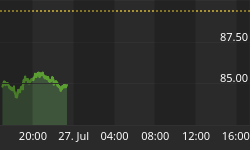

Effective today, the Chinese Ministry of Finance increased its so-called stamp tax on stock market transactions from 0.1% to 0.3% in an effort to curb speculation in the Chinese stock market. This stamp tax is nothing but a transactions tax imposed on both buyers and sellers of stocks. In reaction to the increased tax rate, the Shanghai Composite stock index fell 6.5% today. Although the increase in this transaction tax may temporarily temper stock market speculation, it is doubtful that it will temper overall asset speculation as it does not get at the root cause -- rapid central bank credit creation. And that rapid central bank credit creation will not be curbed until the People's Bank of China (PBOC) allows the yuan to appreciate vs. the dollar. The PBOC has to rein in bank reserves growth if it wants to moderate inflation - inflation in asset prices as well as goods/services prices. And to rein in bank reserves growth, the PBOC will have to allow the overnight interbank interest rate to rise, something it has been reluctant to do. But so long as the PBOC continues to support the dollar, neither bank reserves growth can slow nor can interbank interest rates rise. (For additional discussion on the PBOC's predicament, see People's Bank of China Takes With One Hand, Gives With The Other?)