This is the second of a 2-part series on uranium investing. In the last section, we examined the fundamentals of uranium uses, extraction, and nuclear power. In this section we will look at the economics and investment perspectives in the uranium market. (Part 1 here)

The Uranium Market

Due to its sensitive nature, uranium is not traded in an open market. Most uranium is sold under long-term contracts between suppliers and consumers. The Ux Consulting Company www.uxc.com publishes a weekly Uranium "spot" price. This is not actually an auction price quote but derived from that week's contract activity. No futures, options, or other derivative contracts trade on uranium.

Uranium prices are quoted in pounds of U3O8 "yellowcake". Global production in 2005 was 108 million pounds of U3O8. Production growth has been about 2% per year over the last decade. Since the early 1990s, much uranium supply has been recovered from decommissioned Soviet era nuclear weapons. This supply resulted in a sharp drop in price during that era. Russia is now diverting much of that supply into domestic uses and is not going to be a significant source of global supply in the future.

Low prices during the 1990s devastated the uranium mining industry. This was both due to the lack of new reactor construction and the supply of uranium recovered from dismantled Soviet nuclear weapons. Many mines were mothballed and the future of nuclear power looked bleak. Rising oil prices, global warming, and new geopolitical tensions have now revived interest in many forms of alternative energy including nuclear power. Many countries, most notably China and India, are actively building new nuclear power plants to power their torrid economic growth.

Global uranium fuel consumption is estimated to be about 180 million pounds annually. But wait ... we just learned that mine production was only 108 million pounds. Reprocessing from spent fuel rods represents only 11 million pounds and uranium stockpile estimates are a wildcard. It seems that there is a huge shortfall in uranium mine supply. This shortfall in mine supply has been the core investment rationale for uranium.

Although uranium demand currently outstrips mine supply, the IAEA estimated that "Global Uranium Resources to Meet Projected Demand" in a 2006 study. The authors estimated that global mine sources have adequate recoverable resources to meet current electrical demand for 85 years using light water reactor technology. Using breeder technology, that same resource would stretch for 2500 years. So the future status of the uranium mine supply deficit is highly contingent on a number of factors which we will examine further.

Nuclear Power Economics

Unlike other power generation technologies, raw fuel is a relatively minor cost in the production of nuclear power. Fixed costs dwarf fuel costs in nuclear power generation, as long as fuel remains within a historical cost range. The chart below breaks down the cost of 1kg (2.2lbs) of reactor-ready fuel. Less than one third of the total fuel cost is reflected in the uranium input costs at an assumed $53/kg (typical long-term contract price of about $24/lb). Traditionally, enrichment is the major component of fuel input cost and represents over half of the contract price for a finished fuel component. However, current spot uranium pricing exceeds enrichment costs. Keep that in mind as we go forward.

| Uranium: | 8.9 kg U3O8 x $53 | 472 |

| Conversion: | 7.5 kg U x $12 | 90 |

| Enrichment: | 7.3 SWU x $135 | 985 |

| Fuel fabrication: | per kg | 240 |

| total, approx: | US$ 1787 | |

Nuclear power plant construction, operation, maintenance, and fuel disposal consume far more costs than the uranium. This makes uranium demand price "inelastic". This means that power plant consumers of uranium are likely to purchase fuel at the same quantity regardless of the cost.

There is a limit however. On average, nuclear power currently has a marginal cost advantage over coal and gas, but those advantages are vulnerable to the market prices of the various fuels. The chart below shows the average cost per kWh of nuclear, coal, and gas generation around the world.

| nuclear | coal | gas | |

| Finland | 2.76 | 3.64 | - |

| France | 2.54 | 3.33 | 3.92 |

| Germany | 2.86 | 3.52 | 4.90 |

| Switzerland | 2.88 | - | 4.36 |

| Netherlands | 3.58 | - | 6.04 |

| Czech Rep | 2.30 | 2.94 | 4.97 |

| Slovakia | 3.13 | 4.78 | 5.59 |

| Romania | 3.06 | 4.55 | - |

| Japan | 4.80 | 4.95 | 5.21 |

| Korea | 2.34 | 2.16 | 4.65 |

| USA | 3.01 | 2.71 | 4.67 |

| Canada | 2.60 | 3.11 | 4.00 |

Source: OECD/IEA NEA 2005.

At some point fuel costs DO become important and affect the economic competitiveness of nuclear power vs. other sources. The chart below was from a Finnish study that relates the cost of fuel vs. cost of electricity for the three main fuel sources.

These year 2000 data show that a doubling of fuel prices would result in electricity cost for nuclear rising about 9%, for coal rising 31% and for gas 66%. As fuel prices rise, the influence of fuel costs rises also. Uranium was only $10/lb in 2000. It is now over $70 which doing the math should result in a 40% rise in average costs for nuclear generated electricity since 2000. Most nuclear utilities are still operating under older contract pricing so this still hasn't filtered to customers. Gas and coal-fired electrical generation have also been hit by large fuel cost increases so nuclear has remained cost competitive. The influence of fuel prices over fixed costs is now much greater than in the past and uranium prices are now a much more significant component of electricity cost. Under current conditions, another huge increase in uranium cost may hurt nuclear cost competitiveness.

Chart Source: http://www.uic.com.au/nip08.htm

Uranium Investment

As natural resources go, uranium is a relatively small and exclusive market. At $50/pound, the total mine production has a value of about $5 billion. There have been traditionally few investment opportunities in uranium mining or processing. This hasn't stopped investors from pushing up prices dramatically. With such a small market, it does not take much buying to push prices. The 1-year chart of weekly spot prices below shows that uranium has doubled in price over the course of just one year.

Mining companies

On the mining side there is only one mining company that qualifies as a blue chip in the industry, the Canadian mining giant Cameco (CCJ - NYSE). Over the last three years, opportunities have multiplied as the price has multiplied. There are dozens of uranium exploration companies that are now trading in both the US and Canada, each offering a potential bonanza in uranium exploration.

Investment Funds

There is only one mutual fund dedicated exclusively to uranium. It is a new Canadian ETF called the Uranium Participation Corporation (U.TO). The Uranium Participation Corporation was introduced in 2005 and represents interest in stockpiled U3O8 yellowcake. More ETF opportunities are likely to be introduced in the near future assuming that investor interest remains strong in uranium.

Uranium Enrichment

There is only one company, USEC Inc. (USU - NYSE), involved in uranium processing and enrichment in the US. In France a company called AREVA performs enrichment and refining for the European nuclear industry and is traded on the Paris and Frankfurt exchanges. Other countries have either privately-owned or government facilities to process uranium.

Investor influence

Investors have had a profound influence on the uranium market since about 2004 when the price really took off. The chart below from UxC shows the spot market volume and the investment participation within the spot market. Before 2005, investors were essentially absent but now represent 7-9 million pounds per year of demand. (The totals for 2006 in the chart below represent a partial year.)

It is apparent that investor activity is likely responsible for the lion's share of recent gains in uranium. Without investment buying, the spot market would be relatively weak compared to past years. This will not be without consequences in the nuclear industry. The sudden and aggressive inflow of investors into the once sedate uranium market has undoubtedly caused some serious re-evaluation of future nuclear plant operating policies and procedures.

Uranium Opportunities and Risks

Opportunities

- Persistent deficit - A study by the IAEA (International Atomic Energy Agency) shows a significant deficit in production vs. reactor requirements through the year 2020.

- New plant construction - China and India are leading in the construction of new nuclear power plants and these plants will require fuel. More nuclear installations will be built within the next decade than decommissioned.

- Mine development cycle- New mines can take as much as a decade to become operational, delaying the potential for new mine supply to ease the deficit. (Note that the construction cycle for power plants is similar in duration.)

- Global warming initiatives - Nuclear power does not generate greenhouse gases. Should major energy consuming countries adopt aggressive global warming initiatives, nuclear power would be an obvious beneficiary.

- New mining opportunities - Persistently high uranium prices will open up new mining and extraction opportunities for investors.

- Investor participation - Although energy and natural resource investors have bought heavily into uranium, it is still not widely held by the broad investment community. There is still a lot of room for expansion.

Risks

- Technological risk - New technologies such as the Integral Fast Reactor could turn the uranium supply/demand equation upside down. The construction of high-efficiency breeder or CANDU reactors could create a permanent supply surplus.

- Disaster risk - There is always the potential for another Chernobyl or Three Mile Island disaster that will create new political resistance to nuclear power.

- Nuclear proliferation - many rouge states are actively building nuclear weapons. Should a nuclear weapon be used in an aggressive act, resistance to nuclear power may dramatically increase.

- Nuclear disarmament - Although the possibility now seems remote, a new global nuclear disarmament effort would bring millions of pounds of bomb-grade HEU into the market as the result of weapons dismantling. This has happened one before in recent history resulting in a uranium price crash, so I wouldn't count it out. Geopolitics can change quickly.

- Plant operational changes - The nuclear power industry may react to potential fuel shortages or high fuel prices by using higher enrichment levels, making fuel use much more efficient and as a result reducing or eliminating the supply deficit.

- Reprocessing - The US and other countries may elect to reprocess spent fuel, creating additional supply.

- Alternative fuels - Thorium has been investigated for a long time as a possible nuclear fuel. Its advantages include abundance and immunity from nuclear proliferation dangers. It cannot be used in light water reactors but CANDU and Breeder designs can accommodate thorium fuels. Both China and India have shown interest in thorium fuel cycles for their new CANDU and breeder reactor projects. Plutonium is also an alternative fuel and is usually mixed with uranium in MOX fuels which can be used in traditional reactors but have the disadvantage of nuclear proliferation danger.

- Investor sentiment - Investors have bought heavily into the future of uranium. Should any disappointment befall the market, sellers could swamp the small uranium investment sector.

It is obvious in retrospect that the price of uranium was too low at $10-20/lb to maintain adequate supply and prices had to rise. At $70, the economics is much different and investment risk in the uranium market is now much higher. As we have seen, the uranium market is complex and defies simple "sound-bite" analysis. Many factors, both bullish and bearish can be identified in the uranium market. As price rises, so does risk. Uranium may continue to rise in price, but I think that the easy money is now behind us.

Investment Strategy

Uranium is a single-use commodity that has great opportunity in an era of energy uncertainty. I believe that nuclear power has a bright future as part of a comprehensive global energy infrastructure. But it is not an energy panacea. It has unique risks and high costs. As the uranium market matures, it will start behaving more like any other commodity, with ups and downs, whipsaws and bubbles. I am convinced that there are still good investment opportunities remaining in uranium mining and processing. But there are also great dangers lurking for overly optimistic investors who have bought into speculative uranium plays that have questionable economics.

The small universe of uranium investment vehicles is both a blessing and a curse. The limited number of uranium related securities makes analysis much easier, but it has become difficult to find the hidden gem among this picked-over sector.

I think that the uranium processing companies represent the best risk/reward ratio at this point in time. Recent contract prices on uranium now exceed enrichment costs and put uranium processors into a better market position. They have underperformed the miners and are still trading at reasonable valuations from a fundamental perspective. There are only two uranium processors that are publicly traded, USEC in the US and AREVA in France.

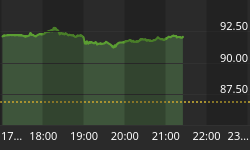

Looking at the chart below for USEC, we can see that it is trading higher than three years ago, but it has dramatically underperformed the rest of the uranium complex. USEC has suffered a lot of bad news due to technical issues and high input costs. Technically, it has formed a solid bottom at just above $9 and has broken out above its 200-day MA. Long-term, it shows a solid uptrend. It still has significant overhead resistance, but it looks poised to poke through that resistance. Although it does not have the profit potential of a junior mining company, USEC looks like a low-risk way to participate in the uranium boom. As they say, buy 'em when nobody wants 'em. (I own a small position in USEC.)

France's AREVA has performed much better than USEC. AREVA is more diversified than USEC. They build reactors and power plants as well as process fuel. Unfortunately it is not traded on US or Canadian stock exchanges. I have heard talk that ADRs may eventually be traded in the US. But in the mean time, it may be a good candidate for European investors. The technicals look quite good for AREVA. The chart below shows that AREVA is sitting right at resistance just under 650 and is trading well above the 200-day MA. This stock looks likely to eventually break through resistance and go to all-time highs, but may test the 200-day once again before it breaks out. (I do not own AREVA.)

Higher uranium prices encourage nuclear utilities to utilize higher enriched fuels which are more efficient and generate less waste. Also, re-enrichment of depleted uranium becomes economic at high uranium price levels. I think that both these companies will be the beneficiaries of increased demand for enrichment services as a result. These companies would also benefit from increased reprocessing should more countries decide to reprocess spent fuel.

Another potentially bullish factor for uranium processing companies is a new proposal from the IAEA for a 10-year moratorium on the construction of new uranium processing plants as a deterrent to nuclear proliferation. Such a moratorium would create a processing bottleneck and give these companies powerful pricing power over enrichment services. If investors decide to shift even a modest amount of capital into the tiny uranium processing industry, these two stocks could be bid up significantly.

Perspectives on Uranium

We have learned that uranium is being consumed faster than it is being mined. This fact has been identified by many analysts at the main cause for the spectacular rise in its price. We also learned that the story of uranium is complex. Uranium is not a rare element and is available via many primary and secondary sources. There are immense untapped primary sources and the extent of global stockpiles is debatable. There are many options for nuclear power plants to feed their reactors and these alternatives are now becoming economically viable. According to industry sources, there is little danger of nuclear power plants running out of fuel under any foreseeable circumstances. If there really was uncertainty over fuel supply, nobody would be building billion-dollar new nuclear power plants. In short, the fundamentals give a mixed investment picture for uranium at this point in time.

It is true that a mine supply deficit is a bullish factor in uranium. But a mine supply deficit by itself does not in itself mandate a price increase. Silver had been in a structural mine supply deficit for decades before the price started to rise. It seems that in our finance-dominated marketplace, fundamentals are secondary to liquidity trends Global liquidity has been in an historic expansion since the market meltdown of 2000-03. In a desperate attempt to recover from that meltdown, governments, central banks, and private financial institutions have loosened credit to the point that they created the conditions for extreme speculation. This historic tidal wave of global liquidity has given global investors both the means and the motive to bid up metals, energy, and almost all tangible assets. It is no coincidence that copper, nickel, zinc, lead, uranium, and almost all other metals are dramatically higher in price since 2003. Not all of these markets are in supply deficits. I contend that investor demand fueled by easy money is likely the primary driver behind the rise in industrial metals, not necessarily the condition of the physical markets.

Even though I just presented a fairly exhaustive fundamental analysis of a single commodity called uranium, I claim that fundamentals are not the dominant force behind the current bull markets in uranium and industrial metals. I chose uranium to analyze because it is actually a simpler market than copper or other multi-use metal. With uranium, we can see that a deep analysis can give a much different picture than a superficial investigation. But it does not matter in a finance-dominated market. The technicals rule in a finance-dominated market and the fundamentals are only a story used to justify technical market behavior. In this perspective, uranium an example of what can happen when an army of well-funded investors descend upon a small and vulnerable market.

It is my contention that a combination of extreme global liquidity creation and investor zealousness is pushing prices higher. So as long as those conditions persist, uranium and other industrial commodities will also continue to be strong. Should global liquidity contract or investors become spooked for some reason, all bets are off. Prices could fall regardless of the underlying supply/demand conditions.

As long as finance remains dominant over the economy, investor behavior will determine the pricing of industrial commodities and probably most other assets as well. At the time of this writing, I don't see compelling evidence of any imminent change in these conditions. In other words the trend will remain in place until it doesn't. This is not a cop-out, just an acknowledgement of our limited ability to forecast the future.

But as investors we must anticipate likely future scenarios to exploit opportunities and manage risk. The best way to do this in a finance-dominated market is with technical analysis. TA is the most effective method of determining liquidity flows and investor behavior. There are many TA tools that can be employed. I think that the most powerful tool in this environment is inter-market analysis. If my assumption that the metals bull market is an artifact of global liquidity is correct, then trend changes should be reflected in all related markets. Metals investors should keep a sharp eye on both industrial commodity markets and global credit markets for clues to the future.

This implies that a source of concern for metals investors should be the condition of the global credit system. One of the prime sources of new liquidity is the mortgage security market. The explosion in mortgage credit is intertwined with the global real estate bubble. The real estate bubble is now in retreat. This will ultimately be reflected in the price of mortgage securities which is a multi-trillion dollar market. It is possible that a mortgage security market bust could cause investors to seek refuge in the much smaller hard asset market. If so, the prices of industrial metals, gold, and other commodities could soar even if bonds and stocks collapse. This is not a prediction, just a possible scenario. A mortgage security market bust could also take down commodities depending upon investor sentiment. Technical analysis will give the best indication of liquidity flows in all of these markets.

****

This concludes my rather long-winded analysis of uranium. I started with a single obscure commodity and tied it into the global liquidity expansion, industrial commodities, and the real estate bubble. It is a tightly interconnected world! Uranium is a fascinating subject and I really enjoyed doing this research. I dubbed this article "Perspectives on Uranium" because my own perspectives on energy were profoundly changed by performing this research. I discovered that the Universe is literally alive with energy. Humans have barely begun to exploit the energy locked up within the structure of matter. Future technology will ultimately provide abundant energy for all of humanity's needs ... if we use it wisely.

Special thanks to Nuclear Materials Engineer Mark Hugo for his technical assistance on this article.