"With the Pound so strong, how come inflation is rising so fast...?"

"SAVINGS INCOME normally has 20 per cent tax taken off before you get it," explains the British state on its "Direct Government" website.

And as anyone trying to save money today also knows, inflation is deducted at source, too.

Ten years ago, New Labour - the current administration - swept to power with the greatest electoral majority granted by British voters to any party since WWII. And the first decision taken by Gordon Brown, the new finance minister, was to give operational independence to the central bank, the Bank of England.

By way of thank you, or so the Bank would have you believe, it has given the nation record price stability. It's tweaked interest rates and twiddled the knobs of monetary policy so deftly, the Bank has abolished the risk of runaway inflation, but also steered clear of the dreaded deflation, too.

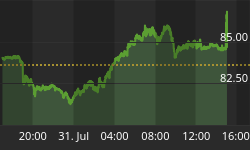

Good work! Hence the Two-Dollar Pound hit on Tuesday - the first $2.00 exchange rate for GBP/USD since the summer of 1992. On the Consumer Price measure (CPI), the cost of living rose 3.1% in March; forex traders the world over now expect higher Sterling interest rates to counter these numbers.

But take a peek through the other end of the telescope for a moment. With the Pound so strong, how come inflation is rising so quickly?

And rather than speculative flows being a mere by-product of tackling inflation with higher rates, isn't a stronger Pound the only way to prevent inflation - already at a 16-year high - from running ahead even faster...?

Somehow, the Bank of England has built itself a fantastic reputation for inflation-busting, despite presiding over the greatest flood of money growth since the huge bubble-top that preceded the collapse of UK house prices - and the collapse of Sterling along with them - at the end of the '80s.

The Pound was the first of the world's top 5 currencies to gain higher interest rates after the "Deflation Scare" of 2003. The BoE jumped to raise its rates seven months before the US Fed started hiking Dollar rates off their half-century floor of 1%. (The European Central Bank took until Dec. 2005; the Japanese and Swiss have only just got round to it.)

Mervyn King, governor of the Bank, also loves to talk the talk. He's repeatedly warned that he's not afraid of higher rates ahead if necessary. He even makes occasional reference to "rapid money and credit growth" - so at least he knows there's a problem.

Indeed, "I am surprised it has taken ten years and 120 meetings of the Monetary Policy Committee before a [1.0%] deviation of inflation from target," he says in response to the latest Consumer Price data. He's mandated to send the chancellor an explanation of why CPI inflation is off-target if it moves too far away from the Bank's target of 2.0% per year.

According to Dr.King, he relishes this opportunity to explain his policies. But his open letter (posted here) reveals little of the Bank's immediate policy response. And despite gaining such kudos from the forex markets, all the Bank of England has really given British voters - as Tuesday's awful cost-of-living data prove - is a collapse in the real rewards paid on cash savings.

Over the last 10 years, real Sterling interest rates have shrunk to their lowest level since the late 1970s. Come March 2007, and even ignoring the deduction of basic-rate tax, real returns paid to cash savers in Britain fell to just 0.45% - their lowest level since the "Deflation Scare" of mid-2003. That summer, spooked by the threat of inflation vanishing altogether, the Bank of England cut its base rate to a half-century low. Real interest rates as measured against the respected and trusted Retail Price Index dropped to a two-decade low of 0.40%.

The UK stock market leapt higher. UK house prices rose at their fastest pace in history. Household savings rates shrank towards zero. And no wonder. You'd now have to go back to May 1981 to find British savers enduring a worse rate of return on cash-in-the-bank post inflation.

But that spring, Bank of England interest rates stood at 12%. Retail price inflation - the old and more trusted measure - was running at 11.7% year on year. Now the Bank of England is expected to raise base rates to 5.50% at its May meeting. Unless inflation falls away dramatically, however - an unlikely event given that inflation in energy prices slowed in March, only to be overtaken by soaring prices for milk, bread, furniture and furnishing, large electrical goods and even computer games - then holding cash on deposit will continue to teeter on the verge of costing British citizens money.

After tax - that other deduction at source - British savers are already under water. They'd best hope that Mervyn King makes good on the currency market's expectations of higher rates.

Otherwise, the Pound looks fated to fall - fast - pushing the rate of inflation yet higher again.