"Despite a minor struggle last week, the trend continues to be up until it's not. Weaker consumer confidence and existing home data could be the start of that reversal." ~Precious Points: Sailing the Seas of Liquidity, April 21, 2007

The dollar is sharply lower for April, and stocks are up largely on that fact, but precious metals, which would traditionally be the beneficiaries of a sinking dollar, are looking to come out roughly flat. Once again, recovery in the metals from softness earlier in the week was foiled by a Friday rally in the dollar. But the real damage started on Tuesday's economic data.

Though metals are global markets, New York trading over recent months has kept metals moving mostly higher, along with stocks, on economic strength. But now a persistent trend toward higher interest rates in key foreign economies, combined with tighter regulation in China and growing inventories at exchanges, has prevented metals from taking advantage of the otherwise beneficial environment. Consumer price inflation didn't slow consumer spending, and this had traders buying again on Friday. The rumblings of geopolitical turmoil from Russia to Saudi Arabia didn't hurt either, but the dollar's rebound severely limited the upside potential.

After this week's economic data, the stage is just about set for the May 9th Fed meeting. Resilient consumers keep the economy growing, however slightly, and signs of slower inflation are starting to appear. Remember last month the Fed didn't entirely shift to a neutral bias, but did leave the back door open for an accommodation if the data deteriorates significantly, which it has not yet done. Still, fed funds futures remain priced for a 100% chance of a 0.25 cut by the end of the year and bond yields refuse to rise to the level of the overnight rate. This update has already addressed the effect of rate cuts on precious metals in previous. But since last fall, we've also described the goldilocks economy as one in a tight range where the Fed could keep rates steady work exclusively through its open market activities.

Curiously, and way under the mainstream radar, the Fed took a different direction in its open market activities this week and actually started removing money from total bank deposits through reverses. The move could reflect less demand for money, but in this case is probably more of a preemptive measure to goose up bond yields and make the dollar more attractive. It's also an anti-inflationary step and if this trend develops, it would be profoundly bearish for metals, especially if in lieu of a change in interest rates.

So, after a protracted decline, last week's strength was probably not the end of the decline for the dollar, but this consolidation period is probably not over yet either. Weakness in the yen has continued to foster liquidity, limiting downside, and making metal a potentially profitable alternative if the current favor for stocks unwinds. Warning signs, nonetheless, are multiplying.

For the time being, though, the path upward has been reopened for gold and silver to drift higher towards a retest of the recent highs, which will provide significant resistance. Just as many speculative traders go long, the threat is that a failure from the $700 area would either appear to be a double top or be labeled a corrective move up before a new impulsive wave down.

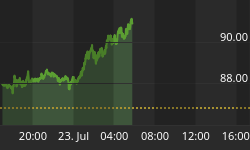

Chart by Dominick

At the very least, readers of this update were alerted to the downside risk in recent weeks. Members at TTC not only caught the top, they were alerted to buy the exact bottom of the recent weakness. The first signal to start looking for a long was when the move from highs earlier this month equaled the decline off the February highs. The chart below shows the exact buy signal and subsequent confirmation from the 5min trend cycle chart, which pegged to the top of it's oscillator as price moved lower. The coming weeks are certain to be choppy, but, by playing the trends, sharp traders can squeeze profits out of a flat month or down month.

Next week's data doesn't offer much in the way of encouraging prospects for the metals, at least in the early part of the week, assuming the numbers come in as expected. Monday's core PCI will probably continue the trend of relatively benign inflation data. Not until Thursdays' productivity report is there a significant chance of domestic economics driving a rally in metals, and this only if the numbers are inflationary enough to spike investor interest in metals.

Despite the media circus surrounding Dow 13000, better investors know to take the number lightly. Given the steady rate of M2 growth and the now unknown rate of growth in what would be M3, stock valuations would have to rise just to retain the same level of relative value. But, as the chart below illustrates, in terms of gold, the indices aren't keeping up the pace and are actually far from record highs.

Of course that's exactly why American stocks have looked so tantalizing lately, particularly to holders of foreign currency, who have a lot more buying power now that the dollar has broken south. Metals, on the other hand, are still finishing up a consolidation period after a nice, long run against all major currencies. As long as stock valuations are so favorable, a breakout to new highs in the metals seems unlikely.