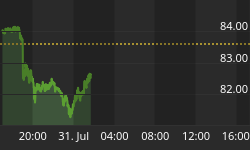

The chart below shows the US dollar index (trade weighted index against the euro, yen, sterling, Swiss franc, Canadian dollar and Swedish Krona) is down 10% from the 92.63 highs reached a year ago (November, 14, 2005). The MACD measure of trend momentum has entered negative territory, suggesting 82.70 could be reached before year end. Recall we noted in our long-term piece of October 20 th that: "Given the dollar's existing high yield advantage and the continued upside risks to inflation, we expect the dollar index to fall by no more than 5.0% from its 87.30 peak of October 13th, making 83.80-84.0 our year-end target."

The United Arab Emirates' central bank announced a 19% increase in its FX reserves to $25.1 bln at end of Q2, while clarifying it had not yet gone along with diversifying its reserves. Less than a month ago, the central bank said it would shift 10% of its reserves from US dollars to euros and gold to alter its 98% USD/2.0% EUR proportion.

This week's busy data/event schedule kicks off tomorrow (Tuesday) with the October M3 money supply from the Eurozone, and the US figures on October durable orders, October existing home sales, November consumer confidence and speeches from Fed Chairman Greenspan and Chicago Fed's Moscow.

Euro readies for temporary retreat

Losing half a cent from its 1.3165 highs, EURUSD is expected to extend its retreat in a relatively data-free session for the technical signals to stabilize from their extreme levels. Traders may accelerate the euro's declines towards the 1.3030s amid cautiousness with Bernanke's speech reiterating the Fed's inflation vigilance. Bernanke may well maintain a relatively hawkish rhetoric in order to slow the pace of dollar decline rather than solely reflect the inflation picture. Thursday's release of the US October core PCE price index will carry significant weight in shaping the market's latest inflation assessment. A figure below 2.3% could well renew dollar selling as it weakens the case for the Fed's long standing inflation vigilance and further make way for the path to easing policy.

German finance Minister Steinbrueck was unequivocal in his optimism, indicating the economy is firing on all cylinders and that next year's VAT tax will not be a shock. Even one member of the economic "Wise Men" said 2006 growth could surpass his 2.4% forecast.

But remarks from France's finance Minister Thierry Breton indicating "of course" he would discuss the euro with fellow European ministers today do not carry the same weight as did the more direct ECB criticism by his nation's president and Prime Minister of two weeks ago.

EURUSD sees interim support at 1.3060, followed by 1.3025-30. The relative strength index currently shows overbought levels at their highest since October 26. Interim resistance stands at 1.3140, followed by 1.3180.

USDJPY seen in corrective bounce

There was no major currency reaction to remarks from Bank of Japan Governor Fukui reiterating the central bank would "adjust interest rates gradually" in order to "avoid impeding the expansion of Japan 's economy". Fukui referred to the recent developments in FX as having "moved slightly", expressing no signs of worry or dissatisfaction with the yen's sharp run-up. Non-central bank officials may add their own version of the FX arena and sound off more aggressive remarks regarding the danger of rapid yen gains, in which case the dollar could get a brief fillip. Concerns ahead of Tuesday's Bernanke speech on the US economic outlook may also be dollar positive as the Fed Chairman is unlikely to depart from his obligatory hawkishness and risk a renewed attack on the dollar.

But these dollar gains are seen largely corrective in nature, with temporary upside capped at 116.55, followed by 116.85-90. Support seen holding at the 116 figure, backed by increased buying at 115.70.