"...The problem of the chicken and the egg applies going forward. Just when will the markets regain their appetite for risk...?"

Oyakodon is a lunchtime favourite of Japanese school children.

A bowl of rice topped with chicken and egg, it translates literally as "mother and child" - a tasteless joke for the chicken and its babies, perhaps. But add a dash of soy sauce and it makes for a very tasty meal.

The chicken-and-egg question of Japanese carry-trades, on the other hand, is rapidly making investors sick the world over. Which came first - the end of carry, or the collapse of share prices in Shanghai? The newswires blame Beijing's threat of higher interest rates...new restrictions on stock market IPOS...even a tax on financial speculation!

But what if the sudden unwinding of the carry-trade caused Shanghai to collapse instead? If you think that oyakodon has got little to do with the S&P losing 5% since this time last week, take note. For the chicken and egg question also applies going forward.

Just when will the markets regain their appetite for risk? Could it be that the entire global carry-trade - estimated at anything between $330 billion and $1 trillion - needs to unwind first?

The cutaway collars of the City don't want to wait for an answer. Word in London on Friday claimed that several major players thought the Yen's sudden up-turn couldn't roll on. So they sold the Yen afresh, putting the cash to work for a higher rate of return elsewhere.

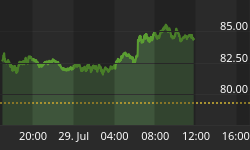

But anyone backing the Yen to start tumbling again will already be suffering from indigestion today. The British Pound - a top destination for carry-trade cash thanks to Britain's 5.25% interest rates - has now sunk nearly 3.6% against the Yen since Friday morning.

All things being equal, the expected pay-out to JPY/GBP carry trade players would have only been 4.75% over the next 12 months as it was. Now the speculators' no-brainer winnings are shrinking, and fast.

Borrowing cheap Yen like this used to be such a no-brainer, of course, that asset markets across the globe went off their head. Even the Nikkei picked up, ending its 14-year bear market, as the Japanese currency sank. Lower export prices made Japan Inc. competitive once again. So long as Japanese interest rates stayed low, and the Yen just kept getting cheaper, what could go wrong...?

But suddenly the dish of the day is hard cash, most of all Japanese cash served in prompt settlement of "short" positions.

The Swiss Franc's also back on the menu. With base rates at barely 1.9%, they have sat below the National Bank's inflation target of 2.0% since the end of 2001. Now the SNB's threatened to raise its rates too, just like the Bank of Japan, and so everything else is off - stocks, emerging markets, asset-backed securities, high-yield currencies...

"Japan and Switzerland have large current-account surpluses," noted Stephen L. Jen for Morgan Stanley late last month, "4% and 16% of GDP in 2005 respectively [plus] a solid net investment position (36% and 114% of GDP in 2005), and higher-than-potential economic growth."

Says Jen, "Most economic theories predict that the JPY and the CHF should have appreciated in 2006. In fact, our valuation models, which are based on these economic theories, suggest that the JPY is now more under-valued than the Chinese RMB. For the JPY and the CHF to depreciate, their low cash yields have almost certainly played an important role."

In other words, the cheap Yen and cheap CHF only got cheaper thanks to investors selling them because they were cheap. As even a school child could see, the word "cheap" figured loudly in the carry-trade logic. So anything risking a rise in the Yen or Swiss Franc posed a big fat risk to carry-trade investors, too.

"The latest plunge in global stock markets came on the heels of a hike in the Bank of Japan's overnight loan rate to 0.50%," as Gary Dorsch notes at Sirchartsalot.com, "its highest in a decade, and renewed warnings by Swiss central bankers of a tighter monetary policy in the weeks ahead, and threats of a short squeeze on speculators betting against the Swiss franc."

If the end of the carry-trade caused the collapse in Shanghai - which is still pulling down asset prices the world over today - will it take fresh declines in the Yen and Swiss Franc to fund a bounce in the markets from here?

On Feb 28th, the Bank of Japan's Atsushi Mizuno warned the world that the carry trade "could cause distortions in global asset prices by speeding up capital outflows from Japan." Better late than never, perhaps, it was a typically speedy response from a central bank wonk.

But the problem today isn't capital outflows from Japan. It's now capital inflows back into the land of the rising Yen, the world's third-largest economy where the savings rate for salaried households rose to 27.5% last year.

Squeezing an over-grown chicken back into its egg-shell was never going to be easy.