I had another installment of "Banks and Bubbles" all set to go today. This one was going to have a little fun with the rumor that Bank of America is negotiating to buy Countrywide Credit, and repeat the by-now-tired observation that at the peak of the credit cycle, bankers tend to start indulging their inner day traders, which always leads to trouble, yada yada.

But something more interesting just happened. It seems that the markets have stopped mistaking the banking debt orgy for "innovation" and started seeing it for what it is: the last bit of debauchery in history's greatest credit bubble. According to reports by Bloomberg and Associated Press, the price of "credit insurance" on the bonds of the big investment banks has spiked.

To understand this bit of poetic justice, you first have to understand what credit insurance is. In a nutshell, it's a derivative contract, known as a credit default swap, in which one party promises to cover whatever losses result from a given borrower not being able to repay a given loan. Sounds innocuous enough, right? But in bubbles, otherwise useful tools often become monsters that enrich their masters for a while and then break free, eviscerating everyone within reach. Recall the collateral damage from junk bonds and dot.com IPOs, and you get the idea.

In the case of credit insurance, the financial engineers at the big investment banks and hedge funds figured out that writing these contracts -- that is, promising to cover losses on various kinds of bonds -- was easy money as long as no one was defaulting (like writing flood insurance in a drought, as Prudent Bear's Doug Noland puts it). And so the bubble machine created a positive feedback loop, with hedge funds writing cheap credit insurance on pretty much anything and investment banks lending money to pretty much anyone, in order to insure the debt and sell it to pension funds and other gullible souls. Defaults, even among the most overleveraged companies, were low because there was always another investment bank waiting to underwrite another issue of junk bonds. So hedge funds competed to write the insurance, sending the cost through the floor. And the big investment banks borrowed immense amounts of money to leverage this process -- after all, if no one is defaulting, you can bet infinite amounts on the proposition with impunity. They reported stunning earnings, and paid out bonuses that would have made Mike Milken and Frank Quattrone smile.

But this week cycle shifted into reverse, and suddenly the linchpin of the whole system, cheap credit insurance, ain't so cheap. Based on what it costs to insure it against default, the debt of the of Wall Street's biggest banks now looks like junk, which is another way of saying that Goldman, Merrill, Lehman and the other masters of yesterday's universe have been exposed for what they are: slick, sophisticated Ponzi schemes that can only operate in their present forms with ever-larger infusions of new money. Cut off the cash -- by, say, raising the price of credit insurance -- and the whole thing falls apart. With that in mind, here's how Bloomberg put it today:

Goldman, Merrill Almost 'Junk,' Their Own Traders Say

Goldman Sachs Group Inc., Merrill Lynch & Co. and Morgan Stanley, which earned a record $24.5 billion in 2006, suddenly have become so speculative that their own traders are valuing the three biggest securities firms as barely more creditworthy than junk bonds.

Prices for credit-default swaps linked to the bonds of the New York investment banks this week traded at levels that equate to debt ratings of Baa2, according to Moody's Investors Service. For Goldman, Morgan Stanley and Merrill that's five levels below the actual Aa3 rating on their senior unsecured notes and two steps above non-investment grade, or junk.

Traders of credit derivatives are more alarmed than stock and bond investors that a slowdown in housing and the global equity market rout have hurt the firms. Merrill since 2005 has financed two mortgage lenders that subsequently failed and bought a third, First Franklin Financial Corp., for $1.3 billion.

"These guys have made a lot of money securitizing mortgages over the years in a mortgage boom time," said Richard Hofmann, an analyst at bond research firm CreditSights Inc. in New York. "The question now is what is the exposure to credit risk and what are the potential revenue headwinds if they're not able to keep that securitization machine humming along."

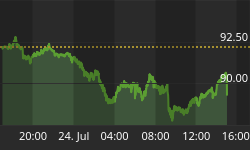

Credit-default swaps on the debt of Goldman, the world's biggest securities firm, have risen to $32,775 per $10 million in bonds, up from $21,500 at the start of the year, according to prices compiled by London-based CMA Datavision. The price touched $35,000 on Feb. 28, the highest since June 2005.

Spokesmen and spokeswomen for Goldman, Lehman, Merrill and Morgan Stanley declined to comment. A spokeswoman for Bear Stearns didn't immediately return calls for comment.

The effects of a cutoff of cheap credit to the securitization machine will be felt pretty much everywhere. But one obvious -- and okay, amusing -- impact will be on the big investment banks' market value. If their debt is junk, then their earnings -- driven as they are by cheap capital -- are suspect. If their earnings are suspect, then their shares probably aren't worth anything like the levels they've soared to on the wings of their last few blow-out quarters. Can't wait for Monday.